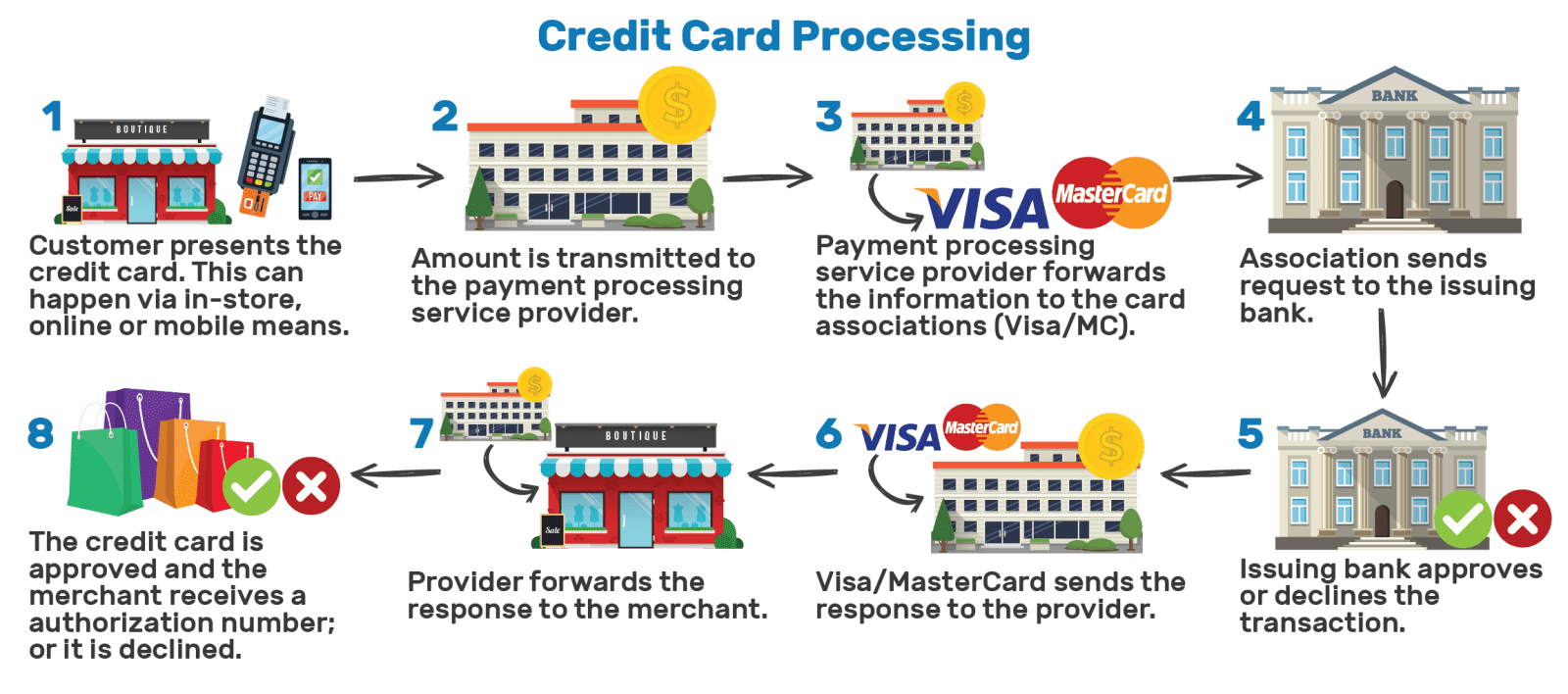

When customers swipe their credit cards at your business, the seemingly simple transaction triggers a complex fee structure that directly impacts your bottom line. Understanding these merchant fees isn't just about knowing where your money goes—it's about making informed decisions that can save your business thousands of dollars annually.

Credit card processing fees represent one of the largest operational expenses for most merchants. According to the latest industry data from 2024, the global overall average fee for processing credit card transactions is approximately 2.4% of the transaction value, with total merchant processing fees in the United States exceeding $187 billion in 2024, up 5.1% over 2023. Credit card processing fees typically range between 1.5% and 3.5% of the transaction amount, but this percentage tells only part of the story. Behind every credit card transaction lies a carefully orchestrated system involving multiple parties, each taking their share of the processing fees you pay.

Think of credit card processing like a relay race where your customer's payment passes through several hands before reaching your account. At each handoff, a fee is collected, and understanding who gets what—and why—is crucial for any business owner who wants to optimize their payment processing costs.

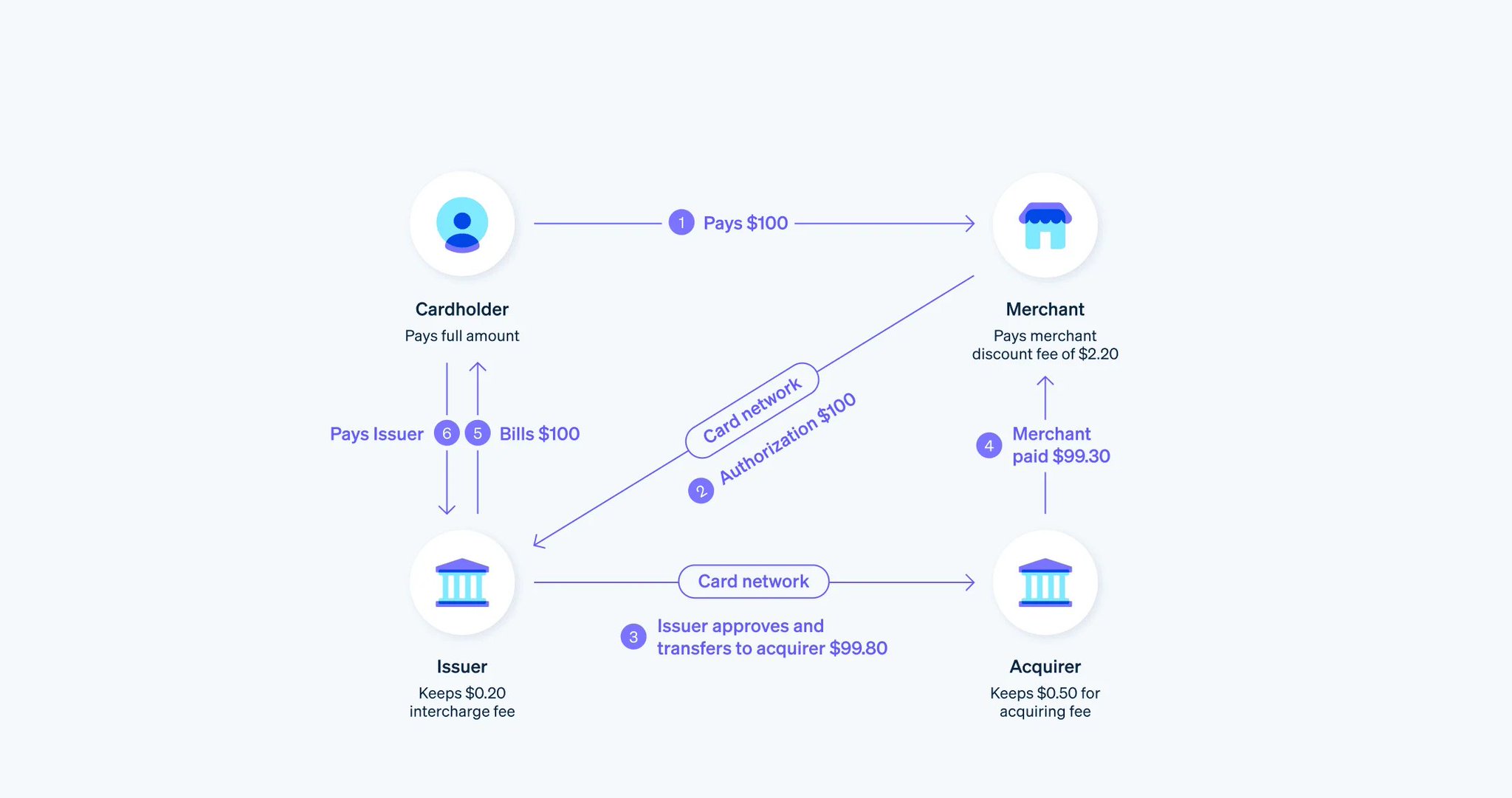

Every credit card transaction you process as a merchant generates fees that are split among three primary recipients, creating what we call the three-pillar structure of merchant fees. This framework helps us understand not just the "what" but the "why" behind each cost component.

Interchange fees represent the largest portion of your processing costs, typically accounting for 70% to 90% of your total merchant fees. These fees flow directly from your acquiring bank to the bank that issued your customer's credit card. Think of interchange as the "wholesale cost" of processing credit cards—it's the base price that all other fees build upon.

The logic behind interchange fees becomes clearer when you consider the risk and services provided by the issuing bank. When a customer uses their credit card at your business, the issuing bank is essentially providing you with an instant loan guarantee. They're promising to pay you for the transaction, even if the customer later defaults on their credit card bill. This risk transfer justifies the interchange fee structure.

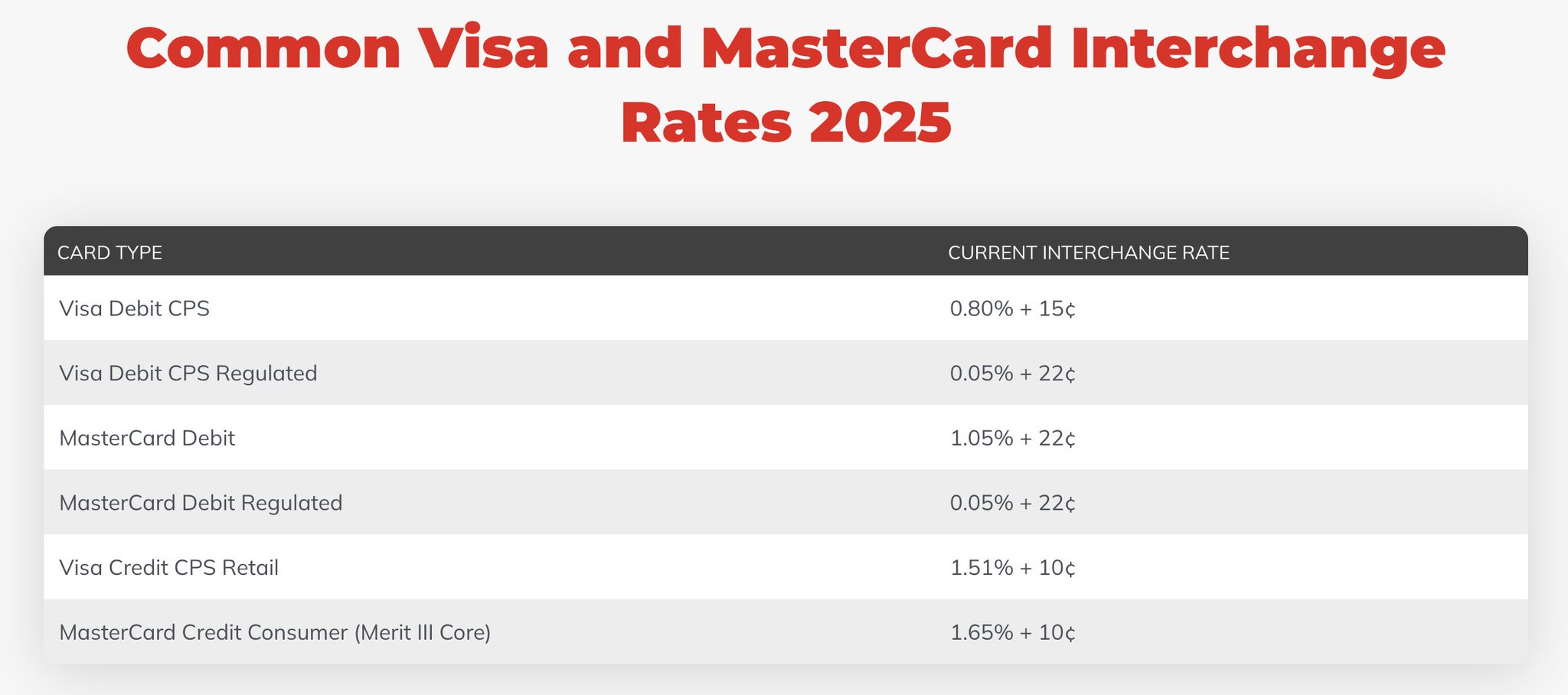

Interchange rates vary significantly based on several key factors. Reward cards typically carry higher interchange rates because the issuing bank needs additional revenue to fund cashback and points programs. Business cards often have even higher rates due to extended payment terms and higher credit limits. The method of transaction also matters—card-present transactions where the customer physically swipes or inserts their card generally have lower interchange rates than card-not-present transactions like online purchases, which carry higher fraud risk.

To put this in perspective, a typical retail Visa transaction might carry an interchange rate of 1.51% plus $0.10, while an online transaction with the same card might cost 2.30% plus $0.10. According to 2024 data, merchants paid $148.52 billion in processing fees to accept credit cards, representing a 9.3% increase from 2023. For a $100 transaction, the difference between card-present and card-not-present processing translates to $1.61 versus $2.40 in interchange fees—a substantial variance that accumulates quickly across thousands of transactions.

Assessment fees represent the second pillar of your processing costs, flowing directly to the card networks like Visa, Mastercard, American Express, and Discover. While smaller than interchange fees, typically ranging from 0.11% to 0.15% of transaction volume, assessment fees serve a critical function in maintaining the global payment infrastructure. According to recent industry analysis, American Express is the most expensive payment network while Mastercard has the lowest rates, especially for transactions of $1,000 and over, though the differences in assessment fees between each payment network are generally minuscule.

These fees fund the extensive technology infrastructure that makes credit card processing possible. The card networks operate sophisticated systems that route transaction authorizations around the globe in milliseconds, maintain fraud detection algorithms, and provide the brand recognition that gives consumers confidence to use their cards. When you think about the complexity of authorizing a transaction in real-time while checking for fraud patterns and ensuring sufficient credit limits, the assessment fee begins to seem quite reasonable.

Assessment fees also tend to be more standardized than interchange fees. Visa, for example, charges a consistent assessment fee regardless of the specific type of Visa card used, making this component more predictable for merchants. However, networks do adjust these fees periodically, and they may vary slightly based on transaction volume or merchant category.

Understanding assessment fees helps explain why some payment processors can offer competitive rates on one card brand but not another. The assessment fee structure differs between networks, so a processor's relationship and volume with specific networks can influence the rates they can offer merchants.

Payment Processor Markup: The Service Premium

The third pillar represents your payment processor's fee—their markup for facilitating the transaction and providing merchant services. This is typically the only fee component where merchants have direct negotiating power, making it crucial to understand how different processors structure their markup.

Payment processors offer various pricing models, each with distinct advantages and trade-offs. The flat-rate model, popularized by companies like Square, charges a consistent percentage regardless of the underlying interchange rate. For example, you might pay 2.9% plus $0.30 for every transaction, whether it's a basic debit card or a premium rewards credit card. This model offers predictability but often results in higher costs for merchants who process mostly lower-cost transactions.

The interchange-plus model provides more transparency by passing through the exact interchange and assessment fees, then adding a fixed markup. You might pay interchange plus 0.25% and $0.10 per transaction. This model typically offers lower costs for merchants who understand their transaction mix and can optimize their processing methods, but it creates more variable monthly statements.

Tiered pricing represents an older model where processors sort transactions into qualified, mid-qualified, and non-qualified categories, each with different rates. While this model can seem attractive with its low "qualified" rates, it often results in higher overall costs as processors have discretion in determining which transactions qualify for the lowest rates.

The key insight here is that processor markup is where your negotiating power lies. While you cannot influence interchange or assessment fees, you can shop around for competitive processor markups and choose pricing models that align with your transaction patterns.

While interchange, assessment, and processor markup form the foundation of your credit card processing costs, several additional fees can significantly impact your monthly processing expenses. Understanding these auxiliary costs helps you budget accurately and identify potential areas for optimization.

Monthly service fees represent ongoing costs for maintaining your merchant account, regardless of your transaction volume. These fees typically range from $10 to $50 monthly and cover account maintenance, customer service access, and basic reporting features. While these amounts might seem modest, they represent fixed costs that can be particularly burdensome for low-volume merchants.

Equipment and terminal fees cover the hardware needed to accept credit card payments. Traditional merchants might pay $20 to $50 monthly for terminal rentals, while businesses using integrated point-of-sale systems might face higher costs but gain additional functionality. The rise of mobile payment solutions has created more options, from simple card readers that plug into smartphones to sophisticated wireless terminals that can handle chip cards and contactless payments.

Gateway fees apply primarily to businesses that process card-not-present transactions, such as e-commerce merchants or businesses that take orders over the phone. Payment gateways provide the secure connection between your website or phone system and the processing network, typically charging $10 to $25 monthly plus a small per-transaction fee.

Chargeback fees present a significant concern for many merchants, particularly those in higher-risk industries. When a customer disputes a transaction, your processor typically charges $15 to $25 for handling the chargeback, regardless of whether you ultimately win or lose the dispute. More concerning is that excessive chargebacks can lead to higher processing rates or account termination.

PCI compliance fees cover the cost of maintaining security standards required for processing credit card transactions. Most processors charge $5 to $15 monthly for PCI compliance services, though merchants can sometimes reduce or eliminate these fees by completing annual compliance questionnaires and maintaining proper security protocols.

As merchants grapple with the complex and increasingly expensive traditional credit card fee structure, a transformative alternative is emerging that promises to fundamentally reshape the economics of digital payments. Stablecoins represent more than just another payment method—they offer a complete reimagining of how value transfer can work in the digital economy, with cost structures that challenge every assumption about payment processing fees.

The numbers paint a compelling picture of this disruption. According to a16z crypto's 2024 analysis, the global payments industry handled 3.4 trillion transactions worth $1.8 quadrillion in value, generating $2.4 trillion in revenue. The United States alone processed $5.6 trillion in credit card payments and $4.4 trillion in debit card payments. Yet stablecoin payments often incur fees of under 1%, and in some cases, especially on layer 2 blockchain solutions, the costs become negligible, enabling merchants to retain significantly higher revenue per sale compared to traditional payment methods.

The fundamental cost advantage of stablecoins becomes clear when we examine the architectural differences between traditional payment systems and blockchain-based alternatives. Traditional credit card processing requires multiple intermediary institutions, each extracting fees at different points in the transaction flow. A single credit card transaction involves the merchant's acquiring bank, the customer's issuing bank, the card network, and often additional processors and service providers. Each participant requires compensation for their role, creating the layered fee structure that results in the 2.4% global average processing cost.

Stablecoins eliminate many of these intermediaries through what economists call disintermediation. When a customer pays with stablecoins, the transaction occurs directly on a blockchain network, with smart contracts automatically handling the verification, settlement, and record-keeping functions that traditionally require human oversight and multiple institutional relationships. This technological architecture fundamentally reduces the number of parties involved in each transaction, creating immediate cost savings that can be passed through to merchants.

The implications extend beyond simple fee reduction. Traditional payment systems operate on what we might call "trust-through-institutions" model, where banks and card networks serve as trusted intermediaries who guarantee transaction completion and assume various risks. Stablecoins operate on a "trust-through-technology" model, where cryptographic protocols and transparent blockchain records provide the necessary security and verification without requiring institutional intermediaries. This shift doesn't just reduce costs—it eliminates entire categories of fees that exist solely to compensate institutions for risk assumption and manual processing.

The cost differential between traditional credit card processing and stablecoin payments becomes stark when we examine specific transaction scenarios. For a typical $1,000 business-to-business transaction processed through traditional credit cards, a merchant might pay $24 to $35 in total processing fees, depending on the card type and processing arrangement. The same transaction processed through stablecoins might incur network fees of $0.50 to $5, depending on the blockchain network and current congestion levels.

This cost advantage becomes even more pronounced for smaller transactions, where credit card processing fees create what economists call a "minimum viable transaction threshold." The combination of percentage-based interchange fees and fixed per-transaction costs makes credit card acceptance economically unfeasible for micropayments. A $5 transaction might generate $0.25 in processing fees, representing a 5% cost that many businesses cannot absorb. Stablecoin networks, with their primarily fixed-fee structures, make micropayments economically viable for the first time, potentially opening entirely new business models and revenue streams.

Cross-border transactions reveal perhaps the most dramatic cost differences. Traditional credit card networks typically add currency conversion fees, international assessment fees, and higher interchange rates for cross-border transactions, potentially increasing total processing costs to 4% or higher. Stablecoins, being global digital assets by design, process international transactions at the same cost as domestic ones, eliminating the premium typically associated with cross-border commerce.

Beyond direct fee savings, stablecoins offer a fundamental improvement in settlement timing that creates additional economic value for merchants. Traditional credit card transactions involve complex settlement processes that can take 1-3 business days, during which merchants bear the risk of chargebacks, network failures, and other complications. This settlement delay creates real costs in terms of cash flow management, working capital requirements, and risk exposure.

Stablecoin transactions achieve settlement finality within minutes or even seconds, depending on the underlying blockchain network. This immediate settlement eliminates the traditional concept of payment processing "float" and reduces working capital requirements. For businesses with tight cash flow cycles, this improvement in settlement timing can be worth more than the direct fee savings, as it reduces the need for expensive working capital financing and improves overall business liquidity.

The implications extend to chargeback risk as well. Traditional credit card transactions remain reversible for extended periods, with cardholders able to dispute transactions months after completion. This reversibility creates ongoing risk exposure and administrative costs for merchants. Stablecoin transactions, once confirmed on the blockchain, achieve true finality, eliminating chargeback risk entirely and reducing the need for complex dispute management systems.

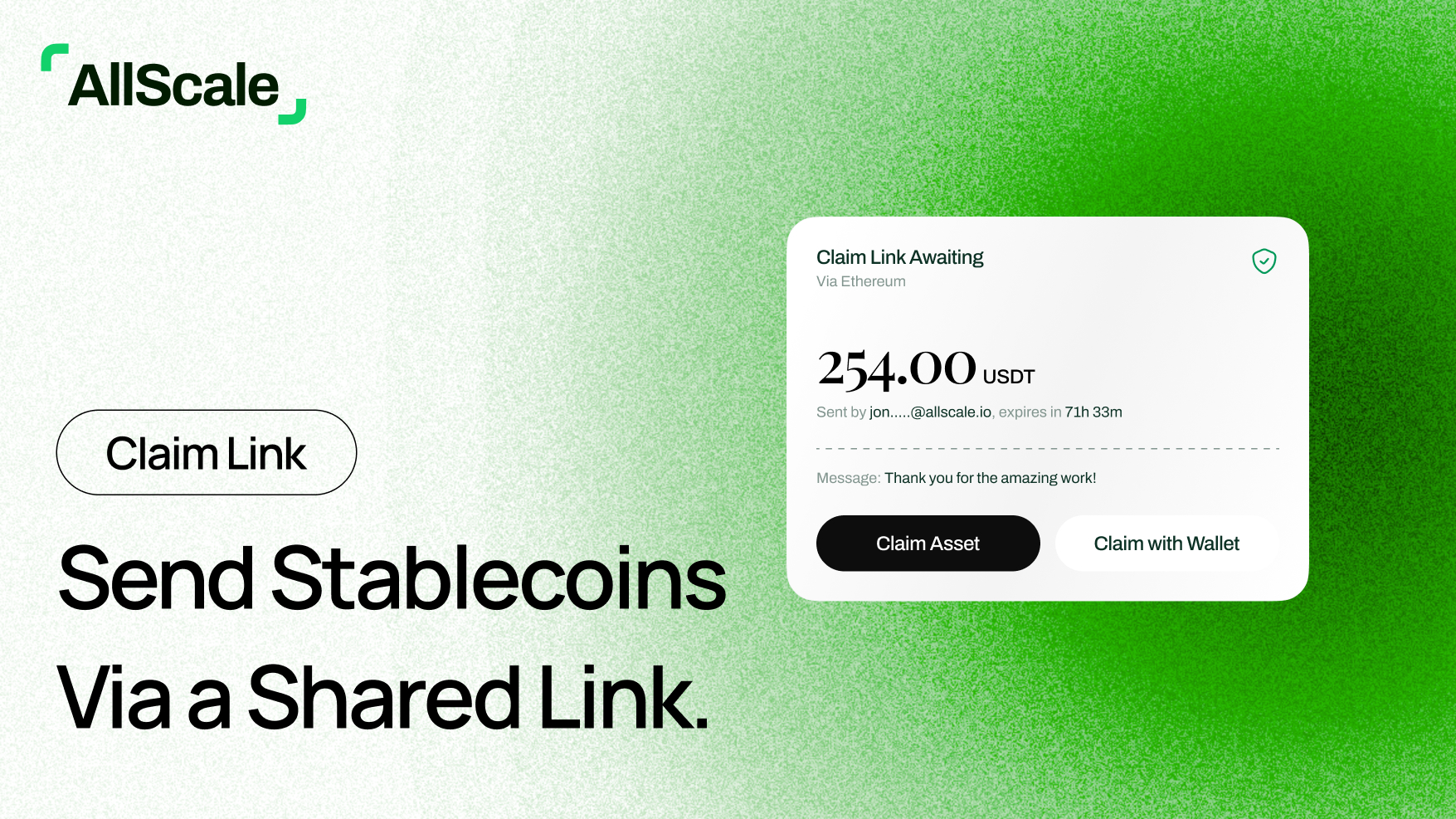

As the stablecoin payment ecosystem matures, comprehensive platforms are emerging that transform these technological capabilities into practical business solutions. AllScale represents a leading example of how stablecoin technology can be packaged into enterprise-ready systems that address real business needs while delivering the cost and efficiency advantages of blockchain-based payments.

AllScale's stablecoin operating system goes beyond simple payment processing to create an integrated financial infrastructure for modern businesses. Their invoicing platform demonstrates how stablecoin technology can streamline the entire accounts receivable process. Traditional invoice processing involves manual payment matching, bank reconciliation delays, and complex international payment handling. AllScale's system enables businesses to send invoices that customers can pay instantly with stablecoins, with automatic matching and immediate settlement confirmation. This eliminates the traditional accounts receivable cycle delays and reduces the administrative overhead associated with payment processing and reconciliation.

The payroll application showcases another transformative use case for stablecoin technology. Traditional international payroll processing involves expensive wire transfers, currency conversion fees, and multi-day settlement periods that create cash flow challenges for both employers and employees. AllScale's payroll system enables instant, low-cost international payments, allowing businesses to pay remote workers or international contractors without the traditional banking friction and fees. For companies with distributed workforces, this capability can reduce payroll processing costs by 60-80% while improving employee satisfaction through faster payment delivery.

Perhaps most innovatively, AllScale's social commerce platform demonstrates how stablecoin technology can enable entirely new business models. Traditional e-commerce platforms are constrained by credit card processing economics that make micropayments and dynamic pricing models economically unfeasible. AllScale's social commerce tools enable creators, influencers, and small businesses to monetize content and services through microtransactions, subscription models, and other innovative pricing approaches that become economically viable only with stablecoin cost structures.

The transition to stablecoin payments creates powerful network effects that compound the individual benefits for merchants. As more businesses accept stablecoin payments, the utility and adoption of stablecoins among consumers increases, creating a virtuous cycle that strengthens the entire ecosystem. This network effect phenomenon is already visible in industries and regions where stablecoin adoption has reached critical mass.

International trade provides a compelling example of these network effects in action. Traditional international trade involves complex correspondent banking relationships, letter of credit processes, and multi-day settlement periods that create friction and cost throughout the supply chain. As more international traders adopt stablecoin payment systems, the efficiency gains compound throughout entire trading networks, reducing costs and settlement times for all participants.

The programmability of stablecoin systems creates additional network effects through what we might call "composability"—the ability to combine different financial functions into integrated workflows. AllScale's platform exemplifies this composability by integrating invoicing, payroll, and commerce functions into unified systems that share data and automate complex business processes. As more businesses adopt these integrated systems, the value proposition increases for all participants through improved interoperability and reduced integration costs.

Understanding credit card merchant fees requires viewing them not as unavoidable costs but as investments in your business's ability to serve customers and generate revenue. The three-pillar structure of interchange fees, assessment fees, and processor markup provides a framework for analyzing and optimizing these costs. With merchants paying a record $187.2 billion in processing fees in 2024, representing a 5.1% increase over 2023, the economic imperative for payment processing optimization has never been more urgent.

The data reveals the scale of this challenge. The global average processing fee of 2.4% means that for every $100 in sales, merchants surrender nearly $2.50 to payment processing costs before considering any other operational expenses. When multiplied across the $5.6 trillion in annual U.S. credit card volume, these seemingly small percentages represent enormous economic transfers from merchants to financial intermediaries.

Yet the emergence of stablecoin payment systems offers a fundamentally different value proposition. With processing costs often under 1% and settlement measured in seconds rather than days, stablecoins represent more than incremental improvement—they offer order-of-magnitude changes in payment economics. The contrast becomes particularly stark in cross-border commerce, where traditional credit card premiums can push processing costs above 4%, while stablecoins maintain consistent global pricing.

The most successful merchants approach this transition with the same analytical rigor they apply to other strategic business decisions. They understand their transaction patterns, regularly review their processing costs, and evaluate emerging alternatives based on total economic impact rather than simple fee comparisons. The goal is not necessarily to eliminate processing costs entirely, but to ensure optimal value for payment processing investments while positioning for the technological shifts reshaping the industry.

Platforms like AllScale demonstrate how stablecoin technology translates into practical business solutions. Their integrated approach to invoicing, payroll, and social commerce shows how businesses can capture both direct cost savings and operational efficiency gains. More importantly, these platforms reveal how stablecoin adoption enables entirely new business models that become economically viable only with dramatically lower payment processing costs.

The payment processing landscape is experiencing a fundamental transition comparable to the shift from cash to credit cards several decades ago. Businesses that understand these dynamics and position themselves strategically will transform what many view as a necessary cost center into a competitive advantage. The question for forward-thinking merchants is not whether this transformation will occur, but how quickly they can adapt to capture its benefits while the advantages of early adoption remain most pronounced.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.