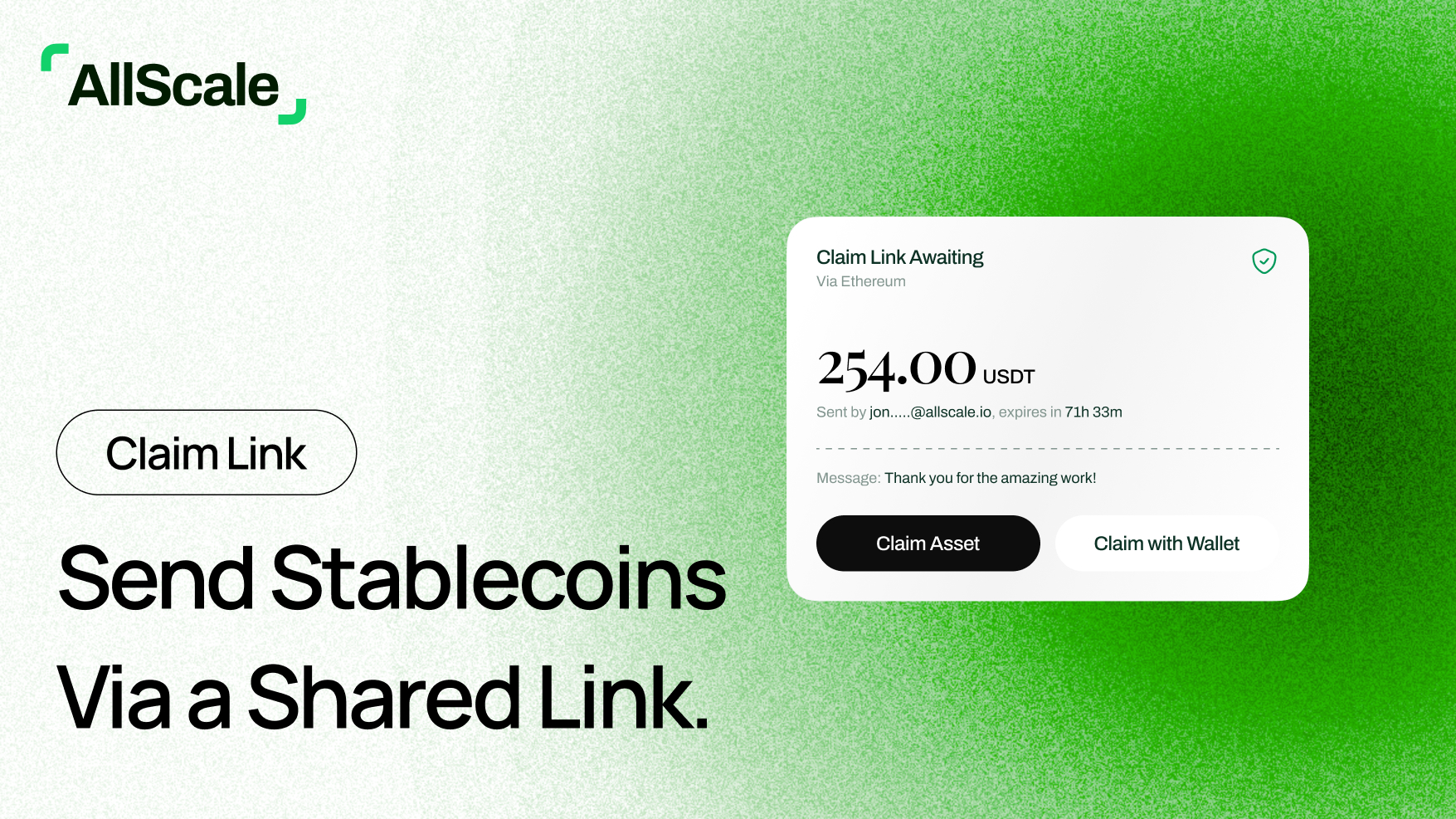

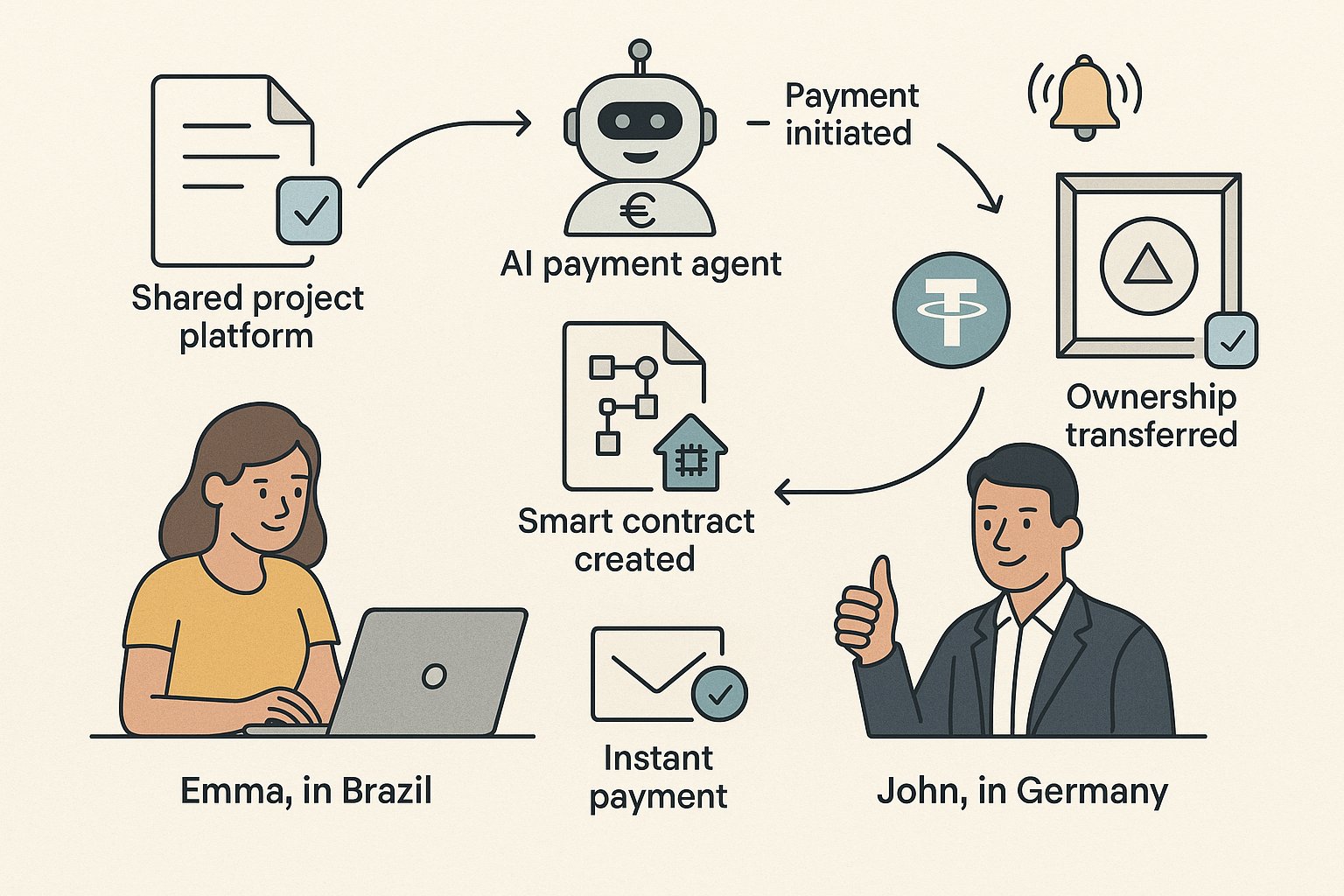

Imaging a scenario like this: Emma, a freelance graphic designer in Brazil, completes a logo design for John, a client in Germany, and uploads the final files to their shared project platform. John’s AI payment agent is notified of the delivery and, after confirming with John that the work meets his expectations, initiates the payment process. The agent checks the current exchange rate and calculates the equivalent amount in Emma’s preferred cryptocurrency, USDT. It then creates a smart contract on the blockchain, specifying that the payment will be released to Emma only after John’s explicit approval of the delivered files. Once John confirms his satisfaction, the smart contract automatically transfers the agreed amount of USDT from John’s crypto wallet to Emma’s wallet, and simultaneously records the transfer of ownership rights for the logo to John. Both parties receive instant notifications of the successful transaction, and their respective AI agents update their financial records for future reference. This seamless process, managed entirely by AI agents and blockchain technology, ensures that Emma is paid instantly and securely, while John receives full ownership of the work, all without the delays, fees, or uncertainties of traditional international payments.

We are entering an era where autonomous AI agents—software entities capable of making decisions, negotiating, and transacting—are poised to become the primary drivers of digital commerce. These autonomous digital agents, equipped to shop, negotiate, and handle transactions in real time, become smart intermediaries when combined with large language models (LLMs) that can interpret data. Their purpose is to streamline tasks such as securing the best deals, timing trades perfectly, and navigating international transactions—all without human involvement.

By linking these AI agents to modular payment APIs and stablecoin infrastructure, flexible orchestration layers enable instant data exchange and decision-making, much like assembling LEGO pieces. These composable APIs guarantee that every payment made by an AI agent is both trackable and reversible, striking the right balance between innovation and oversight that’s essential for agent-driven commerce to thrive.

As I’ve explored this rapidly evolving landscape, it’s become clear that the payment systems we’ve relied on for decades are fundamentally unfit for this new reality. The answer, I believe, lies in the adoption of crypto and on-chain payments. In this article, I’ll share why AI agents need crypto for payments, the unique technical challenges and opportunities this presents, and how this shift will reshape the very fabric of commerce.

At first, it might seem reasonable to equip AI agents with credit cards or bank accounts and let them transact as humans do. But the more I examine the technical underpinnings of our current payment infrastructure, the more I see how deeply it is built for human use, not for machines.

Credit card systems are designed around human input and oversight. The entire stack—from PCI compliance to fraud detection algorithms—assumes a person is entering card details, responding to two-factor authentication, and making judgment calls. There is no robust, standardized API for programmatic, agent-driven payments. Even if one could technically hand over card details to an agent, the risk of abuse, fraud, and regulatory non-compliance is enormous. Attempts to automate card usage—such as screen scraping or simulating user input—are unreliable, error-prone, and often break when the UI changes or new security measures are introduced.

The fee structure of traditional payment rails is another technical dead end. Transaction fees, which typically hover around 3% plus a fixed cost per transaction, are prohibitive for the kind of microtransactions that agents are likely to perform. Imagine an agent paying fractions of a cent for a snippet of data or a millisecond of compute time; the fee structure alone would render such transactions impossible. The very architecture of these systems is built for human-scale transactions—dollars, not fractions of a cent.

The global nature of the agent economy introduces further complications. Many developers and users of AI agents are located outside the traditional banking infrastructure, making it difficult or impossible to receive funds or participate in the global digital economy. The friction, exclusion, and inefficiency built into the current system are at odds with the borderless, permissionless ethos that defines both AI and crypto.

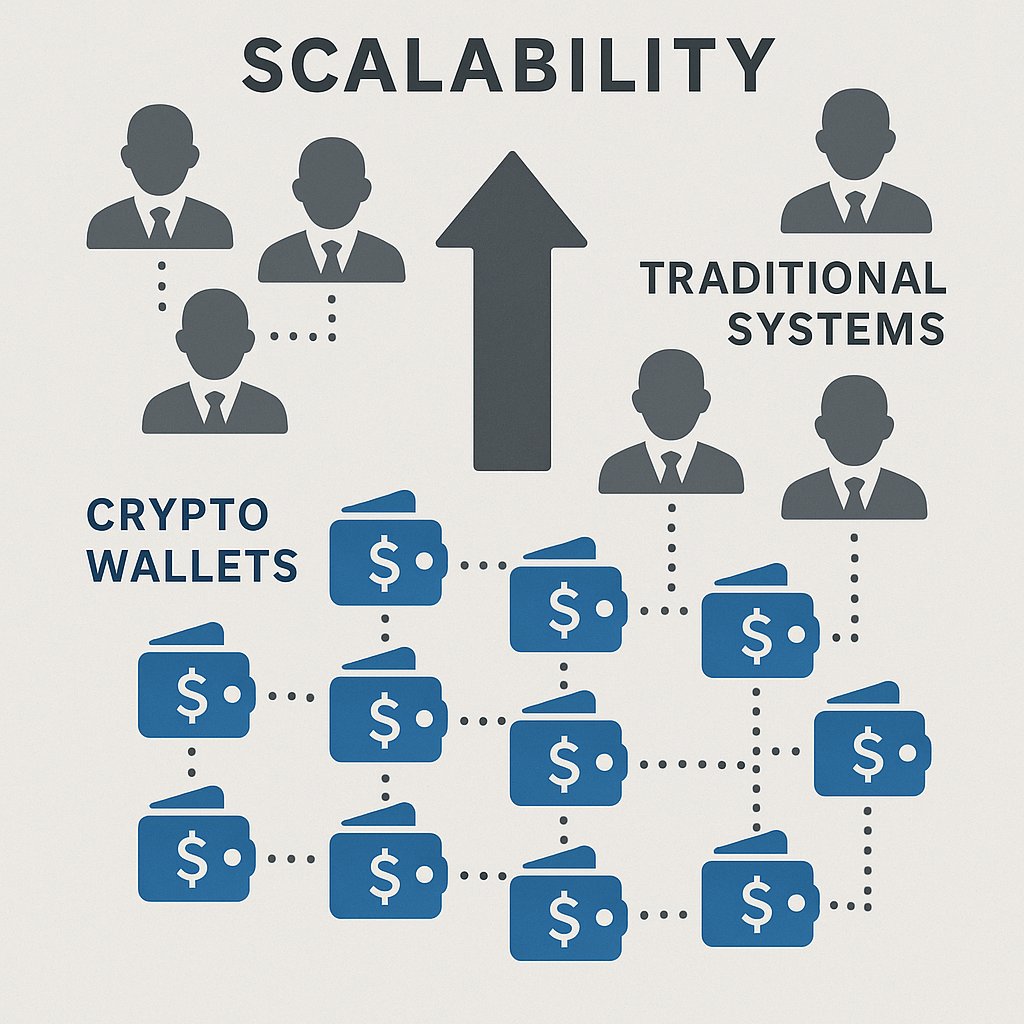

But perhaps the most profound limitation is one of scale and orchestration. As agent ecosystems grow, we will need to spin up new agents on the fly, each with its own wallet and funding source. Traditional systems simply cannot accommodate the rapid, programmatic creation and management of thousands or millions of accounts. Crypto wallets, by contrast, can be created and managed at scale, with no paperwork, no waiting, and no human intervention.

Settlement speed is another critical issue. Traditional payments are slow, often taking hours or days to clear, with multiple intermediaries and ledgers involved. For agents operating at digital speed, this is a non-starter. Crypto, especially on modern blockchains, offers near-instant settlement and atomic transactions, enabling real-time commerce at machine scale

Chargebacks, while a useful consumer protection for humans, are a nightmare for agent-based commerce. In the human world, chargebacks serve as a mechanism to resolve disputes and protect consumers. But for agents—especially in B2B or agent-to-agent scenarios—they introduce uncertainty and risk for service providers. Crypto’s irreversible transactions provide a more predictable and reliable foundation for agent commerce.

Finally, the technical infrastructure of the web is beginning to catch up with these possibilities. The long-neglected HTTP 402 “Payment Required” status, for example, can now be meaningfully implemented using crypto. Agents can programmatically handle payment requests, provide cryptographic proof of payment, and access resources in real time. This could usher in a new era of pay-per-use APIs and data services, with agents as the primary consumers.

Given these limitations, it’s clear to me that crypto and on-chain payments are not just a better option for AI agents—they are the only viable path forward. The technical advantages are numerous and profound.

First and foremost, crypto enables the creation of wallets for every agent, at any scale. Whether I need a single agent or a swarm of millions, I can programmatically generate wallets, assign permissions, and manage funds with unparalleled flexibility. This is essential for orchestrating complex workflows, segregating funds, and ensuring accountability in multi-agent systems.

The process of creating a crypto wallet is fundamentally different from opening a bank account. A wallet is simply a pair of cryptographic keys—public and private—that can be generated in milliseconds by an agent itself. There’s no need for paperwork, identity verification, or approval from a central authority. This means that agents can be spun up and decommissioned as needed, each with its own wallet, without any human bottleneck.

Smart contracts are another cornerstone of agent-native payments. These are self-executing programs that live on the blockchain and enforce the terms of an agreement automatically. For example, if an agent wants to pay for access to a data API, a smart contract can hold the payment in escrow, verify that the data was delivered, and release the funds only if the service was provided as promised. This level of automation and trustless execution is simply not possible with traditional payment systems.

Crypto’s global, borderless nature is another game-changer. Agents can send and receive payments instantly, anywhere in the world, without worrying about currency conversion, banking hours, or international wire fees. This opens the door to a truly global agent economy, where innovation and participation are not limited by geography.

Perhaps the most exciting feature is the ability to conduct true micro transactions. Crypto allows for payments of a cent, a mill, or even less, making it possible to build entirely new business models—pay-per-use APIs, real-time data feeds, and granular access to digital resources. This level of granularity simply isn’t possible with traditional rails. For example, an agent could pay another agent a tiny fee for a single API call, a snippet of data, or a few seconds of compute time, all settled instantly and with negligible overhead.

The programmability of crypto is equally transformative. With smart contracts, I can encode any payment logic I need—escrow, subscriptions, usage-based billing, multi-party payouts, and more. This flexibility is crucial as agent transactions become more complex and sophisticated. The blockchain’s transparency and auditability provide an additional layer of trust and accountability, ensuring that every transaction is verifiable and tamper-proof.

Another often-overlooked benefit is the elimination of chargebacks. In the human world, chargebacks serve as a consumer protection mechanism, but for agents—especially in B2B or agent-to-agent scenarios—they introduce uncertainty and risk for service providers. Crypto’s irreversible transactions provide a more predictable and reliable foundation for agent commerce.

Finally, the technical infrastructure of the web is beginning to catch up with these possibilities. The long-neglected HTTP 402 “Payment Required” status, for example, can now be meaningfully implemented using crypto. Agents can programmatically handle payment requests, provide cryptographic proof of payment, and access resources in real time. This could usher in a new era of pay-per-use APIs and data services, with agents as the primary consumers.

Of course, the adoption of crypto for agent payments is not without its challenges. Trust, regulation, and compliance remain significant hurdles, and it’s essential to address these head-on.

One of the most pressing issues is identity and accountability. In a world where agents can spin up wallets and transact freely, how do we prevent abuse, ensure accountability, and satisfy regulatory requirements? The answer, I believe, lies in a combination of identity verification, reputation systems, and transparent transaction histories.

Protocols for “Know Your Agent” (KYA) are emerging, building on the familiar frameworks of KYC (Know Your Customer) and KYB (Know Your Business). By linking real-world identities to agent wallets, and making this information available to counterparties who require it, we can balance openness with accountability. The system can remain open by default—any agent can join—but businesses and users can choose to interact only with verified agents if they wish.

Reputation and provenance are equally important. In a decentralized world, trust is built not just through identity, but through a transparent record of past behavior. Agents can accrue reputational capital based on their transaction history, attestations from other agents, and successful service delivery. Over time, standardized protocols for agent discovery, authentication, and payment will emerge, further strengthening the trust fabric of the agent economy.

Regulatory uncertainty is an ongoing challenge. The protocols for verification and compliance need to evolve alongside the technology. Some systems may choose to operate as closed loops, using credits or tokens that are redeemable only within a bounded ecosystem. Others will embrace open protocols, allowing for permissionless innovation while providing tools for compliance where needed. The key is flexibility—designing systems that can adapt to different regulatory environments and user preferences.

Authentication and verifiable service delivery are also critical. If I’m paying an agent to perform a task or deliver a service, I need assurance that the work was actually done. Verifiable inference—cryptographic proof that a model produced a given output—is one promising solution, though the technology is still maturing. In the meantime, a mix of centralized attestation and decentralized reputation systems will provide the necessary safeguards.

Looking ahead, the adoption of crypto for agent payments will unlock a host of new opportunities and fundamentally reshape the landscape of digital commerce.

One of the most immediate impacts will be the rise of “micro-gig” work and agent-to-agent commerce. Agents will take on small, discrete tasks—coding, testing, data analysis, and more—transacting with each other in real time and at machine speed. The volume of low-value, high-frequency transactions will explode, creating new efficiencies and revenue streams for both providers and consumers.

Data markets will become increasingly important, as agents pay for access to live data feeds, APIs, and digital resources. The ability to conduct true microtransactions will enable granular, pay-per-use models that simply aren’t possible today. This will benefit both data providers, who gain new revenue streams, and consumers, who pay only for what they use.

The familiar experience of shopping will also evolve. The traditional “shopping cart” may become obsolete, replaced by a collection of APIs and microservices orchestrated by agents on behalf of their users. Agents will negotiate and settle transactions instantly, with no need for manual checkout flows. While humans will continue to enjoy browsing and discovery, especially for physical goods and experiences, agents will handle an ever-larger share of digital commerce.

The flow of payments will also change. Today, most activity is human-to-agent—people paying agents to perform tasks or access services. But as agents become more autonomous, agent-to-agent payments will dominate, with agents spinning up new agents, subcontracting work, and transacting at a scale that dwarfs human commerce. The number of possible payment pairs will grow exponentially, creating a dense web of economic activity that is both more efficient and more complex than anything we’ve seen before.

Trust and reliability will remain paramount. While today’s agents are powerful but not infallible, I am confident that advances in security, authentication, and reputation systems will enable agents to surpass humans in reliability for many tasks. The transition will be gradual, but the trajectory is clear: as agents become more capable and trustworthy, they will take on an ever-larger share of economic activity, freeing humans to focus on creativity, innovation, and higher-order pursuits.

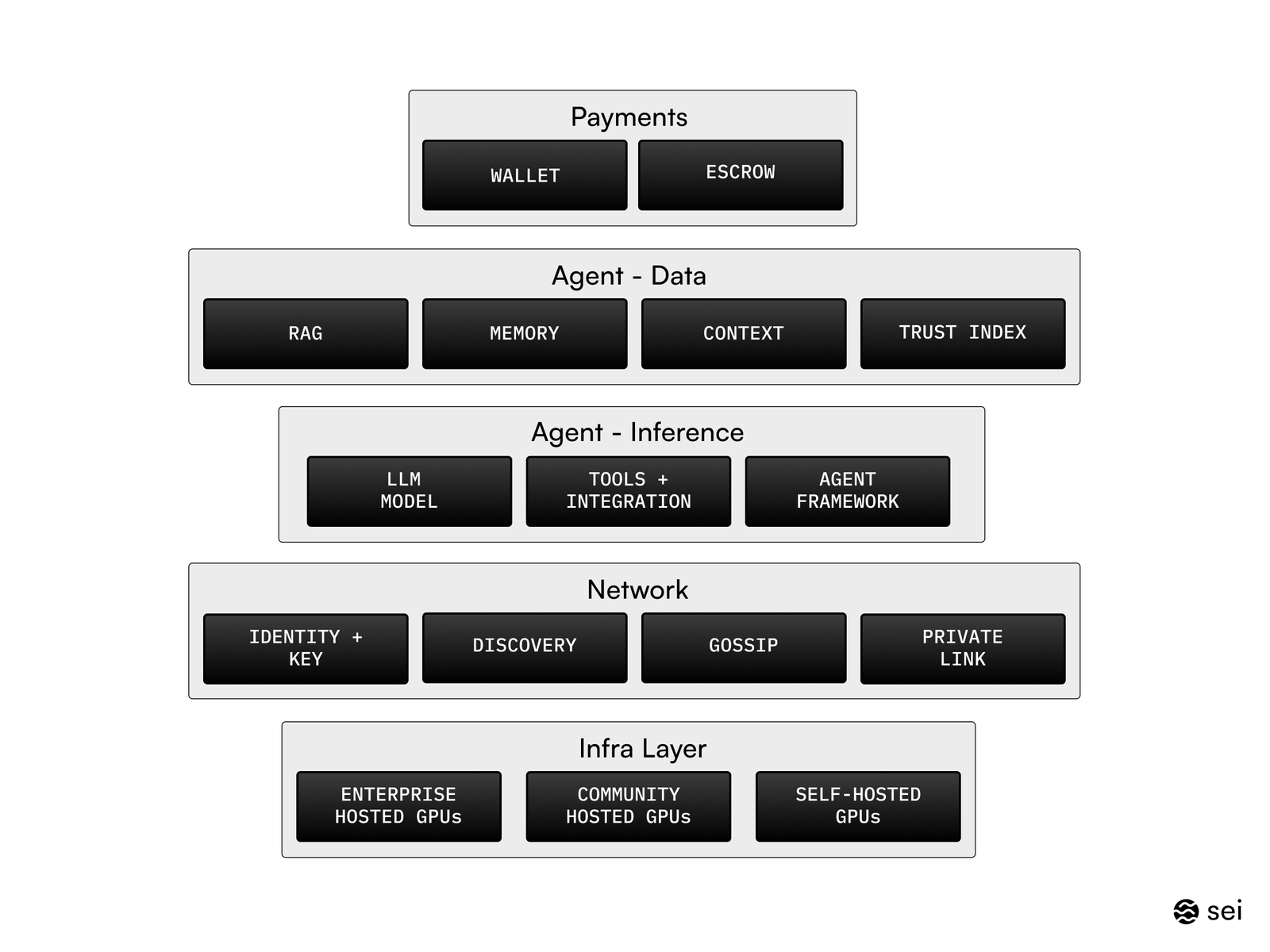

To really understand why crypto is such a perfect fit for AI agent payments, let’s peel back the layers and see what’s actually happening behind the scenes.

At the heart of it all is the crypto wallet. For an agent, a wallet isn’t some fancy app—it’s just a cryptographic keypair: a public key and a private key. The public key is like the agent’s home address on the blockchain, where anyone can send funds. The private key is the secret password that lets the agent actually move money around. What’s cool is that agents can generate these wallets on the fly, programmatically, and juggle as many as they need. They might keep one wallet for daily spending, another for long-term savings, or split funds across wallets to manage budgets and limit risk. It’s flexible, and it’s all automated.

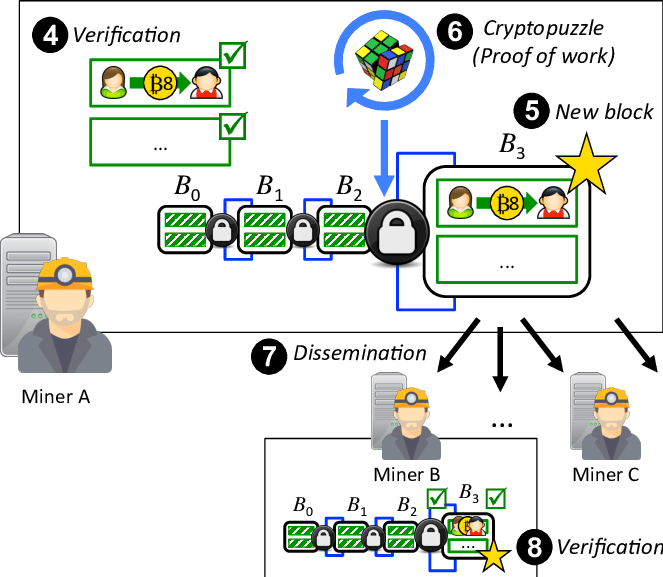

When it’s time to pay for something, the agent creates a transaction. This is basically a signed message that says, “Hey blockchain, please move this amount from my wallet to theirs.” The agent signs it with its private key, proving it’s the real owner. Then it broadcasts the transaction to the network. Miners or validators pick it up, check that everything’s legit, and once it’s approved, the transaction is locked into the blockchain forever. The whole process is fast, secure, and totally transparent—every transaction is out in the open, so anyone can audit the flow of funds.

But agents don’t just send money—they can handle more complex deals using smart contracts. Think of smart contracts as little programs that live on the blockchain and automatically enforce agreements. For example, a smart contract can hold funds in escrow, check if a service was delivered, and only release payment if all the conditions are met. No need for a middleman, no need to trust the other party—the code makes sure everyone plays fair. This is what lets agents do business with total strangers, anywhere in the world, without worrying about getting scammed.

Now, if agents are making tons of tiny payments—like paying a fraction of a cent for every API call, data packet, or compute cycle—doing all that directly on the blockchain would be slow and expensive. That’s where payment channels and layer-2 solutions come in. These are like opening a bar tab: agents can do thousands or millions of microtransactions off-chain, instantly and with almost zero fees. Only the final balance gets settled on the main blockchain. This makes it practical for agents to pay for even the tiniest units of service, without getting buried in transaction costs.

On-chain authentication is another key piece of the puzzle. Agents need to prove who they are and what they can do, but without exposing sensitive info. They use cryptographic signatures to prove ownership of their wallets, zero-knowledge proofs to show they meet certain requirements without revealing details, or get attestations from trusted third parties. This lets other agents (or humans) verify who they’re dealing with, what services are on offer, and whether the agent has a solid track record.

Trust is everything in a world of autonomous agents, and that’s where reputation systems and decentralized registries come in. Agents build up a reputation based on their transaction history, feedback from other agents, and successful service delivery. Decentralized registries act like open directories, storing metadata about agents—what they can do, how to reach them, who owns them. This makes it easy to discover, authenticate, and interact with agents across the ecosystem, and helps everyone avoid bad actors.

All these pieces—crypto wallets, transparent transactions, smart contracts, scalable payment channels, on-chain authentication, and reputation systems—snap together like LEGO blocks. The result is a system where AI agents can earn, spend, and manage money on their own, securely and efficiently, with every move visible and auditable. It’s a new kind of economy, built for machines, but open and trustworthy for everyone.

The convergence of AI and stablecoins is not just a technical challenge — it is a reimagining of how value moves in the digital world. By enabling agents to pay, get paid, and build reputations on-chain, we unlock new business models, new efficiencies, and new forms of collaboration. The agent economy is coming, and with it, a new era of programmable, permissionless, and profoundly human commerce.

The question is not whether agents will need crypto for payments, but how quickly we can build the infrastructure, protocols, and trust layers to make it happen. The building blocks are already here, and the pace of innovation is accelerating. As we navigate the challenges of trust, regulation, and user experience, I am convinced that the future of commerce will be shaped not just by humans, but by the agents we create—and the crypto rails that empower them.

[INVESTMENT DISCLAIMER]

Investing involves risks. This information is not investment advice or a recommendation to buy, sell, or hold securities. Readers should assess their financial situation and risk tolerance before making investment decisions. We are not liable for decisions based on this information

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.