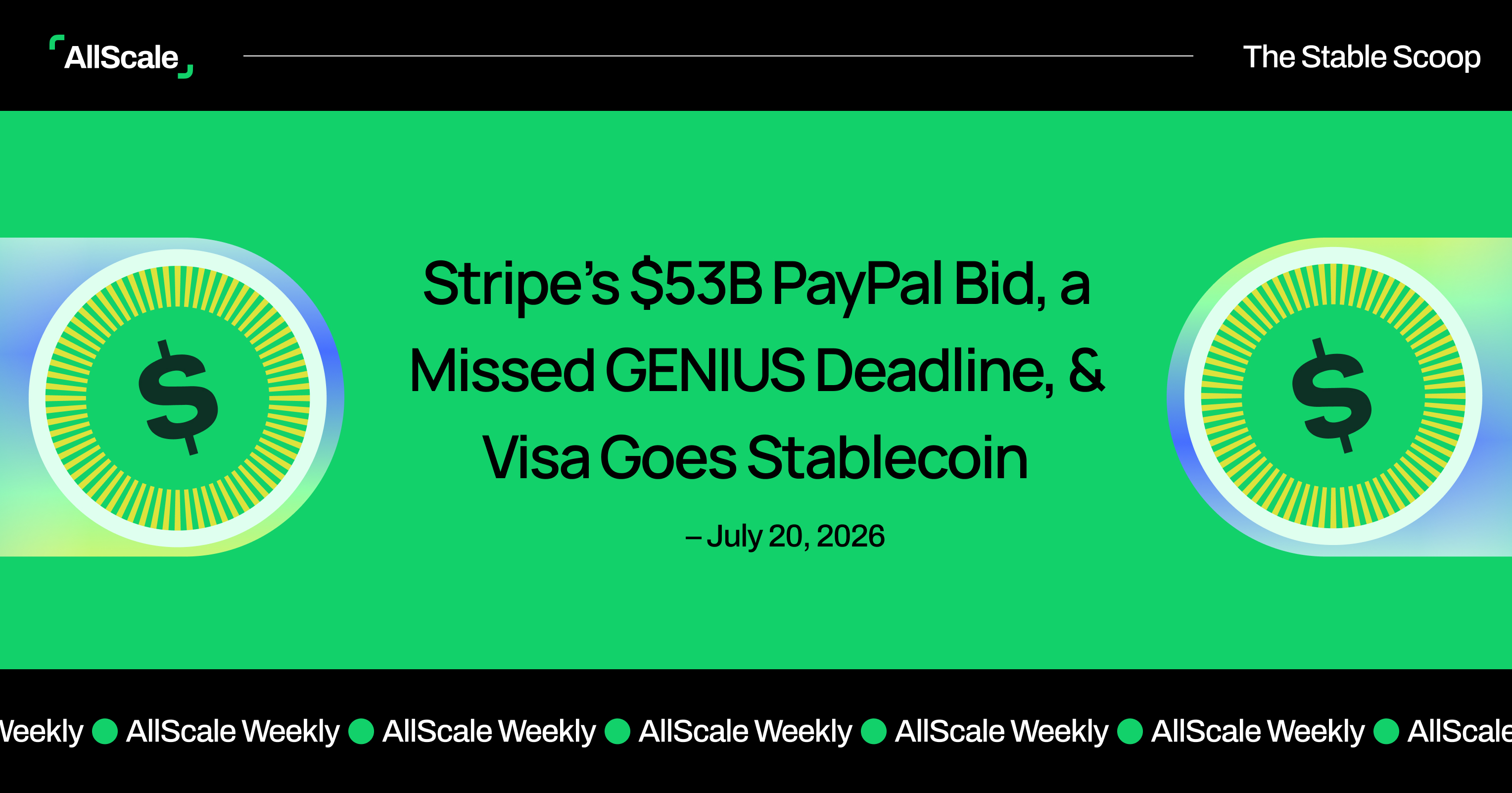

Hi everyone - we’re kicking off a new weekly research series at AllScale covering the biggest forces shaping stablecoins, payments, DeFi, and digital asset infrastructure. Stay tuned for more!

.jpg)

Editor - Jackie

The GENIUS Act is a pivotal legislation that came out in July of 2025 and arguably rewrote the U.S. stablecoin landscape. Let us take a deep dive into the full timeline, starting from when the storm first started brewing in March 2025, and examine how the Act shaped and continues to impact the dynamics between the U.S. government and both DeFi and TradFi players.

Jan-Feb, 2025: The seeds for stablecoin regulation are sowed...

On January 24th, U.S. President Donald Trump created a working group on maintaining responsible digital assets market growth by signing an executive order; the group was to be chaired by special AI and crypto advisors as well as major agencies such as the Treasury. On January 27th, Trump made the promise of making the U.S. The “crypto capital of the planet”.

When February rolled around, the White House echoed Trump’s pro-crypto stance and said it wanted to prioritize stablecoin legislation and make sure the U.S. dollar stayed #1 as the world’s reserve currency. Two proposals came out this month; the STABLE Act of 2025 and the GENIUS Act. Both proposals’ number one goal was to establish a clear regulatory framework for Payment Stablecoins (PS).

Looking back, Trump’s 180 degree switch-up was the most telling sign that stable coin regulation was just beyond the horizon.

On March 13th, The GENIUS Act passed the Senate Banking Committee in a bipartisan 18-6 vote, signifying another major step toward becoming law. So, what changed?

On May 19th, The United States Senate once again made historic progress by pulling off a 66-32 vote, successfully clearing a significant procedural hurdle. Notably, this vote included support from several Democrats who previously opposed it.

The GENIUS Act bill was on an unstoppable winning streak when June arrived. The Senate passed the bill with a 68-30 vote, meaning that the only hurdles ahead were in the Republican-held House.

On the DeFi side, Tether CEO Paolo Ardoino highlighted his excitement for the GENIUS Act as he claims Tether would be seeking a full audit and how it’s a top priority since “[they] are now living in a landscape where it’s actually feasible”. This positive sentiment was echoed by his peers. Companies such as Shopify and World Liberty Financial have all been making more moves, ranging from rolling out USDC-powered payments or launching their own stablecoin.

Team TradFi was clearly not as hyped for the GENIUS Act getting all this love. The American Bankers Association made a statement highlighting their concern for “an outflow of funds from bank deposits to the reserves backing these stablecoins”. They wanted a framework that offered more protection for community banks. On the flip side, some TradFi players were eager for change; banks like Standard Chartered and Bank of America signaled their willingness to launch their own stablecoins.

It seems like the only way to not get left behind in an industry that was becoming more and more stablecoin-leaning was to join in on the journey.

History was made on July 17th as lawmakers in the U.S. Officially passed the GENIUS Act, cementing it as the nation’s first major national cryptocurrency legislation.

Quickly following this pivotal moment, Securities and Exchange Commission (SEC) chair Paul S. Atkins unveiled Project Crypto, an initiative focused on examining existing securities rules related to digital assets. This initiative, although only loosely tied to the GENIUS Act, highlights the country’s strategic shift towards putting cryptocurrency at the center stage. The SEC also softened its stance on fully-backed USD-pegged stablecoin by allowing them to qualify as cash equivalents without being treated like securities.

Not everything was sunshine and rainbows though - there was still a tight rein on stablecoin issuers’ ability to pay interest, but firms such as Coinbase and PayPal were able to “sidestep” this rule by offering “rewards” instead.

Nonetheless, the three months following the officiation of the GENIUS Act was undoubtedly a honeymoon phase for DeFi.

A few notable moves that happened during this era for DeFi players can be well-represented by Tether appointing ex-White House Bo Hines to lead its U.S. Market entry push, Gemini eyeing a Wall Street debut, and crypto advocates rallying for more edits to the GENIUS Act.

As for the TradFi players, some were in deep waters while others decided to go with the flow. Trump cracked down on banks such as JPMorgan Chase that were unfairly targeting crypto firm founders. Over 50 U.S. Banking groups pointed out the loophole for stablecoin rewards and was rallying for more restrictions for stablecoin firms. Those who went with the GENIUS Act flow saw more success; big names like Mastercard and Visa were all quick to come out with strategic stablecoin initiatives. Specifically, Visa reported in July that it has processed over $200M stabecoin settlements and was already expanding its stablecoin settlement in Latin America.

The GENIUS Act tightened rules on stablecoin yield in October by classifying any return that “looks like interest” as such, yet the loophole remains for stablecoin firms. Senators mulled over stablecoin yield for this period. The Federal Deposit Insurance Corporation (FDIC) also started planning an application framework to support the GENIUS Act with further guidance. Apart from the act itself though, the government showcased its warm stance as U.S. Lawmakers pitched the PARITY Act, which suggests consumer-friendly tax relief such as exempting capital gain taxes on stablecoin transactions under $200 from federally regulated issuers. The FDIC also issued the first ever U.S. Stablecoin rule to assist institutions with stablecoin issuance.

DeFi players rushed to apply for U.S. Bank charters to scale operations. Players doing so include Bridge and Erebor Bank. Binance also made a major move by integrating Trump-linked USD1 into its core trading infrastructure. Stress was low for DeFi players, and this era was framed by deepening ties between them and the government.

More and more TradFi players turned team stables. Companies like BlackRock, Citi and JPMorgan all finalized plans of building GENIUS-compliant services or collaborating with stablecoin companies.

Drama aside, one thing is truer than true; stablecoin dominance is now an undeniable reality.

The Senate’s debate regarding the GENIUS Act over the past two months is now mainly centered on whether stablecoin interest or yield should be a thing. The waters are murky: there has been a lot of stalling and banking groups are pushing a blanket “no yield OR reward” stance. There’s still more than one silver lining though; the White House recently signaled its support for keeping limited stablecoin rewards that do not threaten deposits. Trump also spoke at Davos’s World Economic Forum and made it clear the U.S. was to remain the “crypto capital of the world”. The Office of the Comptroller of the Currency (OCC) is still making edits to core GENIUS rules.Stablecoins still remain the hottest center platter at the dinner table.

Both sides have been gearing up to fight for their interests. Coinbase CEO Brian Armstrong spoke out multiple times on the rewards debate, claiming that they were misunderstood and consumers should be able to earn more on their money. On the other hand, the U.S. bank lobby made “banning stablecoin yield” a top 2026 priority. Similarly, community banks warned this exact loophole could pull trillions of deposits, despite there being limited evidence of outflows.

Not all TradFi players were getting themselves tangled up in this fight. Mastercard joined forces with MetaMask to launch a fully-custodial mUSD payment card in the U.S.. Morgan Stanley has also hired veteran Amy Oldenburg to bolster its digital asset strategy department.

We have no idea what is to come in the next few months, but one thing is sure, with the help of the GENIUS Act, stablecoins have become a grounded reality in the U.S...and to survive in the fintech landscape in this time and age, it is best advised that you don’t miss this train.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.