Stablecoins are cryptocurrency tokens designed to maintain stable value through collateralization with reserve assets, typically fiat currencies or other stable instruments. Unlike volatile cryptocurrencies such as Bitcoin, stablecoins function as digital cash equivalents, serving as a bridge between traditional finance and decentralized protocols. As Jenny Zheng noted during the panel discussion, stablecoins operate on a full-reserve banking model with 100% asset backing and no fractional lending capabilities, positioning them as reliable settlement instruments rather than credit instruments.

Currently, stablecoin adoption spans three primary market segments:

Stablecoins serve as the primary quote currency and risk-off asset within crypto markets. During bear markets, traders utilize stablecoins for capital preservation; during bull markets, they enable profit-taking without off-ramping to traditional banking rails. For instance, when Bitcoin experiences high volatility, institutional and retail traders can rotate into stablecoins to maintain crypto exposure while avoiding price risk. This eliminates the friction of converting to fiat through traditional banking channels, reducing settlement time from days to minutes and minimizing counterparty risk with legacy financial institutions. Stablecoins effectively function as the native base money of the crypto economy, serving both as a unit of account and medium of exchange. By transaction volume, this represents the largest current use case for stablecoins globally.

Chiyao Huang highlighted that cryptocurrency exchanges face significant banking challenges due to de-risking policies and regulatory uncertainty, making stablecoins essential "tokenized dollars" that bypass traditional correspondent banking networks. This infrastructure enables exchanges to operate with reduced dependency on traditional banking rails while maintaining USD exposure. For example, Circle maintains a strategic partnership with Coinbase, with Coinbase receiving approximately $900 million in revenue share fees in 2024—representing 54% of Circle's total revenue. This stems from Coinbase's deep integration of USDC across its ecosystem, including its Base Layer-2 network and custodial wallet infrastructure, which provides yield opportunities for USDC holders. Coinbase's platform now holds 23% of total USDC supply as of Q1 2025, up from 5% in 2022. This symbiotic relationship demonstrates how stablecoin issuers require exchange distribution channels for liquidity and compliance infrastructure, while exchanges need stablecoins as settlement rails to enhance user engagement and revenue diversification.

Stablecoins demonstrate significant advantages over traditional correspondent banking networks for international value transfer. The SWIFT messaging system suffers from multi-day settlement times, high intermediary fees, and susceptibility to geopolitical disruption—as demonstrated during the Russia-Ukraine conflict when Western sanctions effectively excluded Russian banks from SWIFT networks. Stablecoins enable 24/7 real-time settlement with programmable compliance and significantly lower transaction costs compared to traditional remittance corridors.

For unbanked and underbanked populations globally, along with those in high-inflation economies, stablecoins provide critical financial infrastructure. Applications include daily commerce, cross-border trade finance, and SME payroll processing—representing massive addressable markets with limited incumbent penetration.

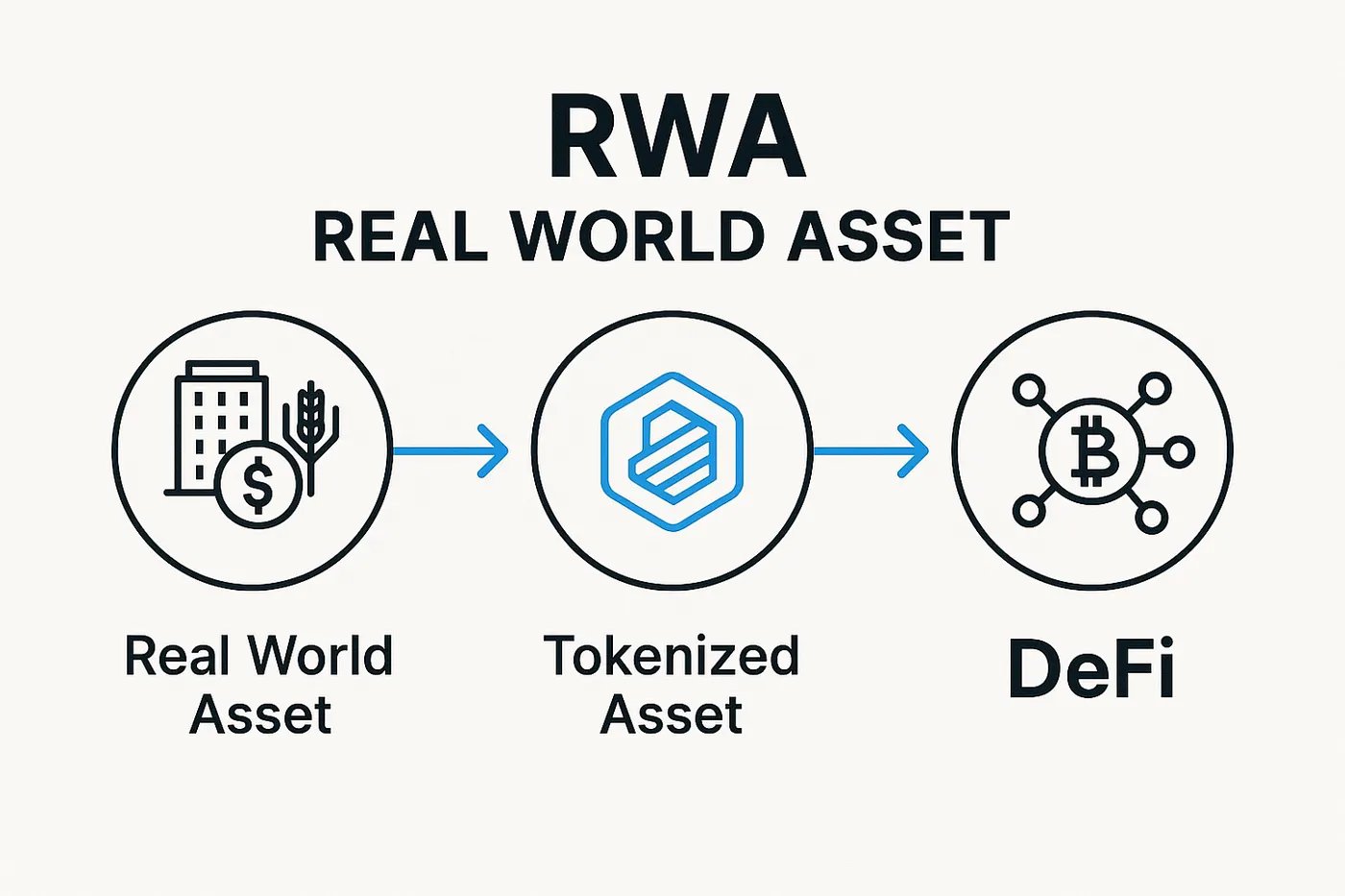

Stablecoins serve as the primary settlement currency for tokenized real-world assets, facilitating the digitization and fractionalization of traditional asset classes including real estate, commodities, and alternative investments. Similar to REITs in traditional finance, on-chain RWA protocols enable global investment access with stablecoin-denominated yield distributions. Platforms like RealT and Propy allow fractional real estate investment through stablecoin purchases, with rental income distributed as stablecoin yields. RWA tokenization also addresses distressed asset resolution and represents a natural evolution of asset securitization into programmable, composable formats.

Hong Kong's regulatory framework represents a strategic proving ground for RMB-denominated stablecoin experiments, with implications for broader digital yuan internationalization efforts. Jenny emphasized Beijing's growing interest in stablecoin infrastructure, driven by competition with US dollar hegemony and the need to modernize cross-border payment rails. The US GENIUS Act provides regulatory clarity for USD stablecoins, and China seeks to avoid technological dependence in Web3 financial infrastructure. Governor Pan highlighted at the Lujiazui Forum that traditional correspondent banking suffers from inefficiency and geopolitical constraints, positioning RMB stablecoins as potential solutions for enhanced cross-border settlement.

However, RMB stablecoin development faces significant structural challenges. Mainland China's crypto trading restrictions require offshore issuance, while limited offshore RMB liquidity constrains reserve asset diversity. The market remains USD-dominated due to superior liquidity and established network effects.

Hong Kong's Stablecoin Licensing Ordinance provides regulatory flexibility by not mandating specific fiat currency pegs (USD, HKD, or RMB), creating optionality for multi-currency experiments. With approximately one trillion RMB in Hong Kong deposits, the territory offers sufficient reserve asset depth for pilot programs. Jenny predicts Hong Kong will initially focus on USD and HKD stablecoins to build technical infrastructure and market confidence before introducing RMB variants.

The stablecoin ecosystem involves a number of participants, from issuers of stablecoins to managers of reserve assets, and from trading platforms to various users of the platform, each of which has potential beneficiaries. First, there are the issuers of stablecoins, such as Jingdong Coin Chain Limited, Roundcoin Innovations Limited, Standard Chartered Bank, On Proprietary Group and Hong Kong Telecommunications Consortium Group. These organizations are already one step ahead in terms of technology development and market layout.

Reserve management represents the critical operational layer ensuring stablecoin price stability and redemption guarantees. Custodial banks like HSBC and Bank of China Hong Kong provide qualified custody for backing assets, while specialized asset managers optimize yield-generating investments within regulatory constraints. Big Four audit firms including Deloitte and PwC provide attestation services and ongoing reserve verification, providing market confidence through third-party validation.

Layer-1 networks like Ethereum and emerging competitors serve as settlement rails for stablecoin transfers, while wallet infrastructure including MetaMask and Trust Wallet provides user interfaces. Payment processors and API providers build interoperability bridges between traditional finance and DeFi protocols.

Centralized exchanges like Coinbase and OKX, alongside decentralized protocols such as Uniswap and PancakeSwap, provide essential liquidity and price discovery mechanisms. Hong Kong-based brokerages including Futu Securities and Tiger Securities are expanding crypto asset capabilities, providing traditional brokerage-style services for digital assets. Professional market makers and authorized participants maintain price stability through arbitrage trading and liquidity provision, earning spreads while ensuring efficient markets. The exchange sector exhibits higher concentration than traditional brokerage markets, with more pronounced winner-take-all dynamics exemplified by Coinbase's USDC revenue concentration.

DeFi lending protocols like Compound and Aave utilize stablecoins for collateralized lending and algorithmic interest rate markets. E-commerce platforms increasingly accept stablecoin payments, particularly for cross-border transactions where settlement advantages are most pronounced. Corporate treasury adoption is emerging as forward-thinking enterprises utilize stablecoins for working capital management and international operations.

The ecosystem requires robust regulatory compliance infrastructure, with central banks developing oversight frameworks while legal and compliance service providers ensure regulatory adherence. AML/KYC service providers add operational costs but ensure ecosystem legitimacy and sustainability.

Rick Zhao highlighted ZhongAn Insurance and its subsidiary ZhongAn Digital's comprehensive stablecoin strategy, spanning issuance, custody, and retail distribution through virtual asset exchange partnerships. ZhongAn Bank, Asia's first digital bank with cryptocurrency trading authorization, maintains a 40% stake in Bank of Tianjin, potentially supporting future custody and payment applications.

Jenny noted that Hong Kong's regulatory sandbox participation doesn't guarantee licensing approval. Over 40 companies are preparing stablecoin license applications, but single-digit licenses are expected this year, prioritizing financially robust entities with proven operational capabilities.

Futu Securities represents a compelling case study, with substantial Hong Kong retail penetration, average customer assets exceeding HK$500,000, strong user retention, and 3.6% retail market share by trading volume. Futu's competitive advantages include integrated platform experiences, diversified investment products, and expansion into Singapore and Japanese markets. The company has accumulated multiple regulatory licenses including brokerage, exchange, and banking authorizations, expecting full cryptocurrency trading licenses by year-end. Futu maintains competitive fee structures and strong pricing power, warranting close industry monitoring.

While Hong Kong's stablecoin initiatives show promise, RMB stablecoin internationalization faces significant headwinds. Jenny identifies three primary constraints limiting near-term RMB stablecoin adoption:

Limited Reserve Asset Liquidity: Offshore RMB instruments including central bank bills and sovereign bonds remain limited in scale and accessibility, constraining issuer reserve diversification options.

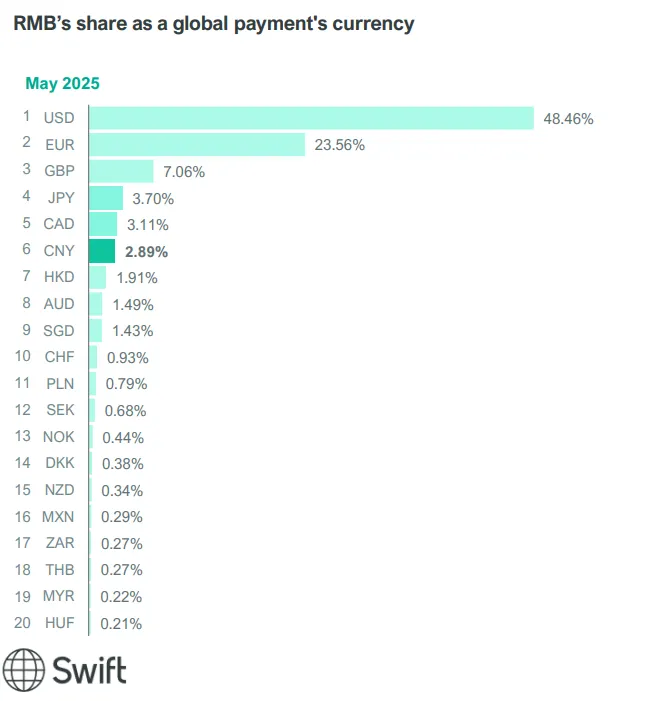

Broader RMB Internationalization Challenges: RMB stablecoins represent only one component of yuan internationalization strategy, with underlying asset attractiveness remaining paramount. RMB global payment share declined from 3% in 2022 to approximately 2% currently. While merchandise trade settlement has increased, this progress is offset by reduced international capital allocation to RMB-denominated assets.

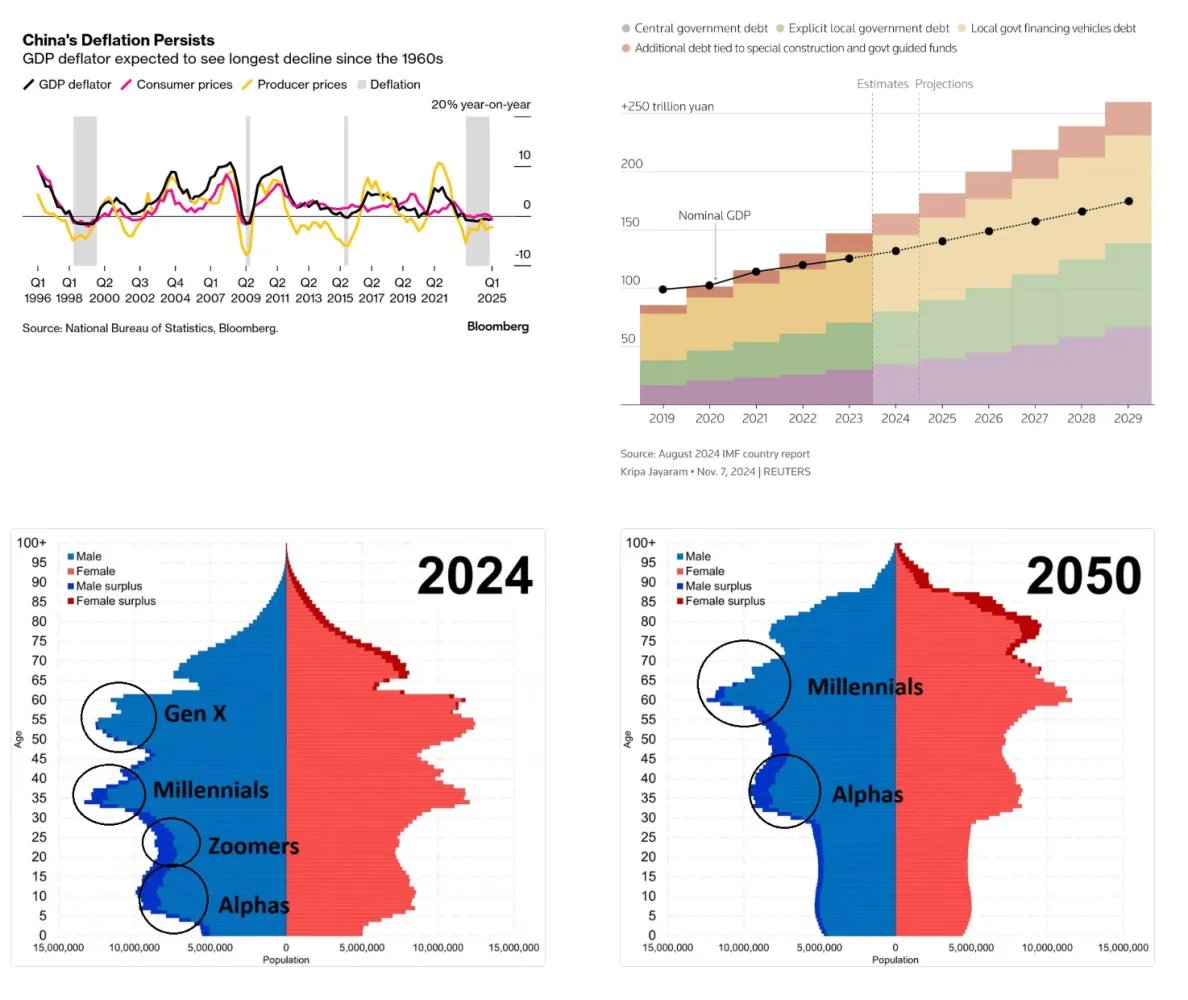

Macroeconomic Headwinds: China faces the "3D" challenge of Deflation, Debt, and Demographics, undermining investor confidence. Deflationary pressures persist into 2025, local government debt requires resolution, and demographic transition raises questions about productivity growth sustainability. Birth rate declines since the Alpha generation pose long-term economic challenges.

Successful RMB internationalization requires structural reforms addressing social welfare systems, debt restructuring, tax optimization, and business environment improvements. These reforms directly impact RMB asset attractiveness, creating necessary preconditions for stablecoin internationalization success.

Stablecoin proliferation generates structural positive effects on global equity market access and efficiency. The most immediate impact involves transaction efficiency improvements through reduced settlement friction. Traditional cross-border equity investment requires multiple currency conversions and banking intermediaries, creating time delays, high fees, and FX risk exposure. Stablecoins function as programmable dollars, enabling more direct global market participation with reduced counterparty risk and transaction costs. This efficiency gain particularly benefits investors previously excluded by minimum capital requirements and technical infrastructure barriers.

Stablecoins fundamentally redefine retail investor access by lowering global capital market participation barriers. Previously, Southeast Asian retail investors seeking US equity exposure faced offshore account requirements, high minimum deposits, and complex compliance procedures. Stablecoin infrastructure dismantles these barriers systematically. Interactive Brokers, a leading online brokerage platform, is exploring stablecoin deposit support for 24/7 instant funding and cryptocurrency integration, targeting improved capital efficiency and user experience. Hong Kong brokerages including Futu Securities and Tiger Securities actively expand crypto asset capabilities, responding to surging virtual currency trading demand that drove significant Q4 2024 volume growth.

Future regulatory liberalization and technological maturation will enable more convenient, cost-effective global market participation through stablecoin rails. This financial inclusion effect rapidly expands global equity investor bases, particularly in regions with underdeveloped traditional financial services including Southeast Asia, Sub-Saharan Africa, and Latin America, democratizing wealth-building opportunities for previously excluded populations.

Hong Kong's Stablecoin Licensing Ordinance implementation on August 1st marks a pivotal moment in bridging traditional finance and Web3 ecosystems. Stablecoins serve not only as crypto market infrastructure and settlement currency but also as potential catalysts for RMB internationalization. Despite challenges including reserve asset constraints, macroeconomic pressures, and regulatory uncertainty, Hong Kong's role as a regulatory testing ground provides valuable experimentation opportunities for RMB stablecoin development.

As a reform and opening-up pioneer with central government support and local government backing, Hong Kong embraces Web3 innovation while maintaining its position at the forefront of global financial evolution.

[INVESTMENT DISCLAIMER]Investing involves risks. This information is not investment advice or a recommendation to buy, sell, or hold securities. Readers should assess their financial situation and risk tolerance before making investment decisions. We are not liable for decisions based on this information.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.