The limitations of traditional finance have made stablecoins a highly anticipated force for change, poised to drive a financial revolution. However, the deeply ingrained legacy systems of traditional finance—what we call Path Dependence—pose a significant challenge. Fear of Missing Out, or FOMO, is a common anxiety that others will have a beneficial experience when one is absent. This sentiment is now brewing in the stablecoin market, and we believe it is the only way to break through the path dependence of traditional finance.

This article will analyze the Path Dependence problem in traditional finance (TradFi), highlight the potential of stablecoins as a blueprint for a modern financial system, and demonstrate how FOMO can accelerate this transformation. We’ll look at historical examples, from the shift to electricity and natural gas to the transition from carriages to trams.

Think of TradFi as an old city, its infrastructure largely built in the 1970s. The systems it relies on are outdated: SWIFT for cross-border communication, ACH for bank transfers, and card networks that are over 60 years old. These systems are like the old city's brick walls, with every bank and institution embedded within them. Regulations are the cement holding it all together, and trillions of dollars flow through these dilapidated pipes every day. The world outside has changed dramatically, but those inside this antiquated fortress remain indifferent.

Traditional finance is considered a broken-down city because it relies heavily on centralized institutions like banks and clearing houses. This results in complex, slow, and expensive transactions that are vulnerable to failures and human error. Information asymmetry is high, and the barrier to entry is significant. In contrast, decentralized finance (DeFi) offers clear advantages. A closer look at history shows that the future is clearly on DeFi’s side.

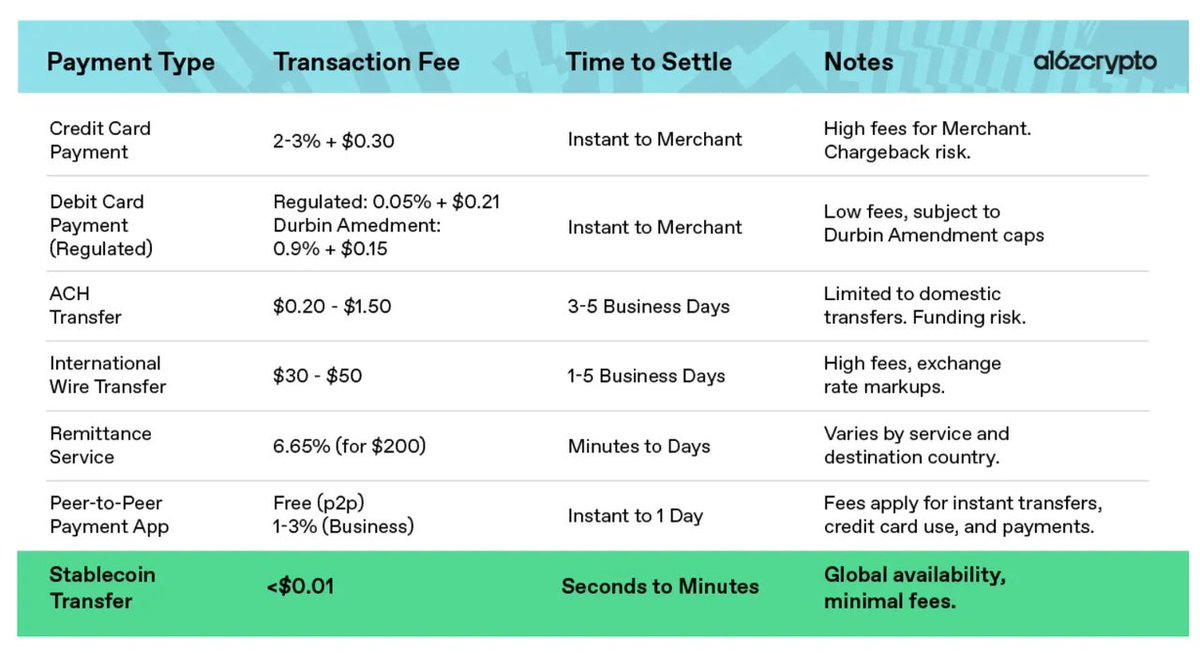

Traditional bank transfers often take a long time. International wire transfers via the SWIFT system can suffer settlement delays of 2-5 days or even longer, requiring careful liquidity management. A critical flaw is the inability to operate 24/7; financial transactions don’t take holidays. The Fedwire system in the U.S., for instance, requires non-working-day transactions to wait until the next business day, severely limiting liquidity and creating major headaches for businesses.

Stablecoins, built on blockchain technology, can achieve near-real-time settlement. For example, Visa's experiment on the Solana blockchain showed settlement times as low as 400 milliseconds. Even on slower networks, stablecoin transfers are typically completed within minutes and operate 24/7. This immediacy drastically improves capital efficiency, a huge advantage for global businesses and individuals who need to make transfers across time zones or during non-traditional business hours.

Traditional finance has many intermediaries who profit from the transaction spread. From banks to foreign exchange dealers to card networks, every step acts like an ancient border checkpoint, where funds are intercepted and charged a “clearance fee.” According to a World Bank report from September 2024, the global average remittance cost is 6.62%. In some regions, these costs are even higher.

From this chart, we can see the comparison of the transaction costs of using cash and electronic transfers in different regions around the world. Horizontal comparison between regions shows that transaction costs are high in sub-Saharan Africa, inland countries in Europe and Asia, etc. Vertical comparison of different transaction methods shows that electronic transaction settlement significantly reduces transaction costs compared to cash settlement. However, we have to admit that this decades-old transaction system is still too inefficient. We urgently need a new transaction system represented by stablecoins to achieve low-cost fund transfer and settlement.

When stablecoins are used, the situation changes dramatically. They use blockchain to cut out the middlemen, and transaction fees are usually just a few cents on an efficient network. For cross-border e-commerce, remittances, or B2B trade, stablecoins can reduce costs from 5–7% to around 0.1%, significantly boosting economic efficiency.

Stablecoins have the potential to reach populations that traditional finance has long excluded. Traditional banking requires robust infrastructure and identity verification, leaving an estimated 1.4 billion unbanked adults globally without basic financial services. Opening a bank account requires a credit history, identity documents, and physical access—all of which are major hurdles for people in remote or economically disadvantaged areas.

Stablecoins, however, only require an internet connection and a smartphone. This offers a "mobile banking" solution for the unbanked, especially in regions with high inflation or currency instability. Stablecoins are becoming a secure tool for U.S. dollar savings and remittances. MoneyGram has partnered with Stellar, for example, to let users in Africa and Latin America receive remittances in USDC, drastically cutting costs and time.

In sub-Saharan Africa, stablecoins have become the largest asset class since 2022. Due to the lack of traditional financial infrastructure and the risk of local currency inflation, more people are using stablecoins to store value. If we broaden our perspective, we’ll find that many of the unbanked are potential stablecoin users.

Given all these advantages, why haven't stablecoins replaced your bank account? They are major players in crypto trading and niche scenarios but are still on the fringe of mainstream finance.

The biggest hurdle for stablecoins is the uncertainty of regulation. Financial institutions are hesitant to invest due to concerns about unclear rules. In the U.S., stablecoin issuers often rely on state licenses, operating in a regulatory "gray area" that discourages banks from integrating these services.

However, the regulatory fog is beginning to lift. The GENIUS Act in the U.S. and MiCA regulations in Europe are establishing clear rules, requiring 1:1 reserves and regular disclosures. Ninety percent of companies in the sector believe this is a catalyst for large-scale adoption. The clarification of regulation is a vital first step, especially for bringing financial services to those excluded by the traditional banking system.

Even with clearer regulations, the inertia of traditional financial institutions remains a major roadblock. The systems banks and corporations rely on are outdated and complex. Integrating stablecoins isn’t a simple flip of a switch; it requires system upgrades, employee training, and a fundamental shift in mindset. This path dependence makes institutions more likely to stick with the old system until a truly compelling reason forces them to change.

Furthermore, traditional finance profits handsomely from fees on wire transfers, foreign exchange spreads, and card payments. Giving up this profitable business model is a difficult choice. This creates a "chicken-and-egg" problem: the value of stablecoins is only apparent with widespread adoption, but institutions and users are unwilling to be the first to take the risk.

A former Visa executive admitted that payment companies see stablecoins as a "strategic necessity" and fear being overtaken by new crypto giants. But there is a huge gap between wanting to act and actually acting. To achieve their full potential for financial inclusion, stablecoins need the pressure of competition and FOMO to drive action.

The foundation of any financial service is trust, and this is another high wall built by the traditional system. As an emerging tool, stablecoins have yet to fully win the confidence of non-crypto users. The collapse of Terra UST in 2022, which saw $60 billion evaporate, cast a long shadow. Although fiat-backed stablecoins like USDC and USDT are fundamentally different from algorithmic coins, the negative impression has scared many people away.

The good news is that USDC and USDT have withstood major redemption events, and new regulations (like mandatory liquidity reserves) are building a foundation of trust. However, brand still matters. Stablecoins launched by JPMorgan or PayPal are naturally seen as more credible. This is a crucial point: "big-brand endorsement" can significantly lower the trust barrier and encourage more people to try them, especially in regions where traditional banking is out of reach.

The infrastructure of the traditional financial system is complex and closed, but stablecoins have also faced their own technical integration challenges. In the early days, they weren't "Plug and Play." How do you manage private keys? How do you connect on-chain transfers to legacy systems? These issues were major obstacles, especially for smaller institutions.

Fortunately, technological progress is closing this gap. The maturity of enterprise-level custody and compliance tools (like Fireblocks and Coinbase Custody) has made stablecoin operations safer and more compliant. In 2024, 86% of companies reported that their infrastructure was ready to move from pilots to full-scale implementation.

Merchant demand is strong, infrastructure is maturing, and regulations are clearing. The technical debt has been largely paid; what remains is a "willingness debt" that needs a stronger impetus. For developing countries, stablecoins, with their low-entry barriers, are the bridge connecting the unbanked to financial services.

Finally, there’s the “last mile” problem: public unfamiliarity. The high barrier of traditional finance has made many people accustomed to being excluded. Stablecoins still feel "hardcore" to non-crypto users. The industry is working hard to simplify the user experience, making it closer to traditional finance. PayPal, for example, embeds PYUSD into its app, allowing users to transfer money without understanding blockchain technology. However, if there aren’t enough places to spend stablecoins, why should people switch? This network effect dilemma needs to be broken.

In the history of technological revolutions, new innovations often violently displace old, outdated ones. FOMO, the fear of missing out, measures this shift. It changes the core question from "Why should we enter this game?" to "Can we afford not to?"

Historically, FOMO has proven to be a powerful demolition crew. The internet boom of the late 1990s is a classic example. Companies rushed to build websites not because they had a clear digital strategy, but because they were terrified of becoming obsolete. They feared missing out on the future, and their frenzied investment quickly laid the foundation for the digital world we know today.

The transition to electricity is another case. In the 19th century, urban lighting relied on gas lamps, with a deeply entrenched infrastructure of pipelines and regulations. When electric light emerged, it was expensive and unstable. Yet, many cities and companies invested heavily in building power grids, fearing they would miss out on a brighter future. This FOMO-driven investment rapidly popularized electricity and sent gas lamps into the dustbin of history. The transition from carriages to automobiles and from city gas to natural gas followed a similar pattern. These examples show that FOMO can break the chains of path dependence and forcefully push technology forward.

Some fintech companies are already reaping the rewards of stablecoins, lighting the fuse of competition. Tether and Circle, which issue USDT and USDC, have seen their market caps skyrocket. Companies like Stripe and Revolut are using stablecoins to offer faster, cheaper services. Stripe supported USDC payments in 2023, and Revolut uses stablecoins to help customers save on massive foreign exchange fees. These companies are getting a head start in the global market.

The entry of major institutions signals that the FOMO is becoming undeniable. PayPal launched PYUSD in 2023, becoming the first mainstream payment company to create its own stablecoin. PayPal is now actively promoting PYUSD, using its Xoom service for international remittances and offering holders a 3.7% annualized return. If PYUSD succeeds, will other payment giants sit by and watch PayPal dominate?

This is why we see other major players preparing: Visa and U.S. banks are developing stablecoin plans, and Standard Chartered has launched a Hong Kong dollar stablecoin. Even governments are contributing to the FOMO. U.S. policymakers have suggested that stablecoin legislation could "maintain the dominant position of the U.S. dollar," showing that even the government doesn't want to miss out on the digital dollar future.

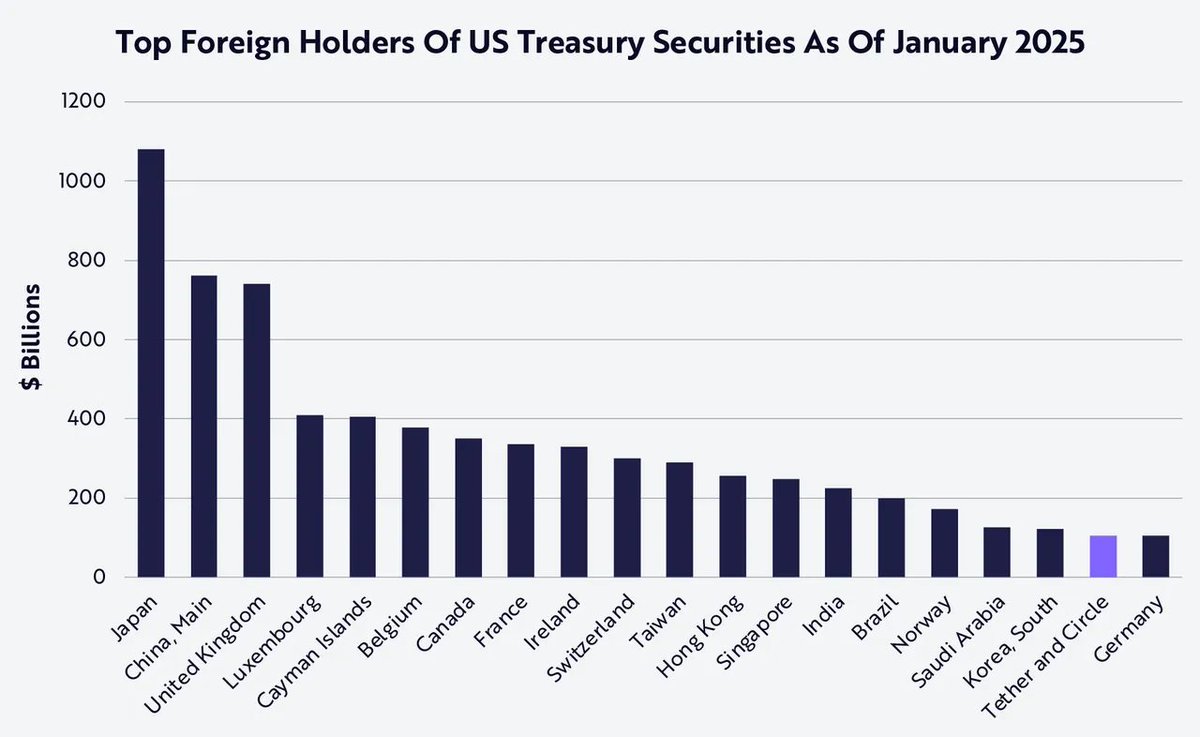

The market value of stablecoins continues to hit new highs, with USDT and USDC now holding over $200 billion in U.S. Treasury bonds, making them the 14th largest holder in the world. This has made traditional finance uneasy. Stablecoin companies have become "systemic players," essentially operating as digital dollar banks. The rapid rise of PayPal's PYUSD, with a circulation of over $1 billion in under two years, shows that big-brand endorsements are legitimizing stablecoins.

All signs point to a familiar story. Stablecoins are moving from the fringes of DeFi to the center of finance, with major companies entering the market, users showing interest, and regulators giving their nod. We may be standing on the verge of the stablecoin boom, much like the internet in 1995.

With good technology, practicality, big brand support, and clear regulations, the outbreak point of stablecoin FOMO seems to be right in front of us. The traditional financial path dependence is a stubborn but dismantling old wall, and history has proven that external forces from FOMO can accelerate demolition. The arrival of FOMO’s frenzy may be accompanied by the following phenomena.

Just like today, Apple Pay and PayPal have become the norm. In the near future, the investment frenzy of stablecoin FOMO will make stablecoin support a standard for software and platforms. “Accepting USDC/USDT” will also become the default option for Payment Processor, e-commerce, payroll systems, and banks. However, it must rely on the iterative update of infrastructure based on area, just as new energy vehicles replace traditional energy vehicles, which require not only technological advantages and policy support, but also large-scale infrastructure such as charging piles. FOMO-driven investment will build a “connecting bridge” to reduce the joining costs of small players and latecomers. Stablecoins have become the core pipeline, and users may not know that they are using it in the background, only feeling that it is faster and cheaper. This is particularly important for the unbanked — the spread of infrastructure will enable Financial Services to reach every corner of the world.

It may be difficult for the establishment to give up the interests of traditional finance, but perhaps the compromise solution is to adopt officially recognized stablecoins, which are stablecoins with semi-centralized properties. The ultimate victory is that stablecoins are no longer seen as “crypto freaks”, but become digital money for traditional finance. Interbank settlement may use regulated stablecoins and CBDC/reserve account networks. US banks transfer reserves to stablecoins recognized by the Federal Reserve overnight, which are quickly delivered to Asian partners without the need for slow proxy chains. Exchanges use “settlement coins” to instantly clear transactions.

If stablecoins are on par with ACH, Fedwire, and SWIFT and become “ordinary channels” for bank backends, Path Dependence will be completely shattered. This may be achieved through cooperation: banks do not trust external stablecoins, but will support the alliance’s “utility settlement currency”. Once the boundaries are blurred, stablecoins will become “digital dollar 2.0”

Taking PYUSD launched by PayPal as an example, it is published by Paxos Trust Company and regulated by the New York State Department of Financial Services (NYDFS). PYUSD is embedded in the payment ecosystems of PayPal and Venmo, allowing users to seamlessly transfer, pay, or hold, with an experience no different from traditional finance. At the same time, the background is based on the Ethereum blockchain for instant settlement. This is a typical regulated semi-centralized stablecoin, which is not independent of the traditional financial system, but integrated into existing payment systems (such as ACH) to provide consumers and merchants with a low-cost and instant settlement experience.

Similar semi-centralized cases include mBridge. This is a batch CBDC project initiated by the People’s Bank of China (PBOC), HKMA, and others, which realizes cross-border interbank settlement based on distributed ledger technology (DLT). In 2024, mBridge completed the pilot and supported real-time cross-border transfer in digital RMB (e-CNY) and Hong Kong Digital Hong Kong Dollar (e-HKD), with transaction costs as low as 0.1%, far lower than SWIFT’s 6% -10%.

Powerful sovereign countries will accept semi-centralized compromise solutions and use them as important pawns for the internationalization of their own currencies. Countries and regions that rely on the US dollar system will also embrace stablecoin payments and settlements due to their own transaction cost interests. With the arrival of FOMO, stablecoins will be increasingly accepted and familiar to more and more people.

The widespread adoption of stablecoins is reshaping the global monetary landscape. The US dollar achieves permissionless global reach through stablecoins, maintaining its hegemony. Other countries may launch their own fiat currencies (such as digital euros and the expansion of the RMB ecosystem through corporate stablecoins). This competition will trigger global FOMO: countries are afraid of currency loss and rush to launch tokenized forms. Hong Kong tests e-HKD, and Japan legalizes some stablecoins. The end result may be that each major currency has an interoperable stablecoin, jointly published by the government and private enterprises, running on blockchain and Layer-2, and the currency truly becomes “borderless programmable”. If financial institutions are not prepared, they will not be able to become the “big players” of future finance.

The revolution of stablecoins is advancing, but the Path Dependence of traditional finance (TradFi) remains a huge obstacle. History has shown that FOMO (fear of missing out) has played a key role in technological change, such as the transformation of electricity, natural gas, and transportation. Today, stablecoins also need the promotion of FOMO, and it is the only way to solve the Path Dependence of traditional finance. Only the competitive pressure and investment boom brought by FOMO can break the inertia of the old system and move stablecoins from the edge to the core. For investors and builders of financial technology, now is the last chance for change. Stablecoins are not only technological innovation, but also tools for achieving financial inclusion, providing services for people without bank accounts. The FOMO wave is forming, and the era of stablecoins is coming.

The future has arrived, but it is unevenly distributed.

[INVESTMENT DISCLAIMER]

Investing involves risks. This information is not investment advice or a recommendation to buy, sell, or hold securities. Readers should assess their financial situation and risk tolerance before making investment decisions. We are not liable for decisions based on this information.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.