A practical guide to how SMEs can use DeFi and stablecoin payments to reduce costs, improve cash flow, and access faster, more efficient financial infrastructure.

Decentralized Finance (DeFi) can be useful for small and medium-sized enterprises (SMEs), but the most practical business case is not broad DeFi speculation. For most SMEs, the immediate value is simpler: stablecoin payments can lower payment costs, speed up settlement, improve cross-border cash flow, and give finance teams more flexible digital payment options.

This article focuses on the payment side of DeFi rather than trying to cover the entire DeFi ecosystem. SMEs do not need to start with complex lending, trading, liquidity mining, or yield strategies to benefit from blockchain-based finance. A more realistic starting point is using stablecoins for supplier payments, contractor payouts, payroll, invoicing, and checkout. AllScale helps businesses approach these workflows through practical stablecoin payments, cross-border business payments, payroll, invoicing, and checkout use cases.

For SMEs, the strongest question is not whether DeFi is revolutionary in theory. The stronger question is whether stablecoin payment rails can make day-to-day financial operations faster, cheaper, and easier to manage. When implemented with custody controls, compliance review, smart-contract risk awareness, and a user-friendly workflow, the answer can be yes for selected payment scenarios.

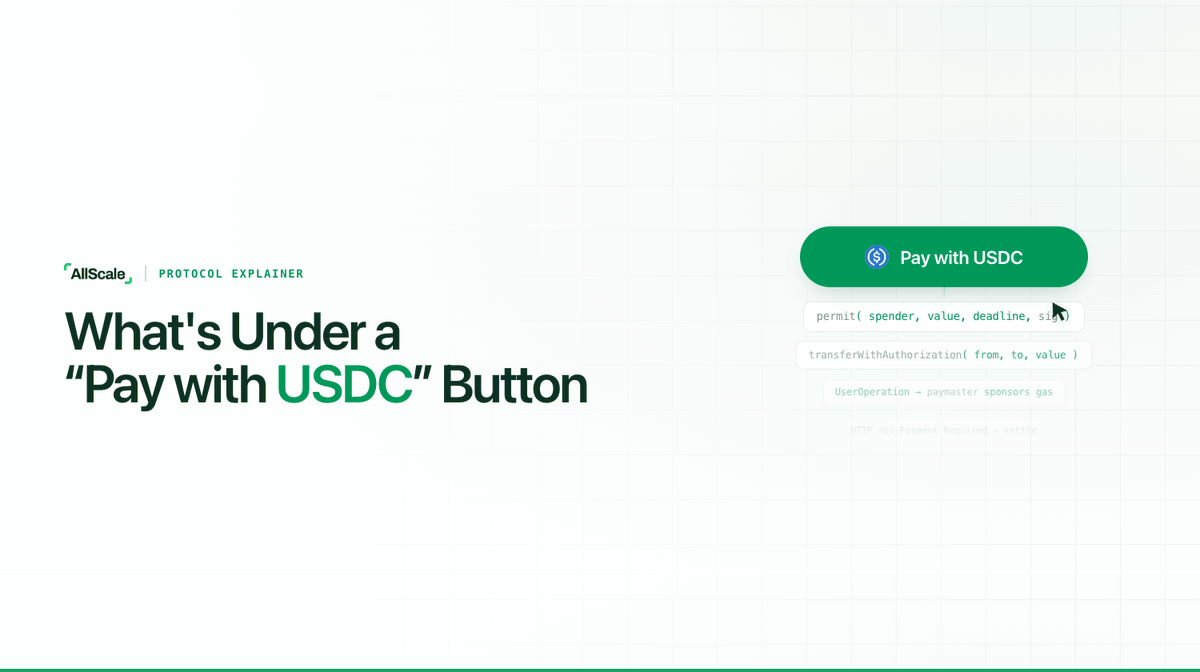

Stablecoin payment solutions allow businesses to send and receive digital assets designed to maintain a relatively stable value, usually by referencing a fiat currency such as the U.S. dollar. For SMEs, this matters because stablecoins can offer many of the operational advantages of blockchain payments while reducing exposure to the extreme price swings associated with more volatile crypto assets.

A stablecoin payment solution can support vendor payments, freelancer payouts, customer checkout, global payroll, and invoice settlement. Instead of waiting several business days for an international bank transfer, a business can settle a payment digitally and track the transaction more directly. This can be especially useful for SMEs that work with international suppliers, remote contractors, or customers across multiple markets.

The practical point is that stablecoin payments should be treated as a business payment workflow, not simply as a crypto feature. SMEs need records, approvals, reconciliation, compliance checks, and clear responsibilities. AllScale’s stablecoin payment workflows can be positioned around those operational needs.

Stablecoin payment solutions can help SMEs in three concrete ways: lower fees, faster settlement, and more flexible cash-flow management. These benefits are most relevant when traditional payment rails are slow, expensive, or difficult to manage across borders.

Lower fees matter because SMEs often operate with tighter margins than large enterprises. International wire fees, intermediary charges, foreign exchange costs, and payment processor costs can reduce profitability. Stablecoin payments may help reduce some of this friction, especially for recurring contractor payments, supplier settlement, and cross-border invoices.

Faster settlement matters because cash flow is often the biggest constraint for smaller businesses. When payments settle more quickly, SMEs can pay suppliers, compensate contractors, release orders, and reconcile accounts with fewer delays. Faster access to funds can also help businesses manage working capital more confidently.

Cash-flow flexibility is the third benefit. Stablecoins can give SMEs more options for how they receive and send digital payments, especially when they operate internationally. This does not mean every transaction should move to stablecoins, but it does mean stablecoins can become a useful additional rail alongside bank transfers, cards, and local payment methods.

Stablecoins can make cross-border payments easier by reducing dependence on slow intermediary banking routes. For SMEs that pay suppliers, contractors, agencies, or service providers in other countries, this can reduce delays and make settlement status easier to track. A stablecoin transfer can also simplify payment coordination when both parties agree on the asset, network, and settlement process.

The benefit is particularly clear for businesses that regularly make smaller international payments. Traditional cross-border transfers may involve fixed fees, exchange spreads, delays, and unclear tracking. Stablecoin payments can help SMEs send value digitally with clearer transaction visibility and potentially lower overall cost.

However, cross-border stablecoin payments still need business-safe controls. SMEs should confirm the correct recipient, wallet address, network, stablecoin type, invoice amount, and compliance requirements before settlement. A faster payment rail is useful only when the workflow prevents avoidable errors. AllScale’s cross-border payment solutions can be positioned as helping SMEs bring structure to these payment flows.

Crypto payroll, especially stablecoin payroll, can help SMEs pay global contractors, remote teams, and contributors more efficiently. The main advantages are faster settlement, lower cross-border friction, and improved payment visibility. These advantages are especially relevant for businesses that work with international freelancers or distributed operational teams.

Stablecoin payroll can reduce payment delays because funds can move through digital settlement rails rather than relying entirely on bank cutoffs and correspondent banking timelines. It can also reduce administrative friction by making payment records easier to connect with payroll files, contractor invoices, and transaction histories.

At the same time, crypto payroll should not be framed as a shortcut around payroll obligations. SMEs still need to consider worker classification, tax reporting, employment law, local compensation rules, and compliance requirements. AllScale’s payroll solutions should be presented as workflow support for compliant payment operations, not as a replacement for legal, tax, or HR review.

AllScale helps SMEs adopt stablecoin solutions by focusing on practical payment workflows rather than broad DeFi complexity. The goal is to help businesses use stablecoins for operational needs such as supplier payments, contractor payouts, invoicing, checkout, and payroll while maintaining clear approvals, records, and compliance-aware processes.

For many SMEs, the adoption challenge is not only technical. It is operational. Teams need to know who approves payments, which stablecoins are permitted, how wallet addresses are verified, how transactions are reconciled, and what happens when a payment fails or is disputed. AllScale can support these needs by helping businesses connect stablecoin payments with existing finance workflows.

This positioning keeps the article grounded. AllScale should not be described as giving SMEs unrestricted access to every DeFi activity. It should be described as helping SMEs adopt stablecoin payment tools responsibly and efficiently, with clear internal links to stablecoin payments, invoicing, payroll, and checkout.

AllScale’s payroll, invoicing, and checkout services should be framed around the practical ways SMEs move money. Payroll helps businesses pay global contractors, employees, or contributors through stablecoin-enabled workflows. Invoicing helps businesses issue, track, and settle invoices with clearer payment status. Checkout helps businesses offer stablecoin payment options to customers who prefer digital assets.

For payroll, the key message is speed and operational visibility. SMEs can use stablecoin payroll workflows to reduce payout delays and improve tracking, while still applying approval, compliance, and recordkeeping controls. Readers can be directed to AllScale’s payroll page for more detail.

For invoicing, the key message is faster receivables and cleaner reconciliation. Stablecoin invoicing can help SMEs receive payment from international customers or partners with fewer cross-border delays. The natural internal link is AllScale’s invoicing page.

For checkout, the key message is payment choice. Stablecoin checkout can help SMEs serve customers who want to pay with digital assets while keeping settlement and records organized. This section should link to AllScale’s checkout page.

AllScale supports multi-currency and global SME operations by helping businesses manage payment workflows across different markets. SMEs that operate internationally often deal with multiple currencies, payment methods, bank timelines, and supplier preferences. Stablecoin payments can provide an additional option for moving value across borders more efficiently.

The benefit is not that stablecoins eliminate every currency or compliance issue. Instead, they can reduce friction in selected workflows where both parties accept stablecoin settlement and the business has the right controls in place. For example, an SME might use stablecoins for international contractor payments while continuing to use local bank rails for domestic payroll or tax obligations.

This practical, hybrid framing is important. It avoids overstating DeFi and positions AllScale as a business payment workflow provider for SMEs that need flexibility, speed, and global reach.

DeFi can create new opportunities for SMEs, but this article should stay focused on payment benefits rather than broad DeFi coverage. The most immediate opportunity is stablecoin-based payment infrastructure. SMEs can use stablecoins to pay suppliers, receive customer payments, manage contractor payouts, and improve international settlement.

Yield should be handled carefully. If yield is mentioned, it should be framed as an upcoming or developing capability through vendor-provided pools on self-custodial infrastructure, not as a fully live or core product. The article should avoid implying that AllScale currently offers a complete yield product unless that is explicitly available. A business-safe phrasing is: “Future or on-demand yield-related workflows may involve vendor-provided pools built on self-custodial infrastructure, subject to risk review, compliance requirements, and product availability.”

SMEs should also understand the risks. Custody matters because businesses need to know who controls funds and private keys. Volatility matters because not all crypto assets are stable, and even stablecoins can carry peg, liquidity, or issuer risk. Smart-contract risk matters because code can contain bugs or depend on external systems. Compliance matters because payments may trigger tax, sanctions, AML, reporting, or licensing questions. UX complexity matters because employees and finance teams need clear workflows that prevent mistakes.

SME stablecoin transactions are most likely to grow where stablecoins solve clear payment problems. These include cross-border supplier payments, contractor payouts, creator payments, international receivables, and stablecoin checkout for digital-first customers. The trend is not simply that SMEs are adopting DeFi. The more precise trend is that SMEs are exploring stablecoin rails to reduce payment friction.

This distinction matters for search intent and credibility. An SME owner may not be looking for complex DeFi protocols. They may be looking for faster settlement, lower fees, fewer international banking delays, and better cash-flow control. The article should meet that intent directly.

AllScale’s strongest cluster fit is therefore stablecoin payments and cross-border business payments, supported by related pages for payroll, invoicing, and checkout.

Stablecoin payments can be useful, but SMEs should implement them with business-safe controls. Custody is one of the first questions to resolve. A business must understand whether it controls its own wallet, uses a third-party custodian, or relies on a hybrid model. Each approach has different operational, legal, and security implications.

Volatility and stablecoin design should also be reviewed. Although stablecoins are designed to maintain stable value, SMEs should still evaluate the asset’s reserve model, liquidity, issuer risk, network support, and redemption options. Businesses should avoid assuming that every stablecoin has the same risk profile.

Smart-contract risk is another consideration. If payment workflows use smart contracts, SMEs should understand how the code is tested, audited, upgraded, and paused in emergencies. If payments depend on external data or approvals, teams should also define how exceptions and disputes are handled.

Compliance controls should be built into the workflow before settlement. SMEs may need KYC, KYB, AML, sanctions screening, tax records, invoice documentation, and transaction monitoring depending on the use case and jurisdiction. UX complexity should also be addressed through simple approval flows, clear wallet instructions, and user education.

A practical mitigation strategy is to start with one narrow payment workflow, such as international contractor payments or stablecoin invoicing, and expand only after the business has tested approvals, reconciliation, compliance checks, and incident handling.

Stablecoins generally include fiat-collateralized, crypto-collateralized, and algorithmic designs. For most SMEs using stablecoins for payments, fiat-collateralized stablecoins are often the easiest to understand because they are designed to track a traditional currency. However, businesses should still evaluate issuer risk, liquidity, reserve transparency, network support, and redemption options before choosing an asset.

The right stablecoin depends on the payment workflow. A company paying international contractors may prioritize liquidity and wallet compatibility. A company accepting checkout payments may prioritize customer demand and settlement reliability. A company managing vendor payments may prioritize accounting treatment and operational controls.

SMEs can support compliance by defining policies before stablecoin payments go live. This includes deciding which counterparties can be paid, which stablecoins and networks are approved, what documentation is required, and when additional review is needed. Depending on the jurisdiction and use case, businesses may need KYC, KYB, AML, sanctions screening, tax reporting, and transaction monitoring.

AllScale can be positioned as helping SMEs organize payment workflows and records, but businesses should remain responsible for legal, tax, and compliance decisions. This framing is safer than suggesting stablecoin tools automatically solve compliance.

Tax treatment varies by jurisdiction, so SMEs should keep detailed records of stablecoin transactions, invoice values, payroll payments, fees, conversions, and settlement dates. Even when a stablecoin is designed to track a fiat currency, a business may still need to account for gains, losses, fees, and reporting obligations depending on local rules.

The safest guidance is for SMEs to work with tax professionals who understand digital asset payments. AllScale’s role should be framed around payment workflow organization and record support rather than tax advice.

Yes, stablecoin payments can be integrated with existing accounting workflows when the business has the right data structure. Finance teams need to connect invoices, payment approvals, wallet addresses, transaction hashes, fees, and settlement status to accounting records. This makes reconciliation easier and reduces manual work.

AllScale can support this operational layer by helping businesses connect stablecoin transactions with invoicing, payroll, and payment automation workflows. The goal is to make stablecoin payments fit into normal finance operations rather than creating a separate, hard-to-audit process.

Smart contracts can automate payment rules such as scheduled payouts, milestone-based settlement, invoice approval, or conditional release. For SMEs, this can reduce manual payment work and make settlement more predictable. Readers who want more detail can explore AllScale’s article on smart contracts for business payments.

However, smart contracts also introduce risk. Code may contain bugs, external data may be wrong, and automated settlement can be difficult to reverse. SMEs should use smart contracts for clear, well-tested workflows and keep approval gates, pause procedures, and dispute handling in place.

SMEs should begin with practical payment education rather than advanced DeFi topics. The first step is understanding how stablecoins work, how wallets and networks operate, how transaction fees are paid, and how payment records are reconciled. From there, teams can learn about payroll, invoicing, checkout, and cross-border settlement.

AllScale’s documentation and blog can be used as internal links for readers who want implementation guidance. Education should also cover custody models, compliance responsibilities, fraud prevention, and user experience so finance teams can adopt stablecoin payments safely.

Is DeFi suitable for SMEs?

DeFi can be suitable for SMEs when it is used for practical, controlled payment workflows such as stablecoin invoicing, contractor payouts, cross-border supplier payments, and selected payroll use cases. It is less suitable when a business lacks clear custody procedures, compliance review, wallet security, accounting processes, or staff training.

The safest starting point is not broad DeFi adoption. It is a narrow stablecoin payment workflow with clear approvals, spending limits, compliance checks, and reconciliation. More complex DeFi opportunities, including yield-related workflows, should be evaluated carefully and treated as upcoming, vendor-provided, or case-by-case capabilities where applicable.

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.

-%E5%B0%81%E9%9D%A2.jpg)