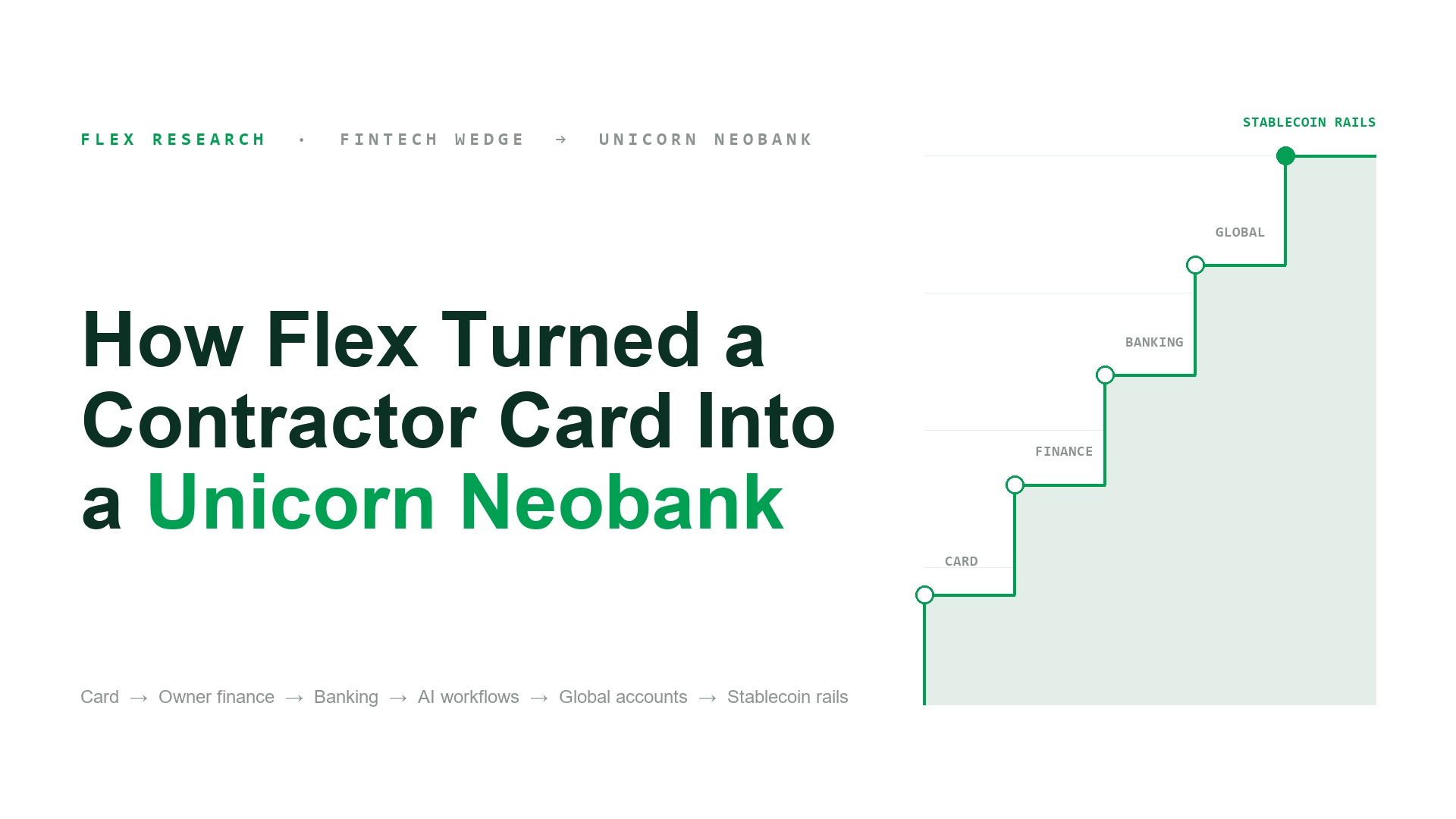

Flex went from a 2020 construction-invoicing tool to a 2026 unicorn neobank. This deep dive traces each year — contractor card, credit float, payments, owner finance, AI workflows, and stablecoin rails — showing how each stage earned the next, and why the biggest fintech stories usually start as a small, specific cash-flow problem.

Flex just turned into a unicorn this week with their $70M series B1 raised. Here is each year's story since they started as a construction card business.

Most fintechs want to start as platforms. Flex started with a very unsexy problem: contractors do the work, send the invoice, and still wait months for cash. That is the interesting part. The unicorn story came later. It is a very clean example of how a fintech wedge expands:

1. Start with one painful cash-flow problem.

2. Build the financial product that actually solves it.

3. Use the data from that product to expand into adjacent workflows.

4. Reframe the customer once the product surface is big enough.

It did not even start as a broad SMB finance platform. It started with contractors who needed to get paid.

First, congrats to the Flex team. Building from a contractor-card wedge into a reported unicorn is hard. Doing it while expanding across credit, banking, AI workflows, global accounts, and stablecoin rails is even harder. We are writing this partly as research, but also with real respect.

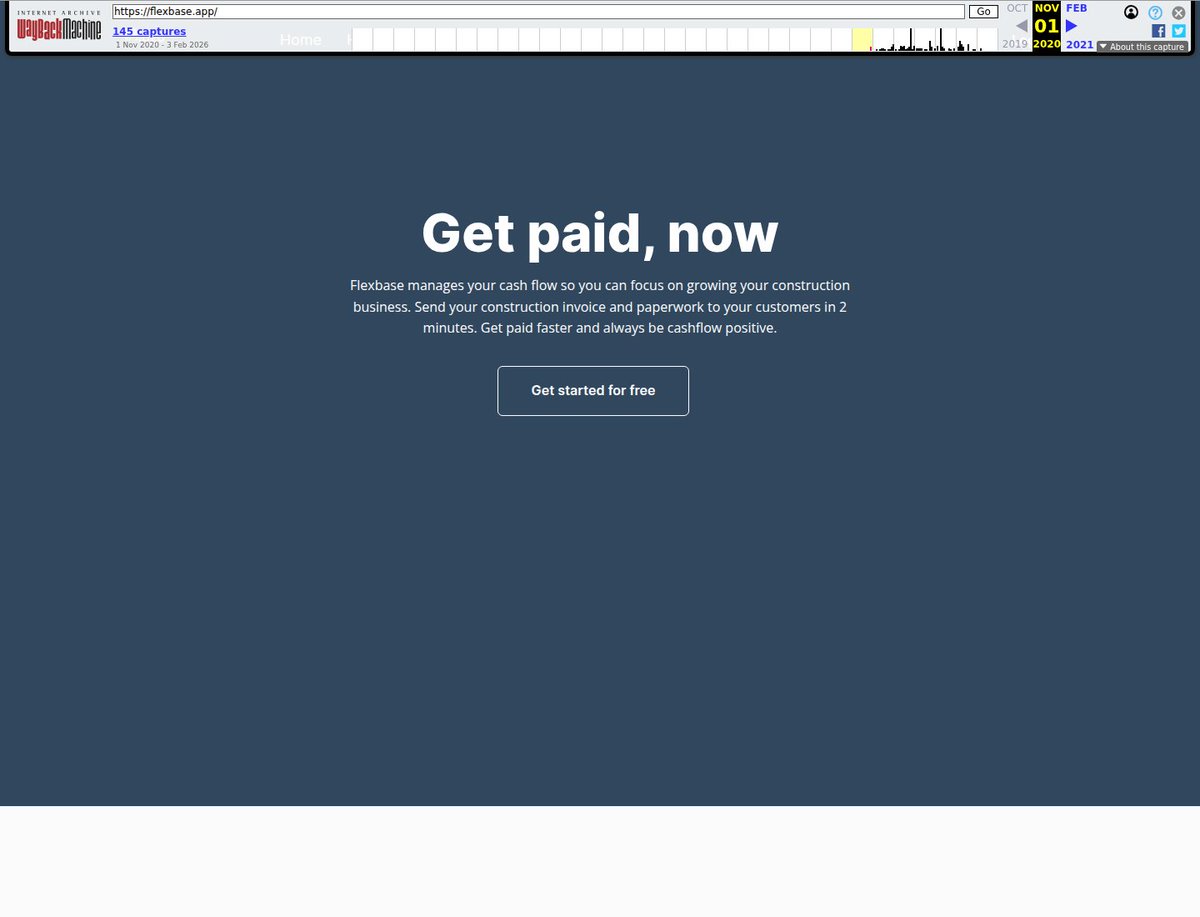

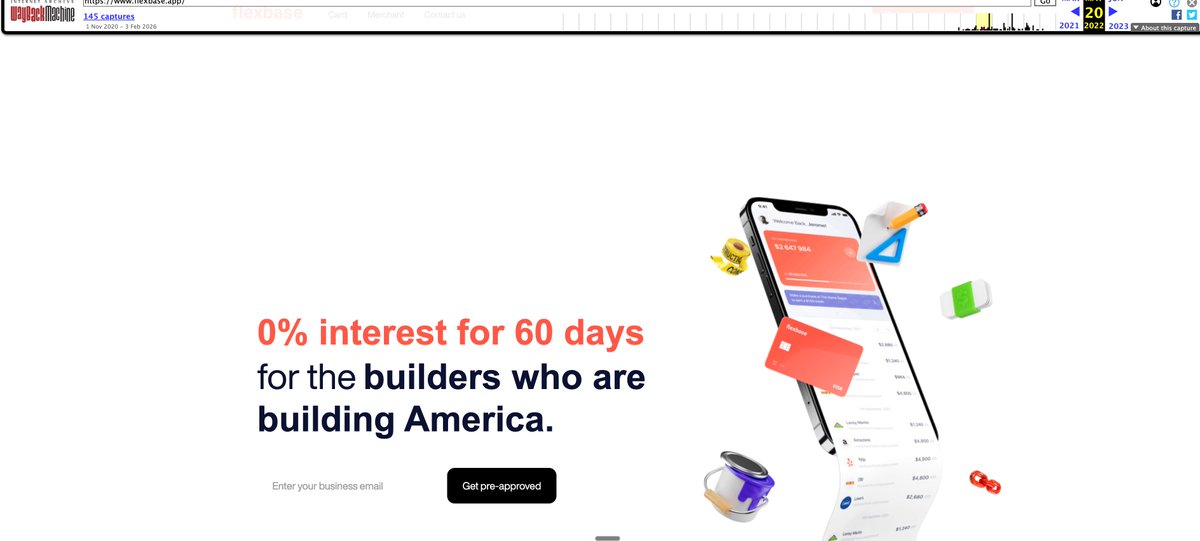

The 2020 Flexbase homepage was not glamorous. It was basically: “construction paperwork sucks, invoices get stuck, cash comes late, we can help you get paid faster.” That's it.

The page talked about construction invoices, paperwork, compliance documents, reminders, and faster payment. This is the kind of wedge we like. Not because "construction is a big market." Everyone says that about every market. It is the default founder slide. The better reason is that construction has weird financial physics. A contractor can:

• win the job

• do the work

• send the invoice

• still wait months for cash

• get delayed because one document is missing

• need to pay workers and suppliers anyway

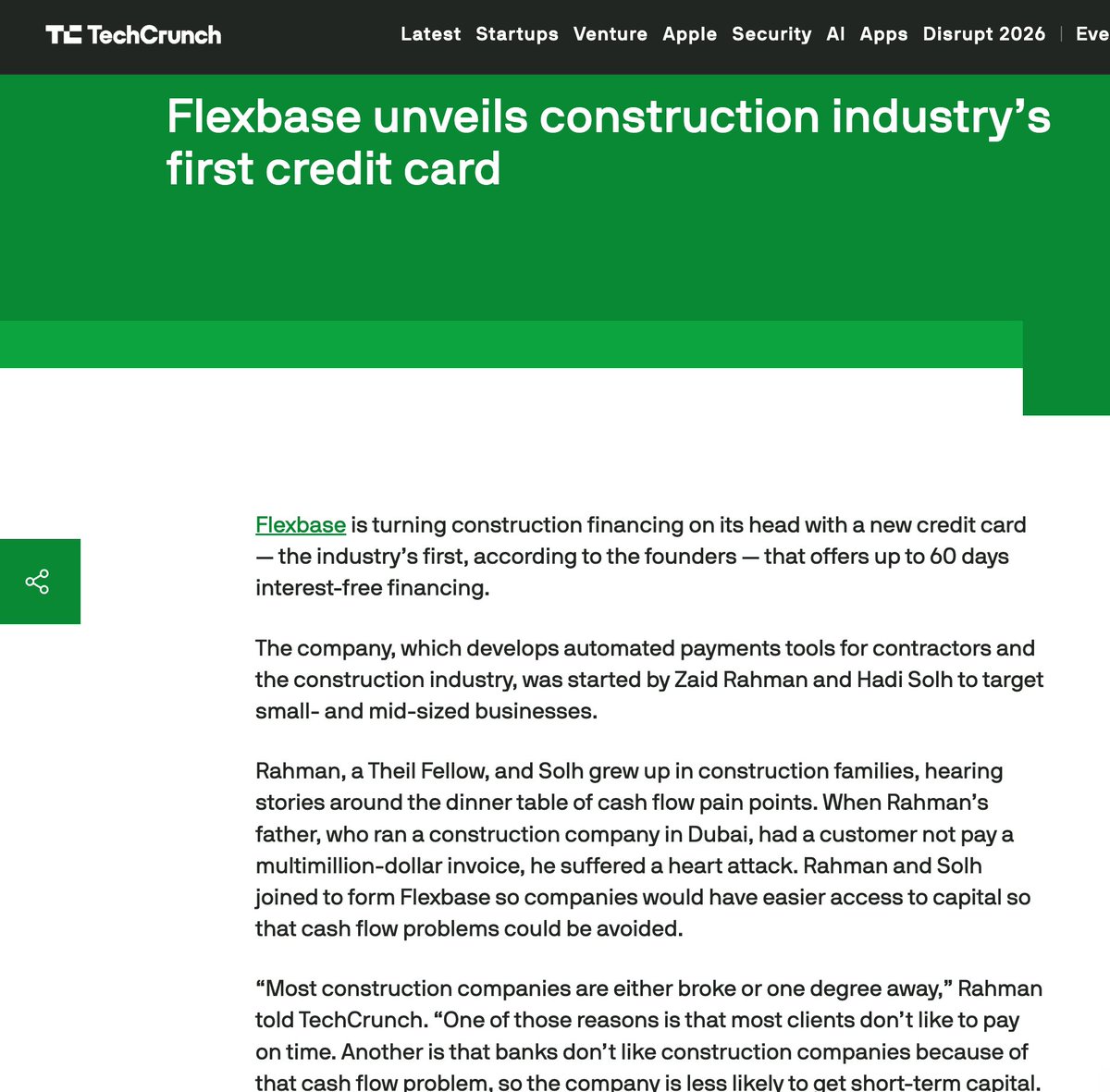

TechCrunch's 2021 Flexbase profile makes the origin story pretty clear. Zaid Rahman's father ran a construction company in Dubai. An unpaid multimillion-dollar invoice created a real cash-flow crisis for the family. Rahman and co-founder Hadi Solh both had construction-family context. TechCrunch also reported that construction companies can wait more than 100 days to get paid, and that payment applications can be 50 to 100 pages.

That is founder-market fit.

Not "I read a report." More like: I have seen exactly how this breaks in real life. The first insight: workflow was the door, float was the product.

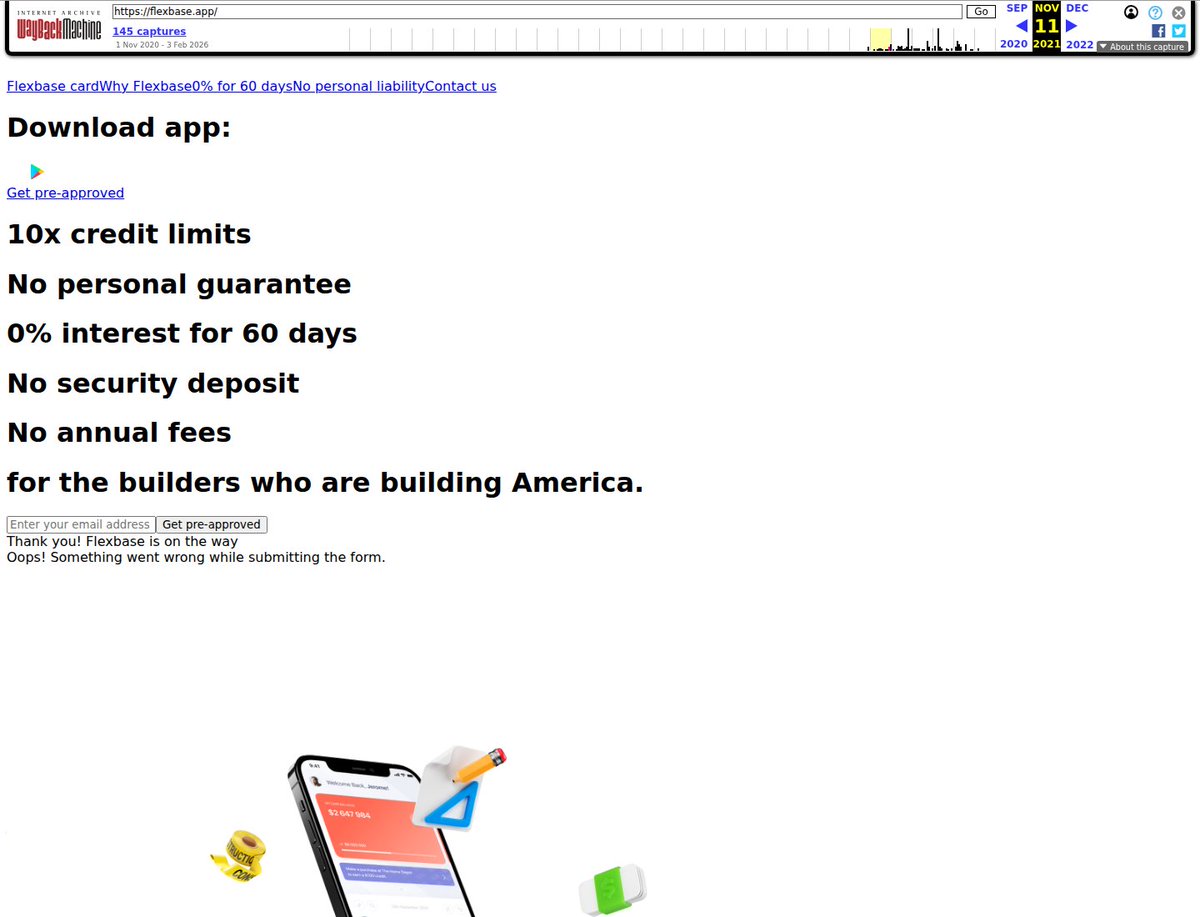

The 2020 product was workflow. Invoices. Paperwork. Reminders. Compliance docs. Useful, but not enough. By November 2021, Flexbase had changed the pitch. Now the homepage was selling:

• 10x credit limits

• no personal guarantee

• 0% interest for 60 days

• no security deposit

• no annual fees

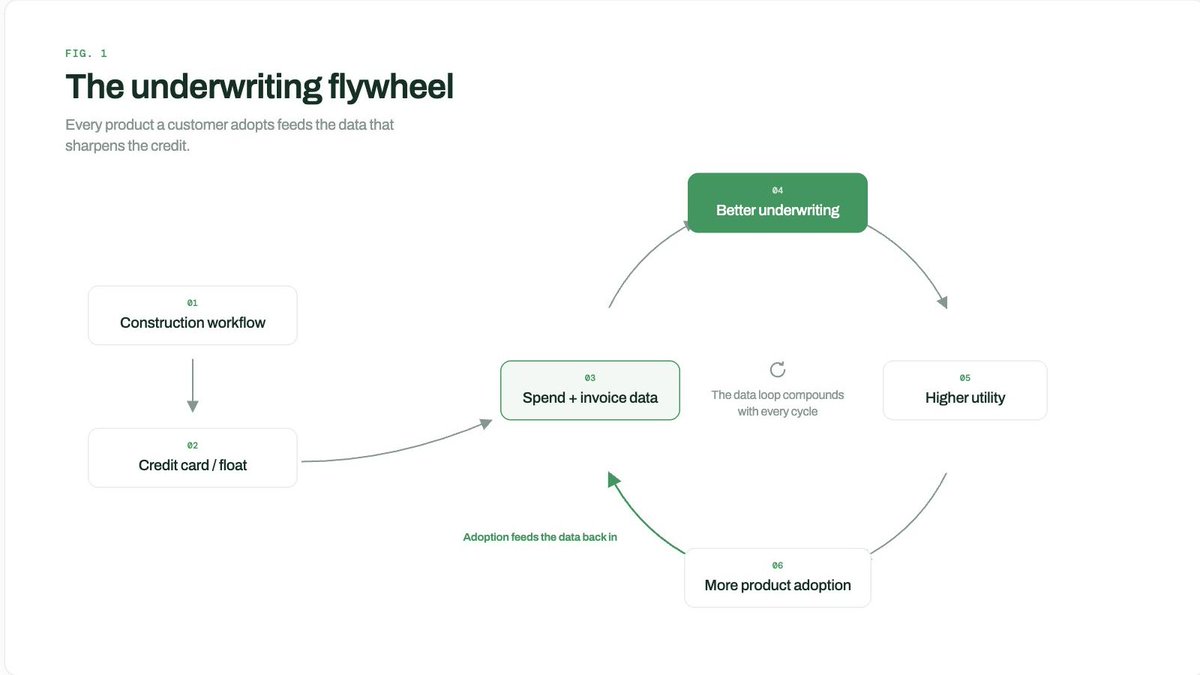

This is the first real lesson for fintech founders: workflow helps you understand the pain. But money timing is often the actual product. If a customer is dying because cash arrives late, giving them better dashboards may help. Giving them float changes the game. This is why vertical fintech is so interesting and so dangerous.

The software wedge gets you close to the customer. But the real monetization often comes from:

• credit

• payments

• settlement speed

• underwriting

• treasury

• FX

• working capital

Flexbase's move from "send invoices faster" to "get 60 days of float" was the moment the company became more than vertical SaaS. The loop becomes obvious:

That is the kind of loop investors love because each layer makes the next layer more believable.

By mid-2022, archived Flexbase pages showed three product surfaces:

• Card • Payments • Merchant

The Merchant product is the one that stood out to us. Flexbase pitched a buy-now-pay-later style button for construction suppliers. Contractors could buy materials and pay 60 days later. Suppliers got paid upfront.

This is a small detail, but we think it matters. Flexbase was not just thinking: "how do we issue a better card?"

It was thinking: "how do we sit inside the moment where B2B money gets stuck?"

That is a much bigger idea. The card was one surface. But the actual job was: make business cash flow less painful. Once you see that, the later product expansion makes more sense.

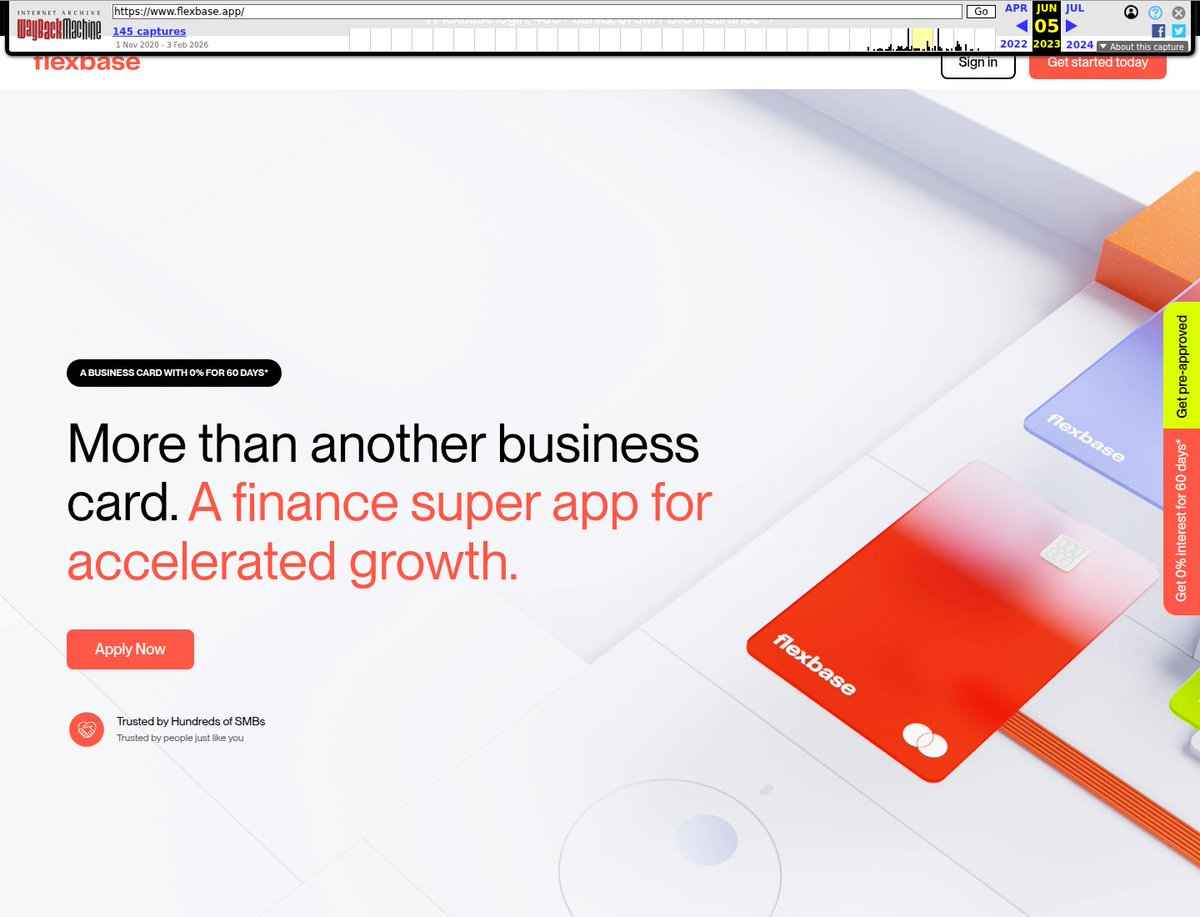

By 2023, the wedge had clearly widened. The June 2023 homepage called Flexbase "more than another business card" and "a finance super app for accelerated growth."

We guess this is also when they decided to use @FlexSuperApp as their X handle.

Then in September 2023, Flex, formerly Flexbase, announced $120M in debt and equity:

• $20M Series A equity led by Florida Funders

• up to $100M debt financing from Community Investment Management

• participation from Home Depot Ventures, MS&AD Ventures, Companyon Ventures, and others

• launch of Flex Credit Card, Flex Banking, and a finance super app

The capital stack is also a product roadmap. Flex did not raise like a normal SaaS company where every round is just more engineers and more sales reps. It needed two kinds of money:

• equity to build product, team, brand, and M&A

• debt/credit facilities to fund customer float and lending

That matters because the product itself depends on capital. Here is the clean version:

• May 2021 — Flexbase pre-seed: $2.5M equity. Construction payment workflow and the original contractor cash-flow wedge

• Sept 2023 — Series A + rebrand: $20M equity + up to $100M debt. Flex Credit Card, Flex Banking, finance super app, and credit-card float capacity

• March 2025 — Equity round + credit facility: $25M equity + $200M credit facility. Payments infrastructure, personal finance software, and more credit capacity

• April 2025 — Maza M&A / Flex Consumer: Deal value not disclosed by Business Wire; additional $10M equity injection from Wellington. Consumer/solopreneur onboarding, entity formation, and the personal-business finance bridge

• Dec 2025 — Series B: $60M equity. AI-native private-bank positioning, owner finance, personal finance, private credit, and AI tools

• July 2026 — Series B1 / Flex Global: $70M equity. Global banking, stablecoin-powered cross-border rails, multi-currency accounts, and private credit expansion

It moved from "business finance" to "owner finance."

That sounds like wordplay, but it is a very different customer model. In March 2025, TechCrunch described Flex as a "Brex for business owners" and reported:

• $25M equity round

• $200M credit facility

• valuation just under $250M

• focus on mid-market business owners who are also CEOs

• average customer revenue of $25M a year, according to Flex

• revenue from card/bill-pay transaction and interchange fees, deposit products, and a subscription membership for the personal platform

This is where the story gets good. Most corporate card products are built around the company:

• employees,

• policies,

• budgets,

• approvals,

• finance teams,

• procurement.

Flex is trying to build around the owner:

• business card

• bank account

• vendor payments

• personal spending

• entity formation

• commingled transactions

• credit

• private-bank relationship

The owner is the economic person. The company is only one container. This is why the "private bank" language is not random. If you are serving the owner, eventually business finance and personal finance start touching each other. Messy? Yes. But also very real. Every founder knows this in their bones. Your company card, your personal card, your payroll anxiety, your bank balance, your tax planning, your entity setup, your global contractors... it all lives in the same brain.

Maza was not random M&A

The Maza deal makes the owner thesis much clearer. In April 2025, Flex and Maza announced an M&A deal. Maza became Flex Consumer, focused on helping business owners manage commingled personal and business finances. Business Wire described Maza as one of the largest entity formation and payments apps for Spanish-speaking solopreneurs and consumers. It had built LLM-powered automation, entity formation, a unified ledger, and transaction categorization.

If Flex was only a business card company, Maza looks confusing. If Flex wants to own the owner's financial life, Maza makes sense. The path looks like this:

1. Person starts side hustle.

2. Person forms entity.

3. Personal and business money get mixed.

4. Business grows.

5. Owner needs banking, card, bill pay, credit, treasury, global payments.

6. Profits become personal wealth.

That is not a random product map. That is the owner's journey. And if you own the journey early enough, you can grow with the customer instead of trying to acquire them after a bank already owns the relationship.

By late 2025, Flex was using much bigger language. In December 2025, Flex announced a $60M Series B led by Portage. Flex said it had reached $105M in total equity, grown revenue 4x over the prior year, launched personal finance, tripled private credit offerings, and introduced AI-powered tools.

The December 2025 Wayback capture of Flex's AI Inbox page pitched turning vendor emails into payments automatically.

Then came the unicorn round. Tech Funding News reported that Flex raised a $70M Series B1 led by Ryan Smith and Ryan Sweeney's Halo Fund, and that the company's valuation was reported at $1.2B. Flex said:

• annualized revenue had tripled since December 2025 and exceeded nine figures

• annualized TPV passed $10B

• total funding reached $180M equity and $300M debt

• Flex Global was announced with support for 100+ countries

• multi-currency accounts covered 76 countries and 32 currencies

• private credit was available in 20+ countries

• the average customer used four or more Flex products

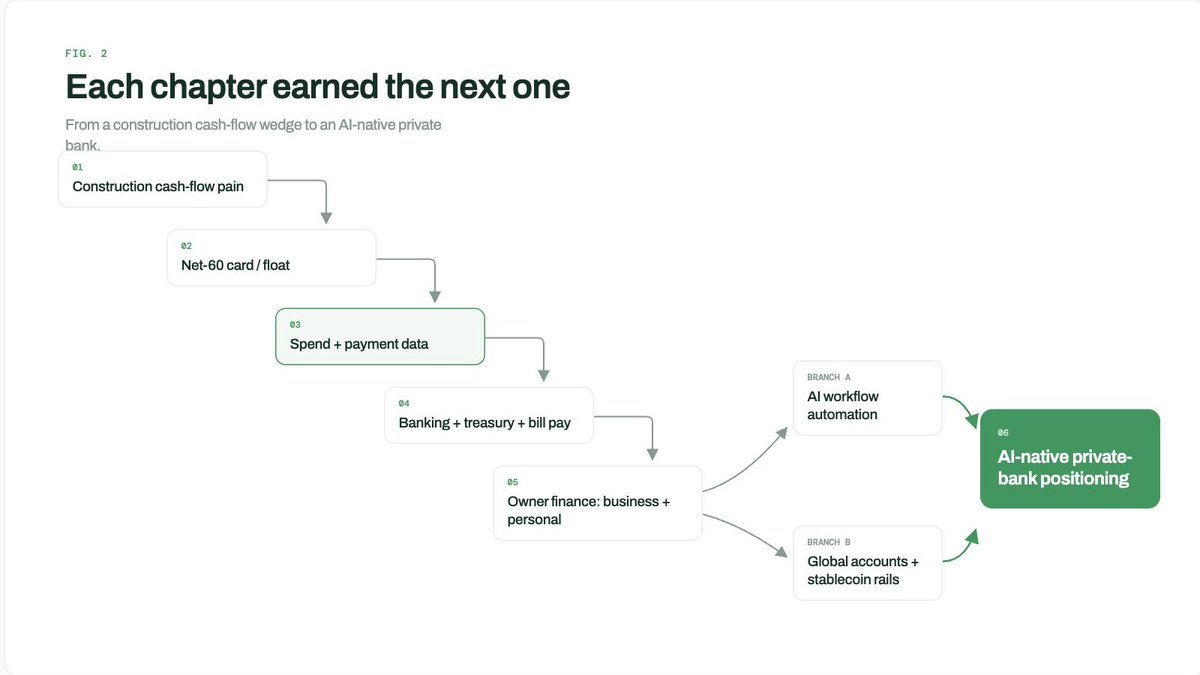

Our read: Flex worked because each chapter earned the next one.

Construction revealed the wound. Credit monetized the wound. Payments and banking expanded the surface. Owner finance reframed the customer. AI automated the workflow. Stablecoins expanded the geography. That is a real sequence. Not easy. Not guaranteed. But real. The interesting part is that the company did not jump from construction to "AI private bank" in one move. It kept changing the altitude of the customer definition:

• 2020 — Contractor waiting on invoices: Paperwork, invoicing, payment reminders

• 2021 — Contractor needing float: Card, higher credit limits, 60-day financing

• 2022 — Construction buyer/supplier network: Payments, merchant checkout, material purchases

• 2023 — Business owner: Card, banking, treasury, finance super app

• 2025 — Owner as business + person: Personal finance, entity formation, commingled transactions

• 2025-2026 — Owner with workflows and global money movement: AI Inbox, private credit, global accounts, stablecoin rails

Flex did not abandon the earlier wedge. It kept translating the same problem into a larger system: cash gets stuck, the owner has to keep moving anyway.

1. Find a cash-flow wound.

2. Build workflow around it.

3. Add the financial product that actually solves it.

4. Use the data to underwrite and expand.

5. Follow the economic person, not just the account.

That is the part worth studying. Flex did not become interesting because it became an AI/stablecoin company. It became interesting because it kept moving closer to the owner's money problem. That is the game.

Personal note: this is also why Flex's journey is inspiring to us at @allscaleio. We are building a non-custodial stablecoin neobank.

And we did not start with the big category language either. Our first feature release was in December 2025 - We started with invoicing problems for freelancers, content creators, and gig workers.

Very small. Very specific. Very unsexy. But that is the lesson we keep coming back to from Flex: the ambitious fintech story usually starts as a boring cash-flow problem for a very specific customer.

Congrats again to the Flex team. The milestone is impressive! The path to get there is even more interesting.

We've been enjoying @defyneric's post a lot! Hope this deep dive can inspire more founders!

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

Sign up for our newsletter to get latest updates

AllScale is a financial technology developer, not a bank and does not provide digital assets custodian services.

© Copyright 2026. All Rights Reserved.