Compare the best cross-border payment solutions for SMBs in 2026, including Wise, AllScale, Stripe, and Airwallex. Discover faster international payments, lower FX fees, stablecoin settlement, and smarter global business banking—plus a risk-free 100-night trial mindset for better payment workflows.

Cross-border payments used to be a back-office headache reserved for large exporters and multinational companies. Today, even a five-person agency may need to invoice clients in three countries, pay contractors in different currencies, settle marketplace revenue, and protect margins from foreign exchange costs, This widespread fragmentation of digital workflows is forcing lean teams to look for more efficient alternatives to manage global settlement.That shift has made cross-border payment solutions for SMBs one of the most important software decisions for global small businesses.

In practical terms, a cross-border payment platform helps a business send, receive, convert, hold, or settle money across countries and currencies. As explained in Airwallex’s guide to cross-border payment services and solutions, these tools usually combine capabilities such as multi-currency accounts, foreign exchange conversion, payment acceptance, and international transfer rails.

The best solution depends on the nature of your business. A freelancer receiving client payments may prioritize fast onboarding and transparent FX. An ecommerce brand may need local payment methods and checkout conversion. A microbusiness serving global clients may want a digital dollar account and stablecoin settlement. This guide compares the leading options and places AllScale at number two because it is especially relevant for microbusinesses and global teams that want modern stablecoin-based settlement without forcing clients to use crypto tools.

The right provider should reduce the number of manual steps between invoicing, collection, conversion, reconciliation, and payout. In practice, SMBs should compare providers across five dimensions: coverage, currency control, payment experience, cost transparency, and operational fit.

Best for: SMBs that want transparent international transfers, multi-currency receiving, and straightforward global money movement.

Wise Business is one of the most recognizable cross-border payment solutions for small businesses because it focuses on the core job most SMBs care about: paying and getting paid internationally without opaque bank FX spreads. On its Wise Business account page, Wise describes a product for making payments, getting paid, spending, and managing money in different currencies. It also states that more than 700,000 global businesses move and spend $21 billion monthly through Wise, which gives it strong credibility among small international companies.

The platform is especially useful for agencies, consultants, SaaS startups, and remote-first companies that need to receive major currencies, pay suppliers, and run batch transfers. Wise says businesses can receive payments in 24 currencies, create invoices and payment links, and make global payments. Its page also states that 70% of transfers arrive in 20 seconds and 95% arrive in under 24 hours, depending on transaction circumstances.

Best for: Microbusinesses, freelancers, creators, contractors, and global teams that want a stablecoin-based dollar account without traditional bank onboarding friction.

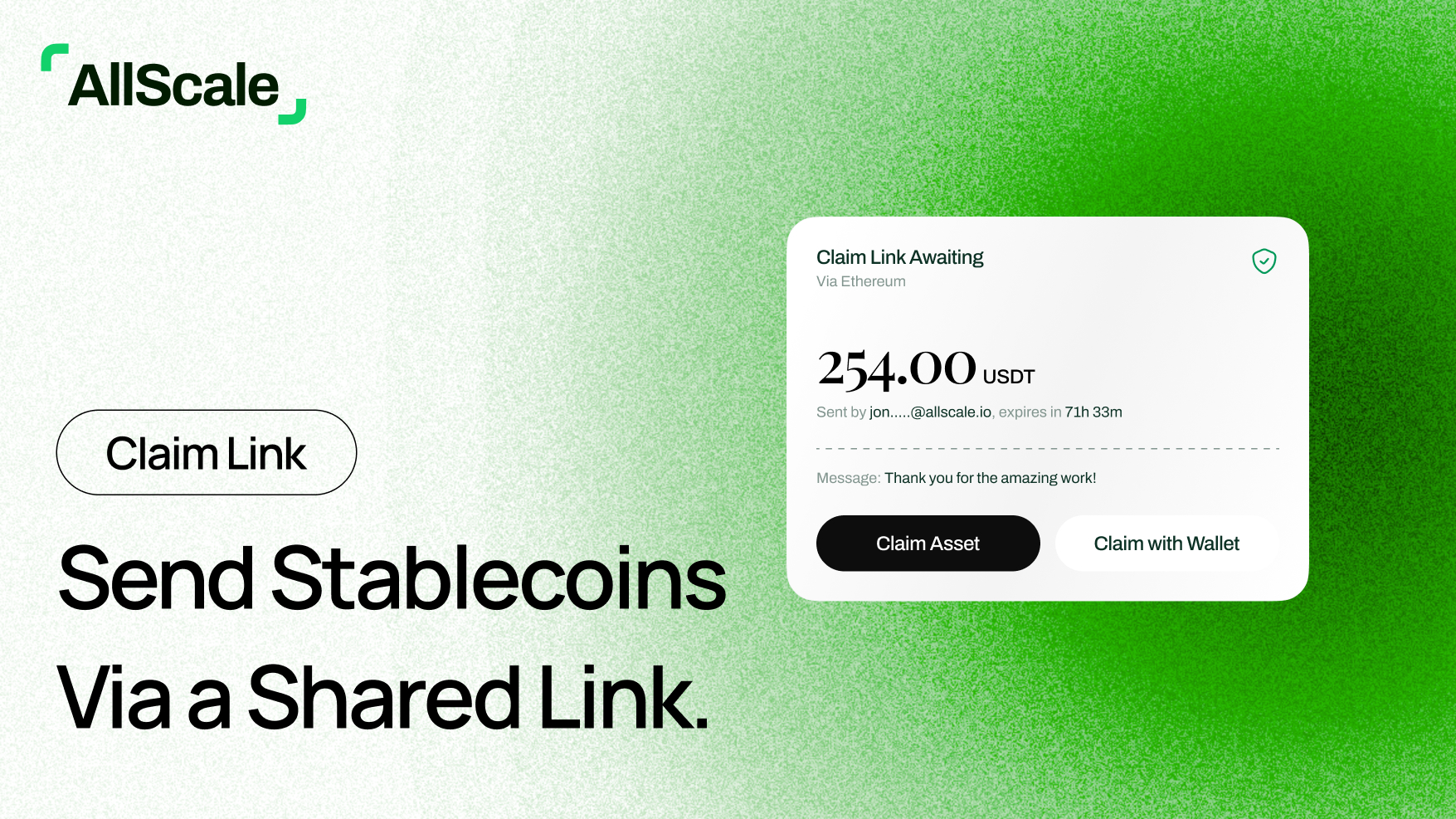

AllScale deserves a high ranking because it addresses a specific pain point that conventional fintech platforms do not always solve: small global businesses need a fast way to receive dollar-denominated value across borders without waiting for traditional banking applications or forcing clients into complex crypto workflows. On the AllScale Pay introduction, the product is positioned as a self-custody neobank for micro businesses, with messaging around getting a global dollar account in seconds, without bank applications, seed phrases, or borders.

The product flow is simple. A business signs up, creates payment links for clients anywhere, and gets paid in USDT or USDC. A particularly important detail is that AllScale says clients do not need an AllScale account or a crypto wallet to pay, while the business receives stablecoin settlement. That makes the platform compelling for globally distributed microbusinesses that want digital-dollar settlement but do not want to explain wallet setup, seed phrases, or crypto UX to every client.

AllScale is not a direct replacement for every bank account, payment processor, or merchant acquirer. Its own site notes that AllScale is a financial technology developer, not a bank, and does not provide digital asset custodian services. That distinction matters. For the right user, however, AllScale can be the modern cross-border layer sitting between invoicing, digital-dollar settlement, and global payouts. This makes it an incredibly cost-efficient alternative to traditional banking rails, especially when factoring in the transparency of AllScale pricing.

Best for: Growing SMBs that want a broader global finance stack rather than a standalone transfer tool.

Airwallex is best suited for SMBs that need international payments, local collection, business accounts, spend management, and financial operations on one platform. The Airwallex U.S. homepage presents the company as a global payments and financial platform used by more than 200,000 companies, with products spanning global business accounts, payment acceptance, company spend management, billing, and platform APIs.

The platform’s strongest advantage is breadth. Airwallex highlights local bank details, local-currency acceptance, multi-currency wallets, interbank FX rates, high-speed transfers, and a proprietary local payments network. Its homepage says businesses can collect funds like a local in 70+ countries, make local transfers to 120+ countries, accept payments from 180+ countries, and process more than $235 billion in global payments annually.

Best for: Marketplace sellers, freelancers, agencies, and SMBs that need to get paid through platforms and international clients.

Payoneer has long been associated with global freelancer and marketplace payments. On its business payment services page, Payoneer says every account includes services and tools to simplify work with global clients, contractors, and suppliers. The same page describes coverage across 190+ countries and territories and 70 currencies.

The platform is particularly strong for businesses that operate through marketplaces. Payoneer says it integrates with 2,000 marketplaces, networks, and platforms, including Wish, eBay, Airbnb, Fiverr, and Upwork. If your SMB revenue comes from platforms, affiliate networks, marketplaces, or global clients that already use Payoneer, it can be a practical default.

Best for: Ecommerce, SaaS, subscriptions, marketplaces, and developer-led SMBs selling globally online.

Stripe is not merely an international transfer provider. It is a global payment processing platform built for online commerce. On the Stripe Payments page, Stripe says businesses can accept payments online, in person, and around the world, sell cross-border to 195+ countries, and reduce multicurrency management complexity. The page also references flexible cross-border options in 195 countries across 135+ currencies, local acquiring coverage in 46 markets, global payment methods, Adaptive Pricing, and multi-currency settlement.

For an SMB that wants to sell to customers internationally, Stripe may be more important than a transfer app. It can support checkout, payment links, subscriptions, fraud prevention, authorization optimization, and local payment method presentation. The trade-off is that Stripe is strongest when the primary use case is accepting customer payments, not simply paying a supplier invoice overseas.

Best for: SMBs that need familiar checkout, invoices, payment links, and buyer trust quickly.

PayPal remains one of the easiest names for customers to recognize at checkout. On its business payments page, PayPal says PayPal Open helps businesses get paid online, in person, and on the go. It also highlights customer choice through PayPal, Venmo, Pay Later, debit and credit cards, and more, while referencing access to up to 400 million users.

For small businesses, PayPal is attractive because it can be deployed quickly through invoices, payment links, ecommerce integrations, or online checkout. It is especially useful when buyer familiarity matters more than lowest-cost FX. The downside is that international transaction and currency conversion fees can add up, so businesses with high-volume cross-border payments should compare PayPal carefully against Wise, Airwallex, OFX, and AllScale.

Best for: SMBs that want international transfers, business accounts, cards, and expense tools in one finance app.

Revolut Business is strongest for companies that want a modern business account experience paired with global transfers and spend controls. On its U.S. page for Revolut Business international transfers, Revolut says companies can transfer money in 25+ currencies to 150+ destinations. The same page emphasizes fast transfers, exact-amount transparency, global visibility, and lower-cost payment workflows through customer testimonials.

Revolut is a practical fit for startups, agencies, and lean finance teams that want business cards, expenses, account controls, and international transfers together. However, its allowances and fees depend heavily on plan, country, currency, and usage, so it is best evaluated against your monthly payment volume.

Best for: SMBs that make supplier payments, manage FX exposure, and need batch payment controls.

OFX is a strong choice for businesses that care about supplier payments, recurring international transfers, and FX risk management. The OFX international business payments page says companies can pay suppliers in 30+ currencies and 180+ countries, schedule recurring payments, and send, receive, and track cross-border payments.

OFX is particularly relevant for importers, ecommerce brands, wholesalers, and SMBs paying international suppliers. It offers multi-currency accounts, batch transfers, QuickBooks and Xero integration, multi-layer approval workflows, payee verification, and specialist support. The platform also emphasizes its 25+ years in secure global payments, FinCEN registration, and ISO 27001 certification.

Best for: SMBs that want payables and receivables automation across domestic and international payments.

Veem positions itself as a one-stop shop for domestic and international payables and receivables. On the Veem homepage, the company describes coverage across 100+ countries and 80+ currencies, along with more than 1.5 million users. It also includes SMB-friendly workflow features such as payment scheduling, mass pay, payment tracking, accounting integrations, approval workflows, payment requests, invoices, pay links, guest pay, and global card acceptance.

Veem is a good fit for businesses that want a workflow tool around payments, not just a transfer quote. It can be especially useful for finance teams that need to automate receivables, schedule recurring payments, track payment status, and sync with accounting software. The key consideration is whether Veem’s payment rails and fees are the best match for your specific currencies and counterparties.

A practical shortlist is usually better than trying every provider. Most SMBs should choose one primary platform and one backup rail, especially when payments are business-critical.

The best overall solution for many SMBs is Wise Business because it is transparent, easy to understand, and strong for international transfers, multi-currency receiving, and batch payments. However, the best choice depends on your model. AllScale is a strong fit for microbusinesses and global teams that want stablecoin dollar settlement, Airwallex is stronger for all-in-one global finance operations, and Stripe is usually best for global online checkout.

The cheapest option depends on the currency pair, payment rail, amount, destination, and urgency. In many cases, specialist fintech providers such as Wise, Airwallex, OFX, Revolut Business, and Veem can be cheaper than traditional bank wires because they are designed around international transfers and FX transparency. For recurring payments, SMBs should compare the total landed cost, including transfer fees, FX markup, intermediary fees, recipient fees, and accounting time.

When exploring options for cross-border payments with stablecoins, companies must weigh the operational efficiencies against regulatory requirements. Stablecoin payments can be useful for cross-border business payments when a company wants fast digital-dollar settlement and counterparties operate across banking systems. AllScale’s model is relevant here because it focuses on USDT/USDC settlement while simplifying the client-side payment experience. However, stablecoins are not risk-free. Businesses should review accounting treatment, tax obligations, wallet controls, jurisdictional compliance, and volatility or depegging risk before relying on stablecoins for critical cash flow.

Wise is often better for direct international transfers, multi-currency receiving, and transparent FX comparisons. Payoneer is often better for marketplace sellers, freelancers, and businesses that rely on platform payouts because its business payment services are built around marketplace integrations and global receiving. If your clients pay by bank transfer, Wise may be simpler. If your revenue comes from marketplaces or freelance platforms, Payoneer may be more convenient.

Stripe is both a global payment processor and a cross-border commerce platform, but it is strongest as a payment gateway and checkout infrastructure for online businesses. Stripe’s payments platform supports cross-border selling, local payment methods, local acquiring, fraud tools, and multi-currency settlement. It is ideal for ecommerce and SaaS, but less ideal as a simple replacement for supplier wire transfers.

SMBs should check whether the provider supports their exact sending and receiving countries, whether they can hold or only accept foreign currencies, what the real FX markup is, how fast payments settle, what happens when a payment fails, and whether the platform integrates with accounting software. Businesses should also review compliance status, customer support coverage, dispute handling, security controls, and whether the provider’s strengths match their workflow.

For most small businesses, Wise Business is the most straightforward starting point for transparent international transfers. AllScale is the most interesting option for microbusinesses and global teams that want a stablecoin-based dollar account and payment links without client-side crypto friction. Airwallex is the strongest choice when you need a broader global finance platform, while Stripe and PayPal remain important for online checkout and buyer-facing payments.

For companies looking to cut FX fees with stablecoin payments, optimizing traditional banking alternatives is often the first step in financial restructuring. The best approach is to map your payment workflow before choosing a provider. If your pain is FX cost, compare Wise, Airwallex, OFX, and Revolut. If your pain is client collection, compare AllScale, PayPal, Veem, and Stripe. If your pain is marketplace payouts, start with Payoneer. The right cross-border payment solution should not just move money internationally; it should make your business easier to run.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.