In the internet age, WeChat Pay leverages its massive user base to build an ecosystem around WeChat Pay, expanding into numerous “small-amount,” “high-frequency” long-tail payment scenarios. Understanding users and their needs is a hallmark of WeChat.

WeChat Pay launched in January 2013, with founder Zhang Xiaolong envisioning deep integration into users' daily workflows, positioning the platform as "digital infrastructure" rather than a standalone financial product. This "invisible commercialization" philosophy consistently guided WeChat Pay's development, creating its distinctive path to market dominance.

During 2013's initial phase, WeChat Pay supported basic functionality including merchant account payments and QR code scanning. In October, the platform partnered with China People's Insurance to introduce comprehensive fraud protection services. Despite launching a decade after Alipay—which debuted in 2003 as an escrow service addressing e-commerce trust issues, introduced mobile payments in 2008, pioneered QR code technology in 2010, and partnered with Tianhong Asset Management to launch Yu'e Bao money market funds in 2013—WeChat Pay successfully captured significant market share during its catch-up period.

By end-2013, WeChat had achieved 270 million monthly active users (MAU), but these users primarily engaged with messaging functionality without inherent payment intent. WeChat Pay faced the classic "user acquisition without use case adoption" challenge. The fundamental issue involved bridging the cognitive gap between social interaction contexts and payment scenarios—users required psychological motivation to utilize social platforms for financial transactions.

WeChat's digital red envelope feature served as this critical bridge, representing an unintended yet transformational product innovation. The feature ingeniously combined social relationships, cultural traditions, and payment functionality into a single experience. Digital red envelopes transcend simple peer-to-peer transfers, functioning as emotional and social relationship carriers. When users send digital gifts, they prioritize "expressing goodwill" over "transferring money," creating psychological comfort with payment actions. The competitive "grabbing" mechanism generated viral social sharing effects, enabling rapid WeChat Pay adoption and scalable user acquisition.

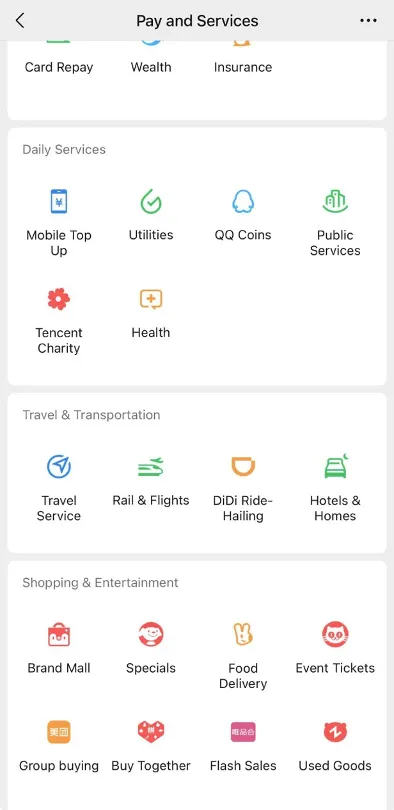

However, digital red envelopes alone proved insufficient for sustained payment engagement, as users typically withdrew funds after Chinese New Year celebrations. WeChat Pay's true breakthrough came through comprehensive long-tail payment scenario penetration, featuring optimal characteristics: "high-frequency," "micro-amounts," and "essential utility." Key examples included social commerce, ride-hailing through DiDi, food delivery via Meituan, and lifestyle services through the services grid interface.

The DiDi integration exemplifies strategic UX optimization rather than simple payment processing. Instead of encouraging app downloads or promotional incentives for payment adoption, the integration redefined transportation user experience. Users could request rides and complete payments directly within WeChat's services interface, creating seamless "one-stop" experiences that built WeChat Pay dependency and significantly improved conversion rates from WeChat users to WeChat Pay adopters. Similarly, the services grid interface enabled natural transitions from messaging windows to lifestyle services, mini-programs, and social commerce—comprehensive long-tail scenarios featuring "micro-payments," "high-frequency," and "essential utility" characteristics that dramatically enhanced user retention.

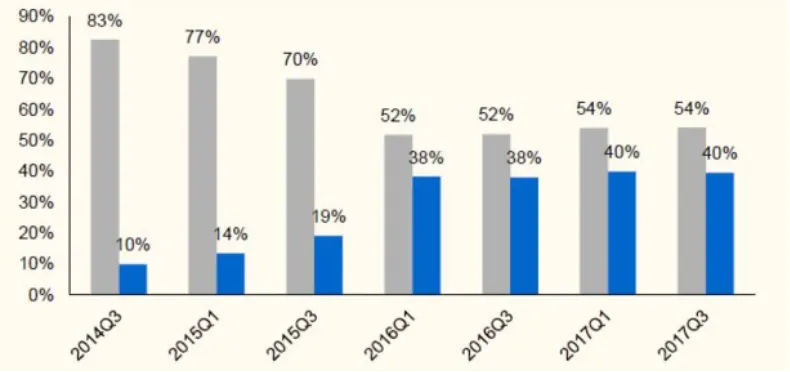

From a competitive strategy perspective, WeChat Pay adopted subtle market penetration rather than Alipay's aggressive "high-visibility" approach, which focused on converting high-margin financial services and "high-value," "low-frequency" financial scenarios. Market data supports this differentiation: as of Q4 2024, both Alipay and WeChat Pay exceeded 800 million MAU. However, Alipay users averaged 2,860 yuan monthly payment volume—2.3x WeChat Pay users' 1,240 yuan average—while WeChat Pay demonstrated superior daily usage frequency.

In data asset management and user profiling, WeChat Pay's advantage stems from social relationship data access rather than technological superiority. This data enables precise user behavioral pattern analysis, social network mapping, and consumption preference insights, facilitating highly personalized service delivery. While Alipay possesses comprehensive consumption data, it lacks social dimension intelligence, limiting user insight depth and personalization capabilities.

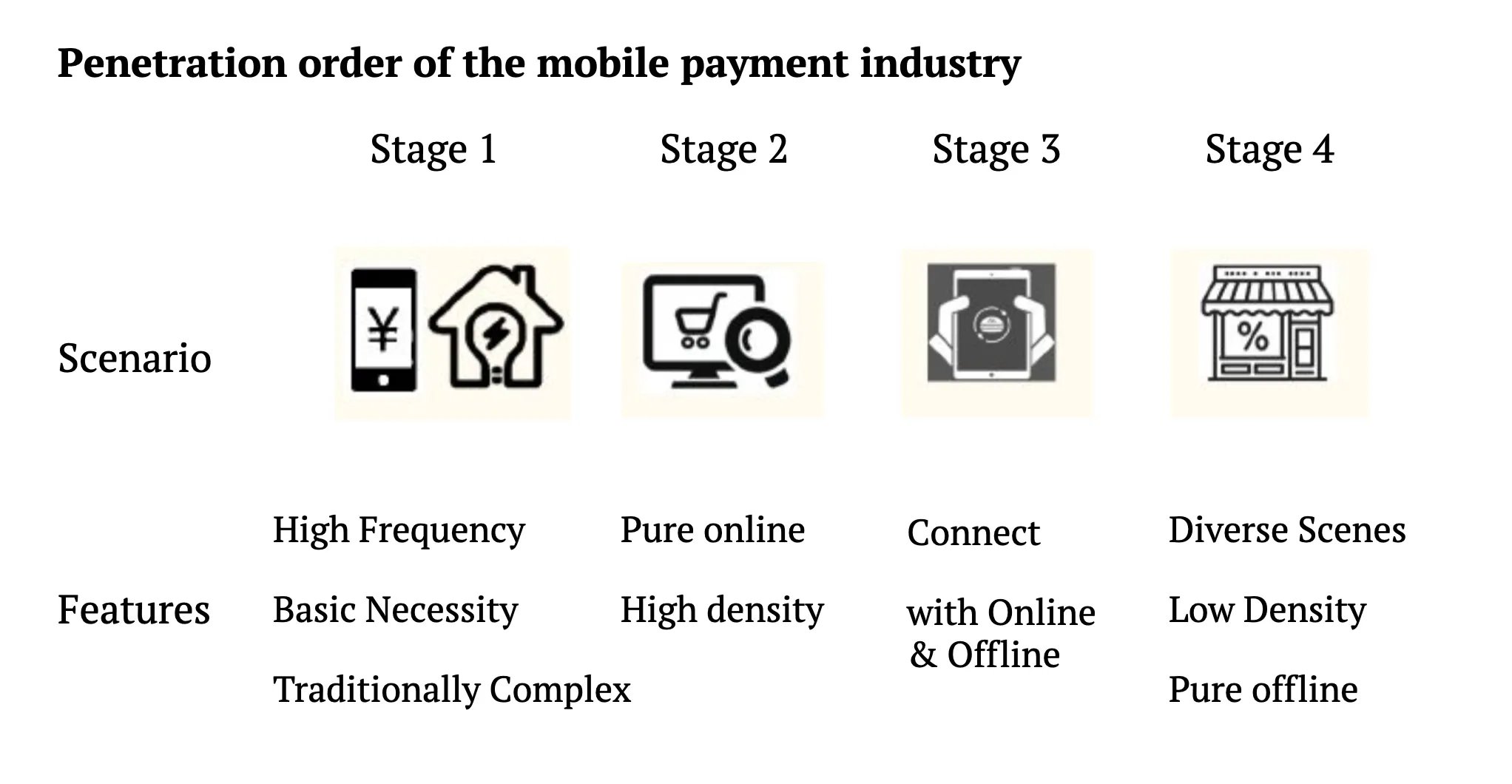

WeChat Pay's growth coincided with O2O (Online-to-Offline) industry expansion, marking digital payment migration from purely online to offline scenarios. Early adopters primarily involved essential daily services where traditional payment methods created friction, including mobile top-ups and utility bill payments. E-commerce represented the next adoption wave due to purely digital transaction flows and relatively low implementation barriers. China's e-commerce sector, led by Taobao and Alipay, pioneered digital payment adoption.

O2O scenarios followed, where users research products online but consume offline, with payments concluding the digital journey. DiDi, Meituan, and Ele.me exemplify this category. Purely offline scenarios presented the highest adoption barriers, as entire activities occur offline, making payment digitization challenging and requiring users to adapt to mobile payment workflows at physical points-of-sale. Additionally, unlike online merchants' "winner-take-all" concentration effects, offline merchants remain numerous and geographically dispersed, requiring extensive field marketing that proves time-intensive and labor-intensive. Consequently, offline penetration remains most challenging and slowest-developing.

From a technological evolution perspective, both platforms pursue ultimate "frictionless payment" experiences. Progression from passwords to biometric authentication (fingerprints, facial recognition) demonstrates that technology itself doesn't create barriers—success depends on seamless integration into user scenarios.

Case studies including Starbucks' social gifting campaigns and McDonald's mini-program demonstrate that within WeChat's mini-program ecosystem, payment competition transcends individual features, becoming ecological competition involving "scenarios + data + services." Social gifting success derived not from gift card functionality but from seamless integration of social relationship networks, personalized customization, and offline consumption, creating novel purchase scenarios. McDonald's Mini Program value lies not in ordering and payment processing but in connecting user, merchant, and platform data to enable precision marketing and personalized service delivery.

WeChat Pay's success provides crucial payment industry insights. In the digital era, competitive advantages stem not from technology—which competitors can rapidly replicate and potentially exceed—but from deep user behavior and psychological understanding based on data assets, plus ecosystems built upon this understanding.

Telegram, founded by the Durov brothers (Nikolai and Pavel Durov) in 2013, evolved into one of the fastest-growing global messaging platforms, reaching approximately 900 million MAU by 2025. Telegram transformed from simple chat functionality into a multifunctional platform integrating social networking, large-scale group communication, and broadcast channels, with privacy, security, and open-source client software as core differentiators. By entering payments through The Open Network (TON) and related cryptocurrency initiatives, Telegram made significant progress toward super app status, aiming to seamlessly integrate messaging, social networking, and financial services.

Telegram's payment journey began with the TON blockchain project announced in 2018, designed to support in-app payments and broader transaction scenarios through its native cryptocurrency, Gram. However, regulatory pressure from the U.S. Securities and Exchange Commission (SEC) in 2019 forced Telegram to halt its initial coin offering (ICO), temporarily derailing TON development. Despite this setback, Telegram quickly pivoted, integrating third-party payment providers and introducing payment functionality in 2022 through Telegram Premium subscriptions and in-app purchases, establishing foundation infrastructure for broader payment ecosystems.

Currently, Telegram leverages TON (now community-driven The Open Network) to support peer-to-peer transfers, in-app purchases, and mini-app transactions, particularly excelling in Web3 and gaming verticals. Telegram Payments emerges as a potential competitor to WeChat Pay and Alipay, especially in markets prioritizing privacy and decentralization.

Telegram's payment ecosystem demonstrates several core competitive advantages. First, it maintains a truly global user distribution—1 billion users worldwide, unlike WeChat's China-concentrated user base. This provides inherent cross-border expansion potential, enabling scenarios like Southeast Asian street vendors or Eastern European freelancers conducting transactions within Telegram—global reach that many payment platforms can only aspire to achieve.

More significantly, Telegram's privacy-first architecture from inception provides unique payment sector advantages. Features including end-to-end encryption and disappearing messages attract users skeptical of traditional banking and centralized platforms. TON blockchain integration reinforces this positioning through low-cost, high-speed transaction processing, making micro-payments seamless—whether purchasing in-game items or tipping content creators with cryptocurrency, transactions complete instantaneously. These high-frequency, micro-payment scenarios mirror WeChat's growth through Red Packets and Didi integration, both deeply integrating payments into user scenarios while building "micro-payment," "high-frequency," and "essential utility" ecosystems that enhance TON payment stickiness.

Telegram's mini-apps represent another ecosystem catalyst, similar to WeChat's mini-programs, further solidifying payment infrastructure. These embedded applications within chat interfaces enable users to shop, game, and handle complex transactions without leaving Telegram. In 2024, Telegram-based blockchain gaming gained significant traction, with users spending small amounts on in-game assets and virtual item trading. This immersive experience made payments as natural as messaging. Additionally, Telegram's group and channel features provide ideal social commerce environments—from fan donations to community crowdfunding—seamlessly integrating payments into social interactions, closely aligning with WeChat's "invisible commercialization" strategy.

Telegram's decentralized architecture provides significant cross-border payment advantages. TON's blockchain technology eliminates traditional banking's cumbersome processes and high fees, addressing critical pain points for global SMEs and individual users. African entrepreneurs can directly receive European customer payments via Telegram, avoiding PayPal's high fees and extended settlement times.

Telegram's payment strategy demonstrates high flexibility and pragmatism. Rather than following WeChat's closed ecosystem cultivation or Alipay's aggressive subsidy spending, Telegram leverages decentralization trends to carve new global market positioning. Core logic involves attracting users through privacy and openness, reducing payment friction through mini-apps and blockchain technology, and integrating payment scenarios with social scenarios, making payments natural and seamless behaviors.

Users engage in group conversations and through social virality might discover entertaining mini-games, click to play, and casually purchase in-game items—the entire experience flows seamlessly. This "scenarios + services" integration mirrors WeChat's services grid approach, consolidating ride-hailing, food delivery, and bill payments into unified platforms.

TON's decentralized technology represents a competitive differentiator, offering low transaction costs and high speeds, making it particularly suitable for emerging Web3 and cross-border payment scenarios. Additionally, Telegram's open API and highly customizable bot capabilities distinguish it from WeChat's relatively closed and centralized approach, attracting developers to create tailored mini-apps spanning e-commerce to gaming scenarios.

However, Telegram's path faces significant obstacles. Regulatory concerns persist, with the 2019 TON controversy and Pavel Durov's 2024 arrest raising platform stability questions. Compared to WeChat, Telegram lacks robust e-commerce and O2O ecosystems comparable to Tencent's portfolio, making it challenging to replicate WeChat's user retention through strong O2O scenarios like Meituan and DiDi integration.

Regarding revenue models, while Telegram Premium and transaction fees generate income, they still lag behind WeChat's diversified revenue streams in scale and growth velocity.

The Web3 boom potentially provides TON project opportunities. Blockchain gaming success represents just the beginning, with more decentralized applications potentially emerging. Emerging markets present another growth opportunity. Financial inclusion demand in Southeast Asia and Africa remains strong, and Telegram's low-cost payment system could address these gaps. Collaborating with local e-commerce platforms or service providers to resolve ecosystem shortcomings could position Telegram as a global "WeChat Pay" equivalent.

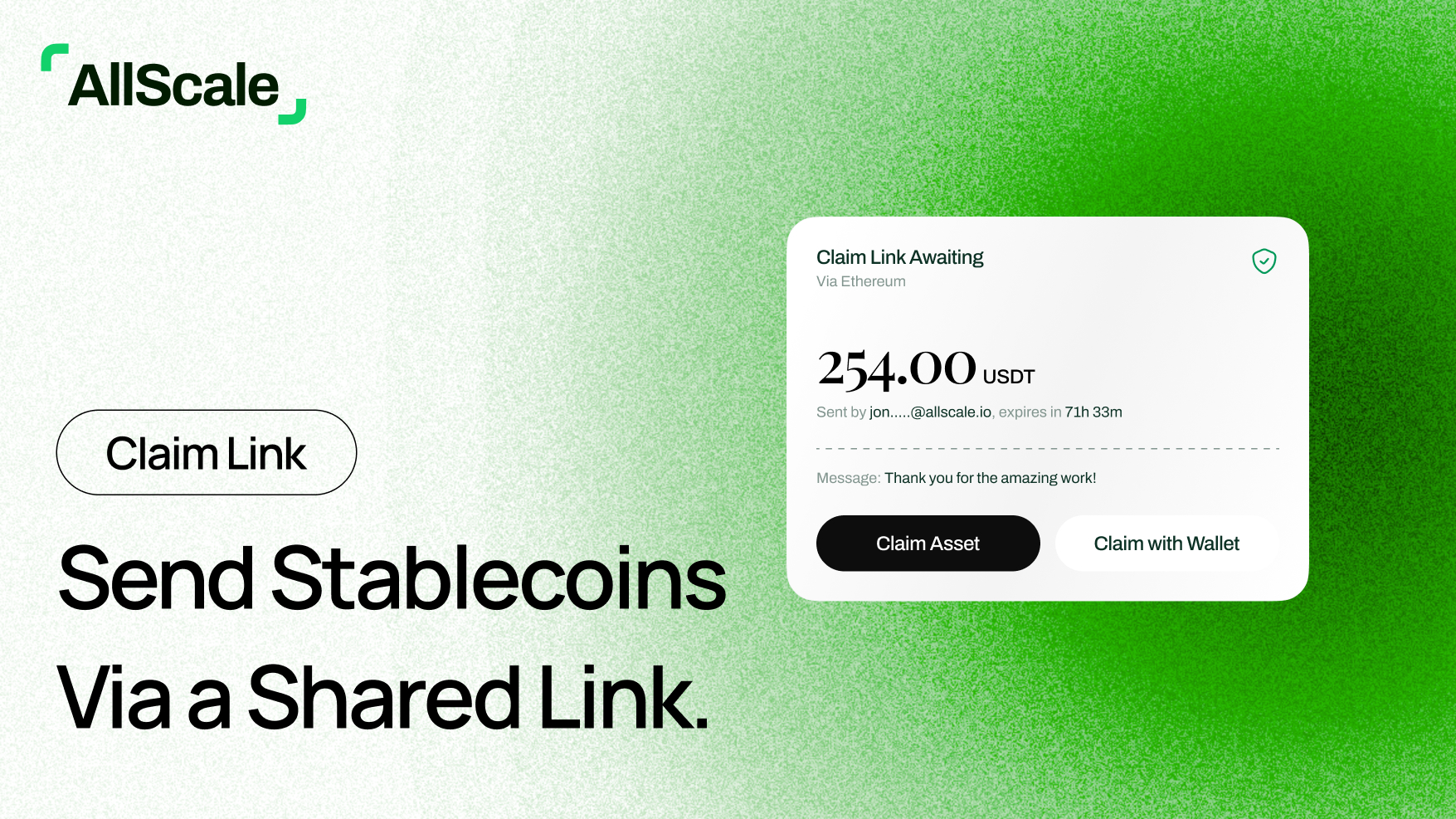

For startups like AllScale building invoicing, payroll, and social commerce solutions based on stablecoins, Telegram and WeChat's payment evolution provides strategic frameworks. AllScale's modular system shows promising development, featuring payroll management, invoice processing, and team collaboration capabilities. However, success depends on integrating these tools into users' core business workflows naturally, rather than presenting them as disconnected technical features.

AllScale's strategy aligns with Telegram's approach. AllScale functions similarly to WeChat Mini Programs on TON blockchain, serving as a powerful builder within Telegram's payment ecosystem. AllScale can collaborate with Telegram to leverage its ecosystem and user base. For example, integrating AllScale's stablecoin payment system into TON blockchain would enable users to process invoices or payroll directly within Telegram mini-apps.

Consider this scenario: a freelancer accepts work through a Telegram group, and the client issues an invoice and completes instant stablecoin payment through AllScale's mini-app, with the entire process completed within minutes. This seamless integration enables AllScale to rapidly access Telegram's 900 million user base.

In social commerce, AllScale's "social storefront" concept aligns deeply with Telegram's mini-app architecture. AllScale can develop Telegram-native store modules, allowing users to display products, manage orders, and receive payments directly within chat interfaces. Customers can purchase items through link clicks, eliminating PayPal redirect requirements.

Furthermore, AllScale's payroll module can be developed as mini-app versions, enabling SMEs to manage global team payroll directly within Telegram while automatically handling tax compliance and regulatory requirements.

Telegram and WeChat Pay success demonstrates that payment solution keys lie not in underlying technology but in making users perceive payments as natural daily life components. Just as Telegram makes payments engaging through tipping and gaming, AllScale can incorporate social or gamification elements into invoicing and payroll scenarios. Examples include sending employees "performance bonuses" during salary payments or automatically triggering team rewards upon invoice completion. This approach ensures users experience warm, interactive engagement rather than cold tool utilization.

Capturing "high-frequency" usage scenarios similar to WeChat and Telegram may prove essential. Telegram drives payments through micro-amount, high-frequency scenarios like gaming and tipping. AllScale can enter similar scenarios, enabling content creators to receive fan tips through biolinks or allowing small businesses to settle invoices quickly with stablecoins. The closer these scenarios align with users' daily activities, the higher the retention rates.

The decentralized approach offers valuable lessons. Telegram uses TON to reduce transaction costs, and AllScale's stablecoin naturally suits cross-border and low-cost payment scenarios. Success requires highlighting stablecoin immediacy and low-fee advantages, precisely targeting users frustrated with traditional finance, especially in scenarios where PayPal imposes high fees and slow settlements.

Data assets represent another value creation opportunity. Telegram leverages group and channel data for user behavior insights, and AllScale can utilize invoice and transaction data to help merchants predict inventory, analyze customer preferences, and potentially provide credit-based financing services. Just as WeChat uses social data to optimize services, AllScale can transform data into business decision catalysts.

Finally, AllScale can emulate Telegram's open ecosystem approach. Telegram's mini-apps continuously expand through developer community contributions. AllScale can open its API to encourage developers creating customized plugins for payroll and invoice modules, covering niche scenarios like gaming industry revenue sharing settlements or cross-border e-commerce rapid payments.

Finally, AllScale can emulate Telegram's open ecosystem approach. Telegram's mini-apps continuously expand through developer community contributions. AllScale can open its API to encourage developers creating customized plugins for payroll and invoice modules, covering niche scenarios like gaming industry revenue sharing settlements or cross-border e-commerce rapid payments.

Telegram's payment strategy acts as a flexible pioneer, leveraging privacy, decentralization, and globalization advantages to establish payment sector differentiation. If AllScale can capitalize on this momentum by integrating with TON and developing mini-apps, it can rapidly integrate into Telegram's ecosystem and reach global users.

By emulating Telegram and WeChat strategies, AllScale can make payments integral components of users' daily workflows, amplifying value through data insights and ecosystem expansion. AllScale has potential to evolve from tool-based platform into indispensable business operating system. The development path is extensive, but the strategic direction is clear.

[INVESTMENT DISCLAIMER]Investing involves risks. This information is not investment advice or a recommendation to buy, sell, or hold securities. Readers should assess their financial situation and risk tolerance before making investment decisions. We are not liable for decisions based on this information.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.