Africa stands at a remarkable crossroads. The continent that leapfrogged landline telecommunications and jumped straight to mobile phones is now poised to skip traditional banking infrastructure entirely and embrace a new financial paradigm built on stablecoins. For companies looking to establish themselves in this rapidly evolving landscape, understanding this shift isn't just beneficial—it's essential.

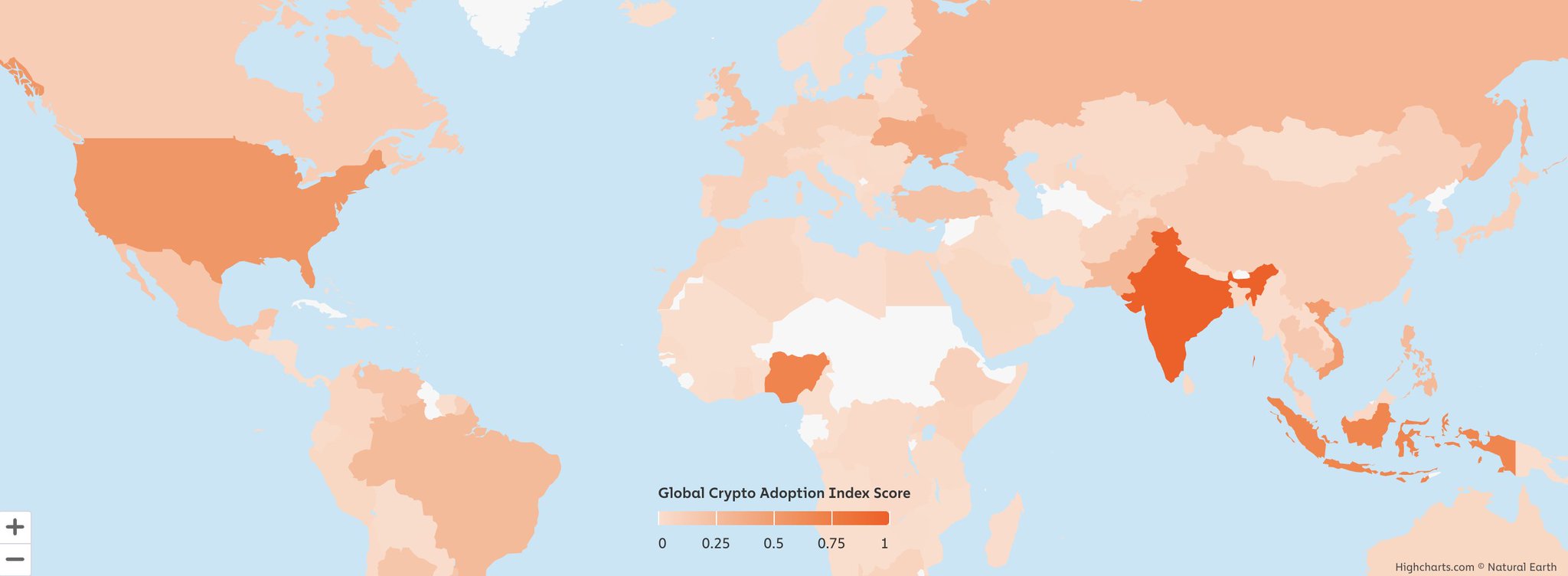

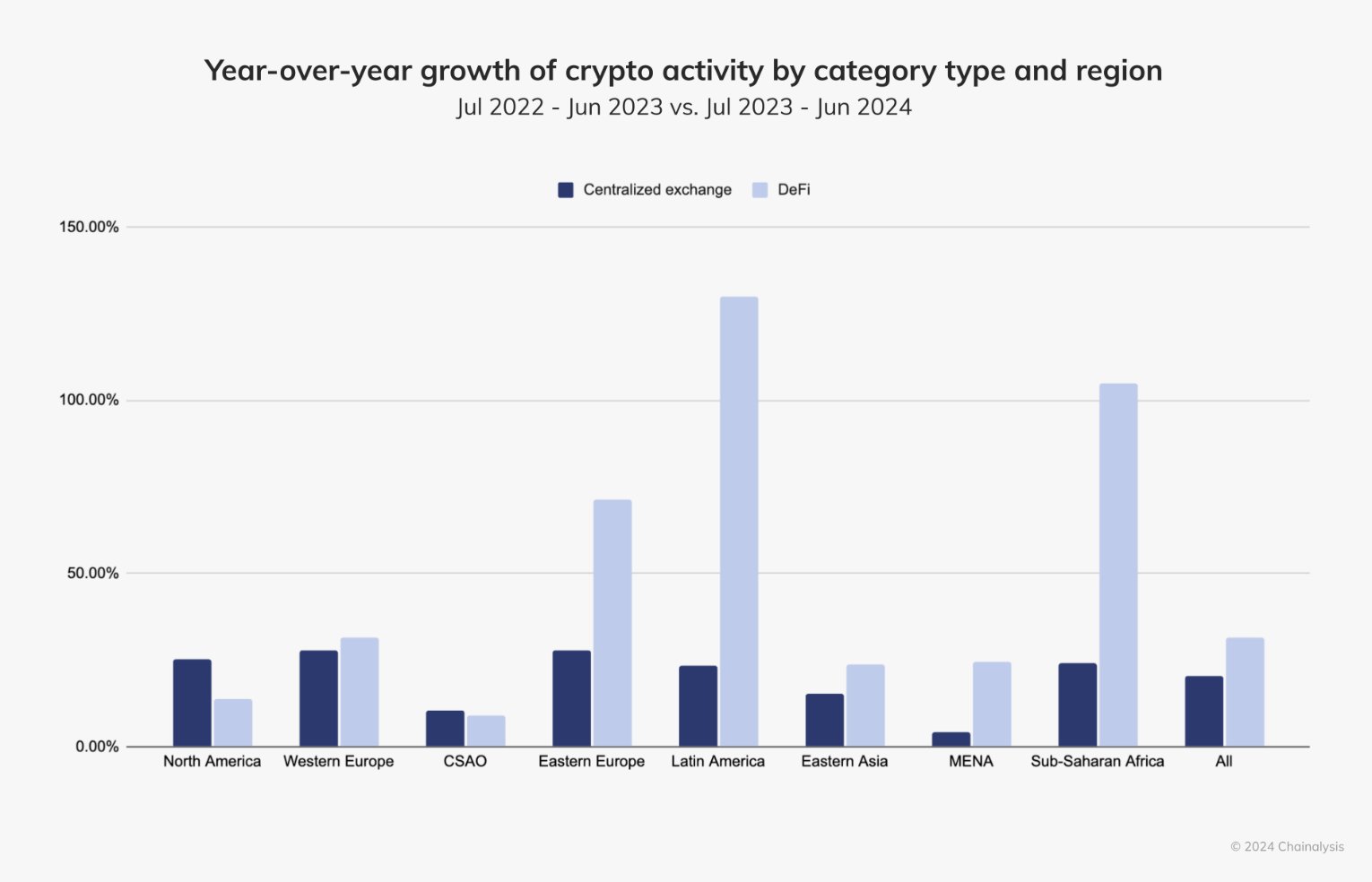

The numbers tell a compelling story. Africa has emerged as the fastest-growing region for cryptocurrency adoption globally, with a staggering 45% year-over-year growth rate from 2022 to 2024, according to Chainalysis. This outpaces even Latin America's impressive 42.5% growth rate. But what makes this particularly interesting is that unlike other regions where crypto activity is largely speculative, African users are turning to stablecoins for practical, everyday financial needs.

To understand why stablecoins are gaining such rapid traction in Africa, we need to examine the fundamental challenges with existing financial infrastructure. Traditional cross-border payment systems operate through two primary mechanisms, both of which create significant barriers for African users and businesses.

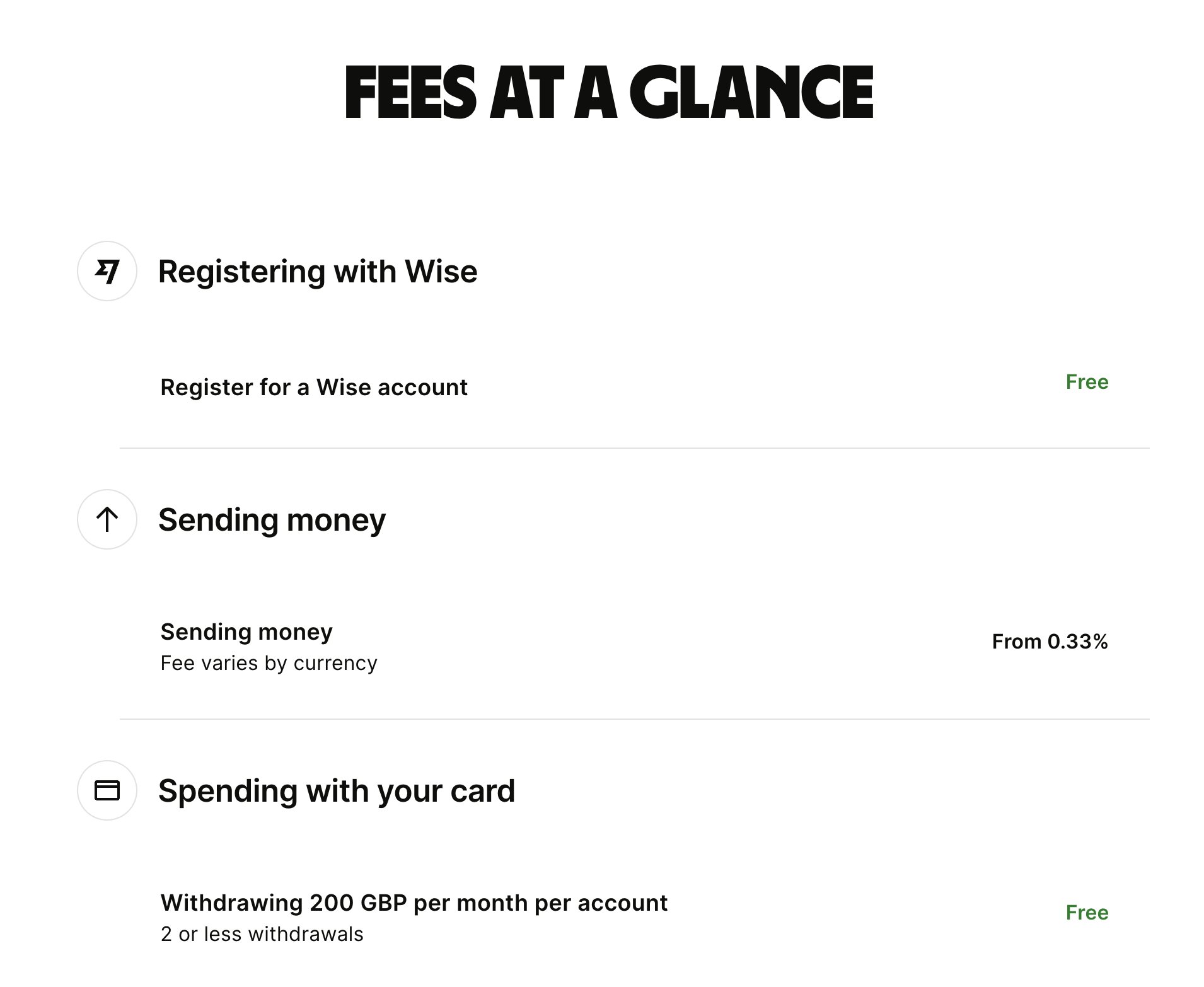

The first method involves netting-based payments, used by platforms like Wise and Remitly. These services maintain large cash reserves in multiple countries and simply adjust internal balances when transfers occur. While this can enable faster transfers, it requires companies to hold substantial capital in each market—something that becomes extremely challenging in Africa due to strict foreign exchange controls, currency volatility, and liquidity constraints. The costs typically range from 75 to 100 basis points, but the real challenge is the capital inefficiency that limits scalability across African markets.

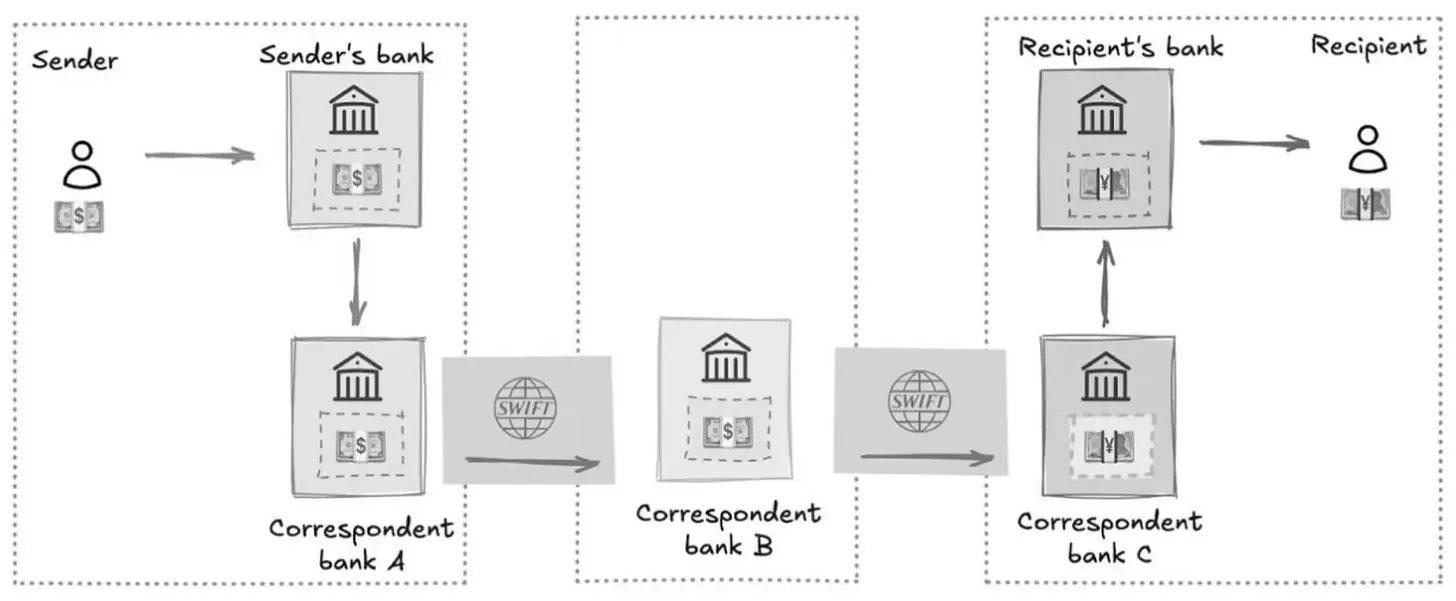

The second method involves SWIFT-based payments, which handle larger institutional transfers through a complex web of correspondent banks. A payment from the United States to Nigeria might pass through multiple intermediaries—local banks, foreign exchange dealers, and intermediary institutions—before reaching its destination. Each step adds delays, fees, and potential failure points. The entire process can take several days and cost between 150 to 300 basis points. For many African banks that lack direct connections to global networks, these transactions often route through European or American financial centers, adding even more complexity and expense.

These traditional systems create a particularly acute problem in Africa because a significant portion of the population remains unbanked. According to World Bank data, only 49% of adults in Sub-Saharan Africa had a bank account as of 2021. This leaves hundreds of millions of people excluded from formal financial services entirely, unable to participate in the global economy or access basic financial tools like savings accounts, credit, or insurance

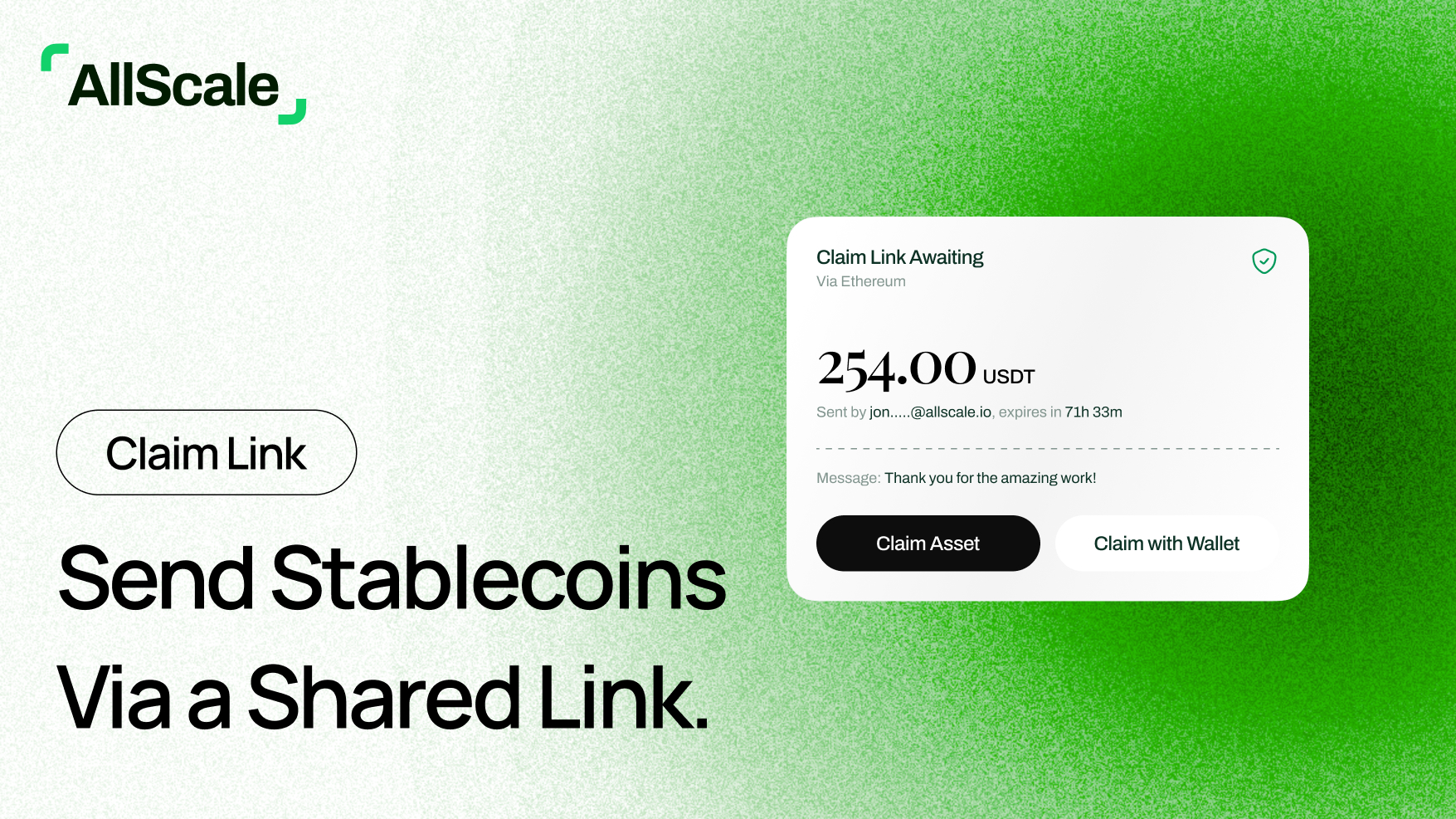

Stablecoins offer a fundamentally different approach. Instead of routing payments through multiple intermediaries, a user in New York can convert dollars into USDC and send them directly to a recipient in Lagos, who can then convert them to Nigerian naira through local exchanges or mobile money platforms. This process settles in real-time with fees as low as 10 to 50 basis points—a dramatic improvement over traditional methods.

The practical applications of stablecoins in Africa extend far beyond simple cost savings. They're addressing fundamental economic challenges that have persisted for decades.

Currency devaluation represents one of the most pressing financial challenges across African markets. The Kenyan shilling has lost 50% of its value against the US dollar since 2008, despite Kenya's GDP tripling over the same period. This stark contradiction—economic growth coupled with currency weakness—illustrates the disconnect between real economic progress and monetary stability.

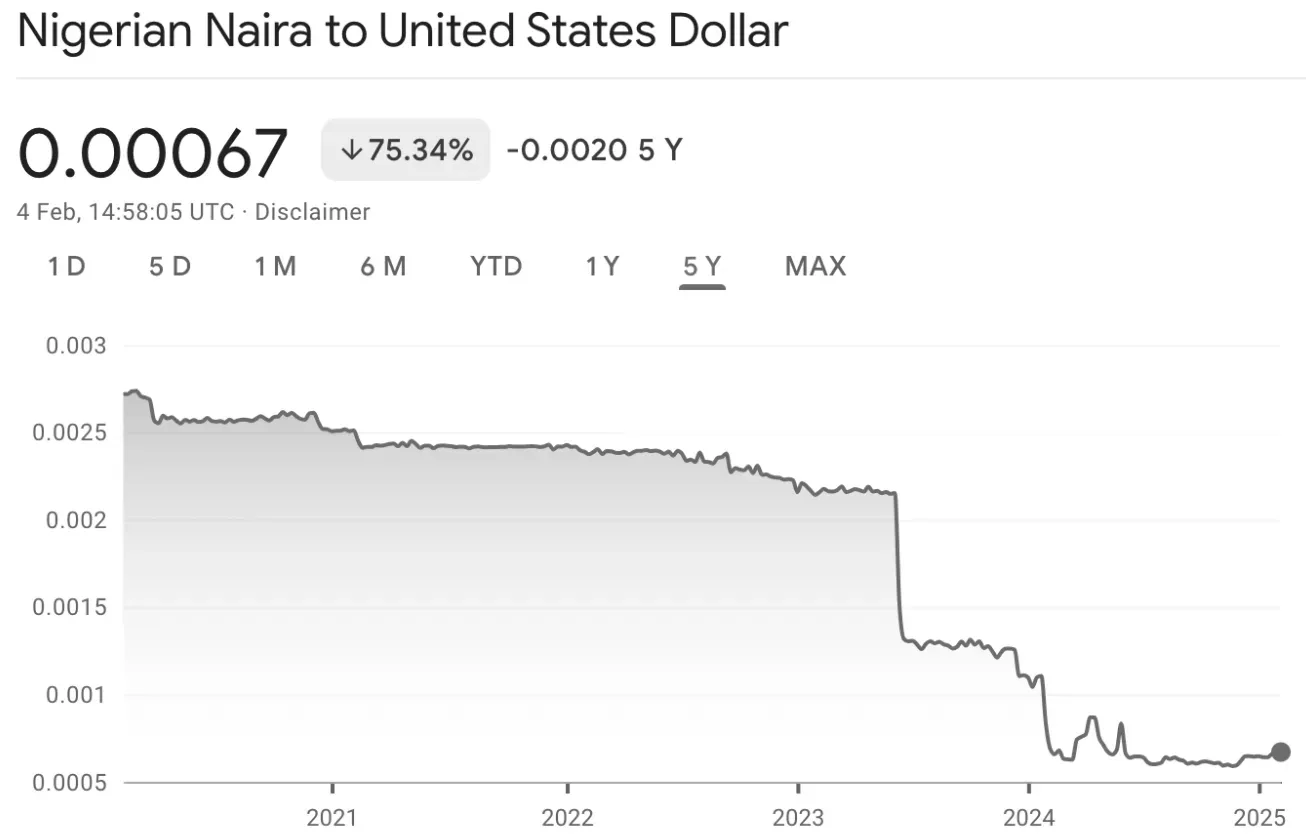

Nigeria presents an even more dramatic example. The naira hit record lows in February 2024, and inflation has reached levels not seen in decades. For ordinary Nigerians trying to preserve their wealth or conduct business, these conditions create impossible choices. Traditional hedges like US dollar bank accounts are often inaccessible or require minimum balances far beyond most people's reach. Physical dollars, where available, carry security risks and liquidity constraints.

Stablecoins provide a digital alternative that's accessible to anyone with a smartphone. A small business owner in Lagos can convert naira earnings into USDT during stable periods and convert back when needed for local transactions. This isn't speculation—it's basic financial risk management that was previously available only to the wealthy or well-connected.

The impact becomes even more significant when we consider the yield opportunities available through stablecoin platforms. While traditional Nigerian banks might offer interest rates of 2-3% annually, stablecoin savings platforms like Busha Earn provide yields up to 7.5%. For users already benefiting from currency stability, these higher returns create a powerful incentive for adoption.

Perhaps nowhere is the stablecoin advantage more apparent than in remittances. Africans working abroad sent approximately $100 billion home in 2023, with average fees around 8% according to World Bank data. For a typical $200 transfer from the United States to Nigeria, traditional services charge about $7.60. The same transfer using stablecoins costs less than $0.01.

This dramatic cost reduction has immediate, tangible benefits for families across the continent. A construction worker in Dubai sending $500 monthly to support family in Ghana saves over $400 annually by using stablecoins instead of traditional remittance services. For families operating on tight budgets, this represents a significant improvement in their financial situation.

But the benefits extend beyond individual savings. Businesses conducting cross-border trade are discovering that stablecoin settlements can dramatically improve their cash flow. A company importing goods from China can settle payments in minutes rather than days, reducing the working capital requirements that often constrain growth in emerging markets.

Africa faces a $330 billion credit gap, with millions of individuals and small businesses unable to access formal financing. Traditional banks avoid serving micro and small enterprises due to high operational costs, perceived risks, and regulatory constraints. The result is that promising businesses often turn to informal lenders charging interest rates that can exceed 100% annually.

Innovative stablecoin-based lending platforms are beginning to address this challenge through new models that leverage blockchain technology to reduce costs and improve risk assessment. Companies like Jia have achieved impressive results, with loan originations growing from $2 million to over $10 million in just one year while maintaining a default rate of only 0.14% and delivering 24% internal rates of return to investors

These platforms succeed by combining local market knowledge with global capital access. A small retail business in Nairobi might receive a $500 working capital loan funded by investors in London or New York, with the entire process managed through smart contracts that ensure transparency and efficiency for all parties.

Different African countries are embracing stablecoins through distinct pathways that reflect their unique economic conditions and regulatory approaches. Understanding these differences provides valuable insights into how the technology is evolving across the continent.

Nigeria has emerged as the epicenter of African cryptocurrency activity, ranking second globally in Chainalysis's latest adoption index. What makes Nigeria particularly interesting is that stablecoin adoption is primarily driven by retail users rather than institutions or speculators. Stablecoins comprise the largest portion of Nigerian crypto portfolios and are predominantly used for practical purposes rather than trading.

This grassroots adoption reflects real economic necessity. Nigeria suffers from one of Africa's highest inflation rates, reaching levels not seen in nearly three decades. The naira's persistent weakness, combined with limited access to foreign currency, has made stablecoins an essential tool for wealth preservation and international transaction

The regulatory environment has also evolved significantly. In December 2023, Nigeria lifted the central bank's ban on banks serving cryptocurrency companies, opening new possibilities for partnerships and smoother operations. Building on this progress, the Securities and Exchange Commission introduced the Accelerated Regulation Incubation Program in June 2024, requiring virtual asset service providers to register and undergo assessment before receiving full approval.

Perhaps most significantly, the Central Bank of Nigeria approved cNGN, the country's first regulated stablecoin, granting it a provisional license in 2024. This represents a major shift toward local currency-backed stablecoins that could help build trust and drive broader adoption of both stablecoins and the naira itself.

South Africa has positioned itself as the continent's most advanced cryptocurrency market from an institutional perspective, receiving $26 billion in transaction volume over the past year. Unlike other African markets where adoption is primarily retail-driven, South Africa is seeing significant institutional participation, with licensed firms and traditional financial institutions actively entering the space.

The country's success stems largely from regulatory clarity. South Africa has classified cryptocurrencies as financial products, creating a structured legal environment that provides certainty for businesses and investors. In March 2024, financial regulators approved 59 cryptocurrency operating licenses, paving the way for broader institutional adoption.

Local stablecoins are already gaining traction, with ZARP and ZARC providing rand-pegged alternatives for domestic transactions. As these integrate with existing payment networks, they're creating bridges between traditional finance and digital assets, making it easier for South Africans to incorporate stablecoins into their daily financial activities.

The government's 2024 budget review emphasized structural reforms and new policies focused on stablecoins and blockchain-based digital payments. This top-down support, cmbined with growing institutional interest, positions South Africa as a potential hub for regulated, bank-backed stablecoins that could drive mainstream adoption across the continent.

Kenya has long been Africa's fintech pioneer, from launching M-Pesa to embracing blockchain early in its development. Now, the country is positioning itself as a key stablecoin hub in East Africa by leveraging its mature mobile money infrastructure and progressive regulatory environment.

M-Pesa processes around 60% of Kenya's GDP and reaches over 90% of the adult population, creating the perfect foundation for stablecoin adoption. Users already comfortable with digital money transfers can easily transition to stablecoins for international transactions or value storage. The technological and behavioral infrastructure already exists—stablecoins simply extend these capabilities globally.

Kenya's regulatory approach through the Capital Markets Authority's sandbox program has fostered innovation while maintaining appropriate oversight. This environment has enabled blockchain companies to test and refine their products, contributing to Kenya's emergence as the global leader in tokenized real-world asset lending, with $73.8 million in loans—outpacing much larger economies like India and Brazil.

Small and medium enterprises in Kenya face significant credit constraints, with businesses seeking approximately $1.1 billion in loans in 2021 alone. Stablecoin-powered lending solutions are beginning to fill this gap by providing cheaper, faster, and more accessible credit options that leverage global liquidity pools.

For companies like Allscale looking to establish themselves in Africa's financial technology sector, the stablecoin revolution presents unprecedented opportunities. The key is understanding that this isn't just about cryptocurrency—it's about building the financial infrastructure that will power Africa's economic growth for the next decade.

The most immediate opportunity lies in building the infrastructure that enables stablecoin adoption. This includes on-ramp and off-ramp services that allow users to convert between local currencies and stablecoins, API platforms that enable businesses to integrate stablecoin payments, and compliance solutions that help companies navigate evolving regulatory requirements.

Stripe's $1.1 billion acquisition of Bridge, just two years after its launch, demonstrates the massive value creation potential in stablecoin infrastructure. Bridge serves most African payment companies, facilitating stablecoin payouts across Europe, the United States, and Asia. This acquisition validates the infrastructure thesis and highlights how quickly the right solutions can scale.

Companies entering this space need to focus on solving practical problems rather than building technology for its own sake. Yellow Card, Africa's largest licensed stablecoin on/off-ramp, doubled its annual transaction volume to $3 billion in 2024 by focusing relentlessly on user experience and regulatory compliance. Their success demonstrates that the market rewards companies that make stablecoins accessible to ordinary users rather than crypto enthusiasts.

The cross-border payments opportunity extends far beyond individual remittances. African businesses conducting international trade face significant challenges with traditional payment rails—high fees, long settlement times, and complex compliance requirements that can tie up working capital for days or weeks.

Conduit, which enables stablecoin payments for import-export businesses across Africa and Latin America, saw its annualized transaction volume surge to $10 billion in 2024, up from $5 billion in 2023. This growth reflects real demand from businesses seeking more efficient payment solutions.

The opportunity is particularly significant for intra-African trade, which currently accounts for only 15% of the continent's total trade—far below other regions like North America (54%) or the European Union (70%). Much of this inefficiency stems from the lack of direct currency conversion infrastructure, forcing trades to route through dollars or euros. Stablecoin rails could eliminate these inefficiencies, potentially saving $5 billion annually in unnecessary conversion costs.

Traditional financial institutions across Africa are beginning to recognize stablecoins as complementary to rather than competitive with their services. Banks in South Africa are exploring bank-issued stablecoins, while regulatory frameworks are evolving to accommodate hybrid models that combine traditional banking with blockchain technology.

This creates opportunities for companies that can bridge traditional finance and stablecoin infrastructure. Rather than attempting to displace banks, successful companies will likely partner with them to extend their reach and capabilities. A regional bank might use stablecoin rails to offer instant cross-border transfers to customers, while a mobile money provider might integrate stablecoins to enable global transactions.

The lending opportunity is particularly compelling given Africa's $330 billion credit gap. Stablecoin-based lending platforms can access global capital markets while serving local borrowers, creating more efficient capital allocation. Companies like Jia have demonstrated that blockchain-based lending can achieve both social impact and attractive returns by reducing operational costs and improving risk management through transparent, automated systems.

Success in Africa's stablecoin market requires careful attention to regulatory developments across different jurisdictions. The regulatory environment is evolving rapidly, with most governments recognizing the need to balance innovation with consumer protection and financial stability.

Nigeria's approach through the Securities and Exchange Commission's Accelerated Regulation Incubation Program provides a model for other countries. By requiring registration and assessment before full approval, regulators can monitor developments while allowing innovation to continue. Companies entering the market should view regulatory compliance as a competitive advantage rather than a burden—early movers who establish compliant operations will have significant advantages as markets mature.

South Africa's classification of cryptocurrencies as financial products provides greater certainty but also higher compliance requirements. Companies operating in South Africa need robust anti-money laundering and customer identification systems, but benefit from clearer legal frameworks and greater institutional acceptance.

Kenya's regulatory sandbox approach allows for experimentation within defined parameters. Companies can test innovative solutions while working with regulators to understand implications and develop appropriate frameworks. This collaborative approach has contributed to Kenya's position as a leader in blockchain-based financial services.

Looking forward, the next decade will likely see stablecoins become deeply embedded in Africa's financial infrastructure. Current trends suggest that more Africans may soon hold crypto wallets and use stablecoins for daily transactions than traditional bank accounts. This isn't just speculation—it reflects the superior user experience that stablecoins provide for cross-border transactions, value storage, and digital commerce.

The infrastructure being built today will determine which companies capture the enormous value creation opportunity ahead. Early movers who solve real problems, maintain regulatory compliance, and focus on user experience will likely see outsized returns as adoption accelerates.

For companies like Allscale, the question isn't whether stablecoins will transform African finance—it's how quickly they can position themselves to benefit from this transformation. The opportunity is massive, the technology is proven, and the regulatory environment is becoming more supportive. Success will go to those who execute most effectively on the fundamentals: solving real problems for real users in ways that create lasting value.

The stablecoin revolution in Africa has moved beyond early adoption into mainstream implementation. Companies that understand this shift and position themselves accordingly will play a crucial role in building the financial infrastructure that powers Africa's continued economic growth. The time for observation has passed—the time for action is now.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.